Property Tax: The Expense That Never Goes Away

The ongoing expense that varies from state to state

Last week we discussed insurance in detail. Today we are getting into property taxes.

My original plan was to do them as a combined newsletter, but when I started writing about insurance I realized just how many layers of information there are.

Why was I planning to cover them in a single newsletter? Because they share multiple similarities:

The amount of each expense is largely outside of your control.

They are generally permanent. You could get rid of almost every other expense, but property taxes and insurance will always be with your property.

They are specialized subjects that benefit from the owner having a certain amount of knowledge and expertise.

But…property taxes are simpler to explain than insurance. Phew!

Today we will discuss:

Why property taxes exist and what they fund.

How they are determined.

Ways to reduce your property taxes.

Owner best practices.

That’s it. Much more simple than insurance.

Let’s dig in.

Why Property Taxes Exist and What They Fund

Property taxes are revenue for the county the property is located in.

Read that word carefully: county. Not the state.

They are the way each county (in each state in the U.S.) funds basic services such as public schools, police, and libraries. A portion of the revenue is sometimes distributed to each city within that county. [Yes, this is a U.S. centric newsletter.]

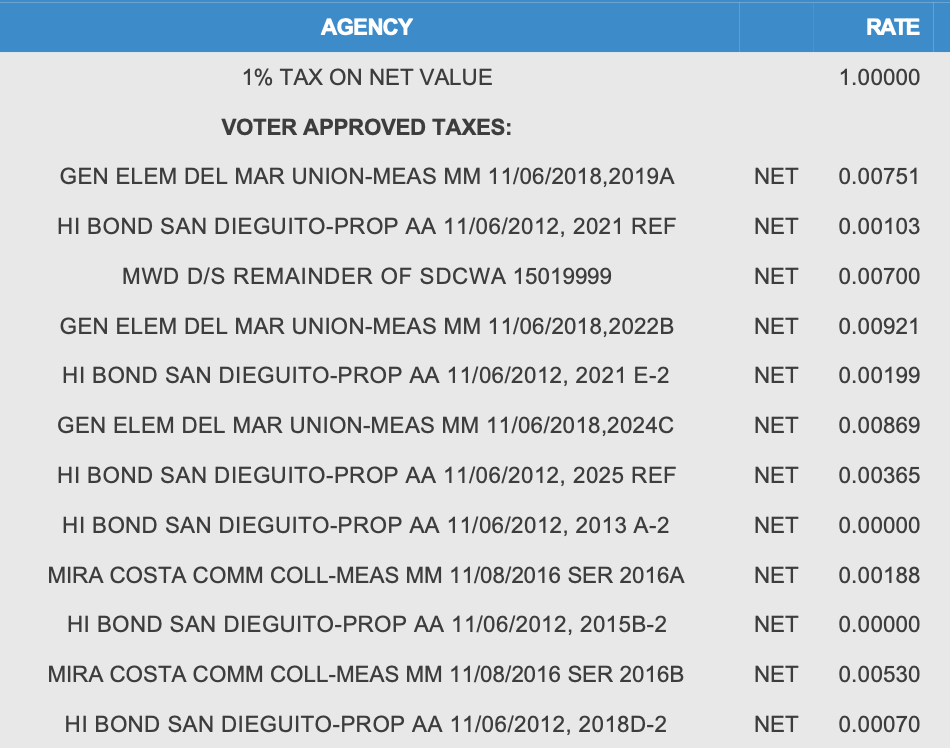

You may have seen a proposition or other measure on your local election ballot that talks about adding an additional fee to homeowners to fund XYZ. If passed, this would add to every homeowner’s property tax expense. Here’s an example of a property tax bill with propositions and measures that passed the voting ballot and were added to each homeowner’s property tax bill:

Table 1: Example of Propositions on a Property Tax Bill (California). Each one increased the “rate”. More on this later.

To add another layer of complexity, property taxes are determined at the state level but administered, collected, and used at the county level.

Your main takeaway should be that property taxes fund your local government and services. They are never going away. All 50 states have some type of property taxes.

But wait - some of you may be thinking that certain states don’t have property taxes. This is not correct. Some states don’t have income taxes or sales tax, but every state has property taxes.

Let’s transition to how they are determined.

How Property Taxes Are Determined

As I said above, every state has property taxes. But unfortunately every state calculates them in a different way.

