Getting Meaning from Monthly Reports

Understanding income statements, rent rolls, A/R, and balance sheets

Let’s anchor in on where we are in the process of learning how to be a real estate investor.

You own your first property.

You have a business plan and are in the early stages of executing it.

You have hired a local property management and accounting firm.

You are eyes wide open that unexpected issues will come up.

Having a clear business plan relative to leasing and construction is probably the most important step you must take. We will get into the details of this in a future newsletter.

Today we are going to discuss how to interpret and get meaning from the monthly reporting package you will receive from your property management and accounting team.

I will define and discuss the individual reports that go into the reporting package:

Summary page

Rent Roll

Accounts Receivable (aka A/R)

Cash Flow and Income Statement with a Comparison to Budget

Balance Sheet

Construction Activity & Leasing Report

You do NOT need to have any accounting knowledge to understand these. All you need is patience, common sense, and a little guidance from Professor Bateman.

Let’s dig in.

Reporting Package Overview

Let’s start with the very basics.

What is a “reporting package” and where does it come from?

What: a reporting package is a collection of reports that help you understand how your property is performing.

When: it will likely be delivered to you within the first 10 days for the month and include activity for the previous month. Example: by May 10th you receive the report for April.

Format: it will be a pdf sent to you by the property manager.

The property manager’s accounting team will have prepared it according to the company’s accounting practices combined with the structure you (the client) have agreed upon. [Note: if you don’t have a property manager, you might have prepared it yourself or hired an accountant to do it.]

You don’t need to be an accountant to understand the reports, but it does help to have some foundational knowledge. Here are some basics.

Whenever there is financial activity at a property, the accountant records it in the general ledger. This could include:

Rent charged to or paid by the tenant.

A maintenance invoice received by or paid to a vendor.

Distributions made to investors.

And any other financial activity.

Think of the general ledger as a big excel file with (i) a date, (ii) a category ID, (iii) the amount, and (iv) comments.

Most reports are just a roll up of this activity, summarized in a specific way using the dates, category IDs, and amounts.

That’s about it. Yes, it is an oversimplification of the reporting process but it gives you an overview of how it works.

To be clear, it is way more complicated if you are doing the work, but as a reader of reports this should anchor you on the basics.

Now let’s discuss the individual reports within the reporting package. Your specific report may be different in order and content. Use the list below as an example only.

#1 - Summary Page

The summary page is just as it sounds: a summary. It will include highlights such as:

Property square feet and percent leased.

List of new or vacating tenants.

Amount of rent not paid (aka delinquent).

List of construction or maintenance projects.

Current cash, recent distributions, NOI and any other “snapshot” financial data.

There may be comments on some or all of these or it could just be a statement of the facts.

All of it will likely be in one page. It will help you understand the overall property performance before you read the individual reports.

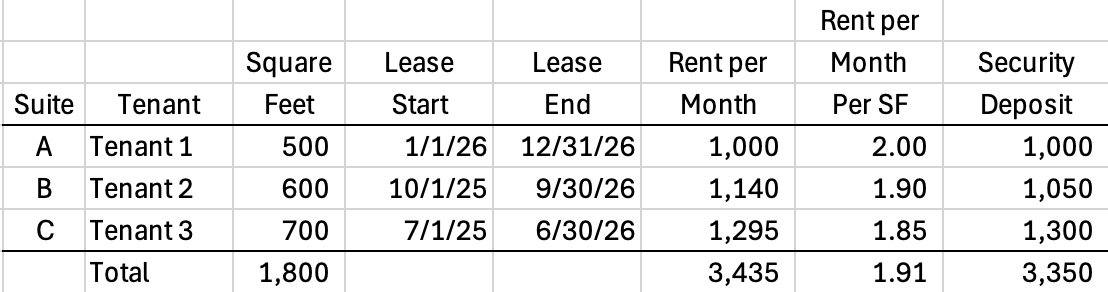

#2 - Rent Roll

The rent roll is a summary of the leases and suites for your property.