Here are the similarities across all states:

County Assessor: the team at each county that determines, administers, and collects property taxes.

Assessed Value: the value of the property and land as determined by the county assessor.

Rate: a percentage that is applied to the assessed value to determine the property tax.

Here are the differences:

Assessment Methodology: how the assessed value is determined (generally, but not always, via fair market value appraisal).

Assessment Frequency: how often the assessed value is determined (every 1-4 years).

Payment Timing: frequency and timing of payment throughout year (1-4 times per year).

Payment Period: whether the payment is in advance or in arrears.

Appeal Options: whether and how the property taxes can be appealed with the goal of reducing them.

So we have a basic framework (the similarities), but a unique way of implementing it within each state (the differences).

Here are some examples:

California

Assessment Methodology: the value is determined by the most recent purchase price and then grown at 2% per year. That’s it. Super simple. That is why you hear of people that have owned their property for 30+ years and have a low property tax basis (and expense), while the person next door who recently bought their property has a much higher property tax basis (and expense).

Assessment Frequency: July 1 every year add the 2% increase and adjust for propositions and measures.

Rate: a little over 1%. Example: $1,000,000 x 1.132% = $11,320.00 per year.

Payment Timing: twice per year in December and April.

Payment Period: December covers the second half of the year (7/1 to 12/31). April covers the first half of the year (1/1 to 6/30).

Appeal Options: through property tax consultants, who do not need to be licensed.

Texas

Assessment Methodology: fair market value appraisal.

Assessment Frequency: beginning of each year.

Rate: changes each year.

Payment Timing: January of the year after assessment.

Payment Period: 100% in arrears.

Appeal Options: typically through a lawyer.

These are just two examples. Each of the 50 states in the U.S. has a different approach.

Ways to Reduce Your Property Taxes

There are ways to appeal and reduce your property taxes. Why would you want to do this? To reduce your operating expense. And you may feel the assessed value is unreasonable.

If you own properties in multiple states with different rules, it may be helpful to use a property tax consultant such as Ryan.

The typical structure will be that they work on 100% contingency. They only get paid if your property taxes are reduced. Example: they might keep 10% - 30% of the reduction as their fee.

My personal opinion is that property tax consultants serve an important role in the industry as this is a specialized area of expertise that varies from state to state. These consultants can help save you money and estimate your future property taxes for properties you are purchasing.

My approach has been:

Personal Home: I appealed this one myself because (i) I understood the California process and (ii) I live in a 100+ home community where the homes are very similar, making it easy to supply sales comparables. I had bought my home a couple years before the Great Financial Crisis of 2008. By successfully appealing my property taxes, I saved quite a bit of money each year.

Industrial Portfolio: when I worked for a company with 100+ properties across many states, we used property tax consultants. It was too complex and labor intensive to justify using one of our internal team members.

Educate yourself by talking with a property tax consultant. If you own a small property (less than $5M), find a smaller local property tax consultant who may give you more focus than a larger, national firm.

Owner Best Practices

Here are my recommended best practices when working on property taxes for your investment property.

Due Diligence & Underwriting - Assessment Methodology

Remember, these vary from state to state. Don’t assume the seller’s property taxes will be your property taxes growing at inflation each year.

Do the research and/or talk to a property tax consultant before you commit non-refundable money towards the purchase of the property. You need to understand how they will change during your ownership.

Propositions & Measures - Expiration Dates

These often have an expiration date. This is especially important when you see a very large additional charge on a property tax bill.

My former company once bought a property where the additional charges were as much as the base property tax bill. This was related to a fee that would expire two years after our acquisition. Knowing the near term expiration changed the way we thought about the deal.

Closing Statement - Payment Timing

The timing of the payment will determine how the property tax expense is prorated in the closing statement on closing day. This could be a big charge or credit.

For example, if property taxes are paid in advance, you (as buyer) could find yourself owing the seller for their prepayment and have to pay this amount through the closing statement.

What would this mean? You could be short on cash on the day of closing. Understand this in advance to avoid surprises.

Appeals

Be proactive. It doesn’t cost you anything to have a conversation with a property tax consultant. If there is a way to save money on your property taxes, you should consider this.

Pro tip: there is usually a deadline by which you must file the appeal. Do the research so you don’t miss it.

Remember, property taxes vary from state to state. Take the time to understand how things work in the state you are buying the property.

As always, have a learning mindset. Be patient. Talk to experts. Take the time to understand it.