Each accounting firm will create a slightly different version of a rent roll. Rent roll templates can also differ by asset class.

See below for an example of a rent roll for a three unit residential property.

Example: Rent Roll of 1-4 Unit Residential Property

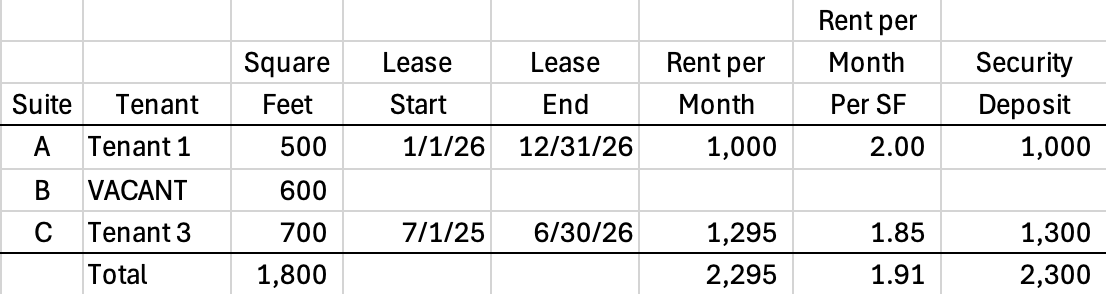

It gives you a way to see your tenants in a summarized report. If there was a vacant suite, it would be listed as vacant as shown in the example below.

Example: Rent Roll of 1-4 Unit Residential Property - Including Vacant Suite

Important Note: never rely exclusively on your rent roll when making a decision about a specific tenant. In this case, you want to refer to the signed lease as there could have been a mistake made when the rent roll was prepared.

That being said, rent rolls are very useful to reference day to day.

Let’s move on to the A/R report.

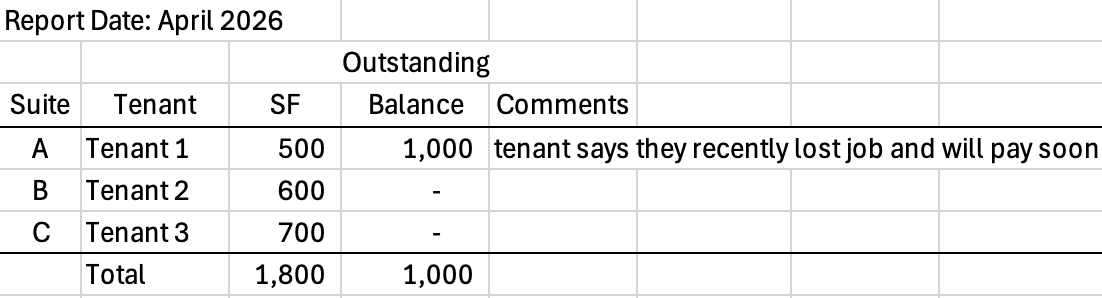

#3 - Accounts Receivable (A/R)

Whereas a rent roll lists what each tenant is contractually required to pay each month, the A/R report will be your guide to what the tenant actually paid.

In the example above, Tenant 1 in suite A is supposed to pay $1,000 per month. If they did not pay that month, the A/R report would show this outstanding balance (aka delinquency).

Example: A/R Report

The comments would have been added by the property manager who would have (hopefully) contacted the tenant to find out what was going on.

It is then your decision as the property owner to decide whether to allow the tenant some time to catch up on the rent or move to eviction.

Let’s move on to the overall property performance reports.

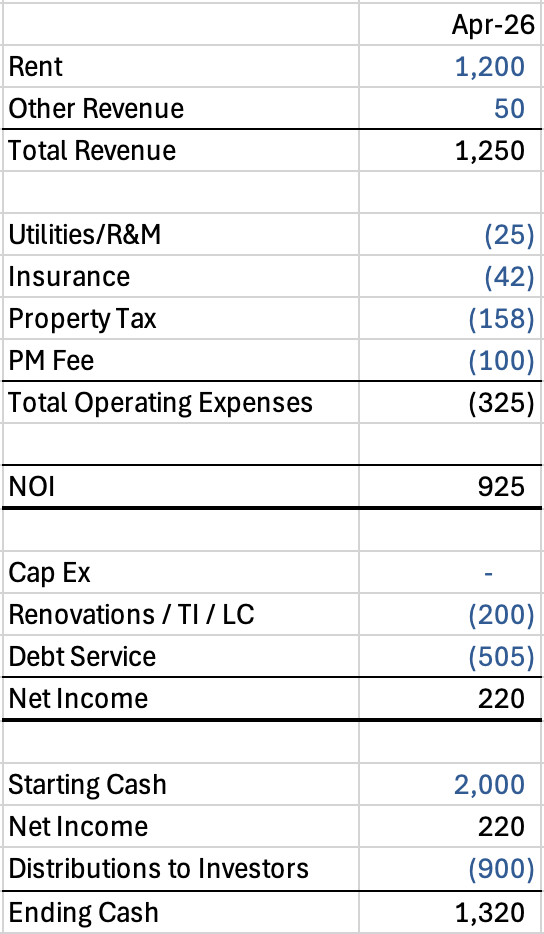

#4 - Cash Flow & Income Statement

Rent rolls and A/R reports are specific to revenue. The cash flow and income statement capture the revenue and expense activity that combine into the net operating income (NOI) and net income.

As an individual investor, I like to think of the cash flow and income statement as a single report.

But those of you who are accountants or in the real estate industry probably recognize that this is not always the case. Here’s how they differ:

An income statement is a summary of activity through NOI and inclusive of debt service, capital improvements (capex), leasing costs (tenant improvements and commissions) that totals in net income. It does not necessarily correlate to (a) the cash activity that occurred at the property that month nor (b) include a starting and ending cash balance.

This is because there are many, many accounting rules that indicate how reports should be prepared. They are anchored on logic that makes sense, but do not always result in helpful information for an individual investor.

Here’s what a cash flow and income statement might look like.

Example: Cash Flow & Income Statement

It looks like an income statement through “Net Income” but then adds comments on the starting and ending cash to give you an ending cash balance.

Cash is king. You always want to know how much cash you have.

A further variation on the income statement would be to include a “comparison to budget”. This would look like the example above with three extra columns:

The budgeted amounts for that month. The monthly budget would have been finalized at the end of the previous year - in this example, the end of 2025.

A comparison of the actual amounts to the budgeted amounts.

Comments on any significant variances to budget.

Now that you have a sense of a cash flow and income statement, let’s move on to the balance sheet.

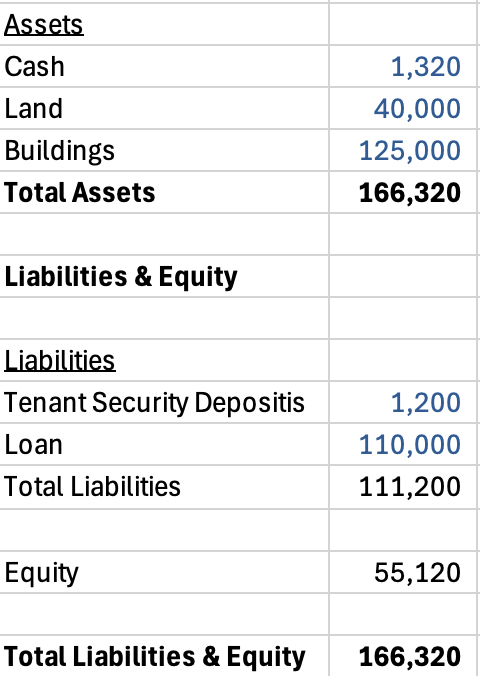

#5 - Balance Sheet

A balance sheet is a snapshot of assets, liabilities, and equity.

Assets are things at the property that have value.

Liabilities are things the property owes to others.

Equity is the difference between the two.

It looks like this.

Example: Balance Sheet

The balance sheet is literal. It must “balance”.

Assets = Liabilities + Equity

Equity = Assets - Liabilities

Balance sheets are helpful to track your liabilities, but I don’t find them particularly useful in my day to day operations of a property.

#6 - Construction Activity & Leasing Report

These last two reports will vary in both who they come from and what they look like.

A construction activity report will likely come from the property manager. It will provide some level of detail on planned, in process, and completed construction activity. It will show things like (i) costs - both budgeted and actual, (ii) timeline - both budgeted and actual, (iii) a narrative on how the work is going.

This will likely be your most important report if you are in the middle of a renovation.

A leasing report will either come from your property manager (all residential properties) or your broker (all commercial properties). It will show leasing activity and lease comparables (aka lease comps).

Lease comps are completed leases at similar properties. They help give you a benchmark of what similar properties are leasing for in the same market. They help you determine what you should charge for rent for your property. We will get into this in a future newsletter.

So what is the takeaway on all these reports?

My Recommendations

Here’s how I use the reports.

For the deals in which I am a limited partner (LP) investor, I read the summary of the report with a focus on what is most important to me. If cash flow (aka investor distributions) is most important, I focus on that.

I recognize that as an LP (a) I have no control over day to day activity nor decision making and (b) I have invested as an LP so I don’t have to do any work. With this in mind, I don’t bother reading much beyond the summary page(s).

If you are an individual LP investor, you will “get what you get” relative to reports from the general partner (GP). Here are three examples of reports I get as an LP investor with three different GPs.

Monthly report an income statement and balance sheet, but with minimal narrative.

Quarterly report with detailed narrative and an income statement.

Annual letter with a narrative only. One page. No numbers.

This does not correlate to the property performance. It is just a choice that each GP has made as to how they want to communicate with their investors. As an LP, I have no ability to change this.

When I am investing by myself or with a partner, I take the opposite approach to reviewing the reporting package.

Not only do I read everything in the report, but I also have my own excel file of (i) monthly cash flow and income statement, (ii) rent roll, and (iii) capex report.

My excel based cash flow and income statement includes both historical and projected amounts per month with a running cash balance so I can project capital spending and investor distributions.

It is more work for me to enter the information from the reporting package pdf into excel each month, but it is well worth the effort as this makes sure I really understand the property financial performance.

A side benefit is that as long as the property manager gives me the information I need to enter into my excel file, I don’t care what format they deliver the reports to me in. They can use their standard templates.

Recognize that if you ask a property manager for customized reports that differ from their standard templates, it may be more work for them. This could mean more costs to you.

Make sure you agree on the content, timing, and frequency of the reporting package before you hire your property manager or accountant. I suggest starting by requesting an example reporting package and seeing if it has the content you need.

Red Flags to Watch For

As you review the reports, here are a list of things to be on the lookout for.

Increasing A/R: this indicates tenants are consistently paying late or not at all. Work with your property manager to come up with an action plan.

Actual Expenses Are Significantly (>10%) Over Budget: either your budget was too low or there are issues going on at the property. Discuss with your property manager.

Minimal Cash Balances: always leave a cash cushion for the unexpected.

Vacant Suites Staying Vacant for 3+ Months: work with your property manager or leasing broker. You may need to lower the asking rate or change brokerage teams.

Construction Delays and/or Cost Overruns: watch this closely and actively manage the team managing the jobs.

Pay attention and don’t be shy about calling your property manager to discuss in detail. Use your common sense and ask questions. Don’t be a jerk, but don’t be too passive.

Your Property, Your Choice

You can decide how you approach each investment.

It is your investment, your money, your time.

And you can always change your approach to report review over time. That is what I did.

How I approach it today is different than I did five years ago and will likely change five years from now.

That is learning and evolution. As my needs change, I adapt my approach to better meet my needs.

Don’t be intimidated by the jargon of real estate reports: income statements, rent rolls, and balance sheets.

Ask your property manager or accountant to explain them to you in simple terms. Take notes. Be a student.

After reading a month or two of reports, you will find they are key to extracting meaningful insight into how your investment is performing.