Closing Day: What to Expect

Documents, money flow, and key takeaways for your first closing

Over the last four weeks we have covered four topics on acquiring (aka buying) an investment property.

Now we are going to get into what happens during the actual closing, when ownership transfers from the seller to the buyer.

This will be the 5th and final newsletter on the acquisition process. Next week we will transition to how to own and manage your property.

Last week’s discussion on debt was long. This one is going to be shorter as it is a fairly straightforward process with far fewer moving parts.

Essentially, the closing process involves two things:

The exchange of money.

The signing of documents to legally transfer ownership.

Let’s dig in.

What is Closing?

When I talk about “closing”, I am referring to the day in which money and ownership transfer between the seller and the buyer.

Due diligence has been completed.

The buyer has gone non-refundable with their deposit and the closing date is here.

What happens next?

Here’s a typical closing timeline:

3-7 days before: finish up loan documents.

1-3 days before: sign documents.

0-3 days before: buyer and lender wire money into escrow. Bind insurance.

1 day before: final review of closing statement.

Closing day: last minute document signing and any other issues.

0-2 days after: notify tenants and vendors; record deed with the county.

The actual “closing day” can be anticlimactic as it may feel like you are just waiting for the escrow officer to say “we are closed”.

The Role of Escrow

As discussed in Demystifying Real Estate Purchase Agreements, the escrow officer at the escrow company plays the “referee” and lead coordinator of the sale process.

They make sure all the documents get signed and sent to them.

They arrange the legal recording (aka evidence) of the sale.

They also hold and distribute the money.

In short, they make it all happen.

Documents Get Signed

As also discussed in Demystifying Real Estate Purchase Agreements, there are a number of “form” documents that were agreed to in the purchase and sale agreement (“PSA”) and added as exhibits.

These “form” documents are then used as templates to create the actual documents that formalize the sale.

They include:

Grant Deed: this is the legally recorded document that confirms the property has been sold. Recording the document with the local municipality allows everyone to see that the property has been sold.

Bill of Sale: this documents the sale of any personal property related to the physical property. Examples: parts and materials for repairing the property such as flooring or light bulbs.

General Assignment: this documents the transfer of the various contracts such as leases, warranties, and service contracts.

There may also be other documents signed such as the one that notifies the county property tax assessor of the sale.

If the buyer is getting a loan to buy the property there will also be:

Deed of Trust: the legally recorded document that shows there is a loan on the property.

Loan Agreement and related documents: each lender has their own set of documents that they like to use.

In addition to documents getting signed, money will need to change hands.

Money Exchange

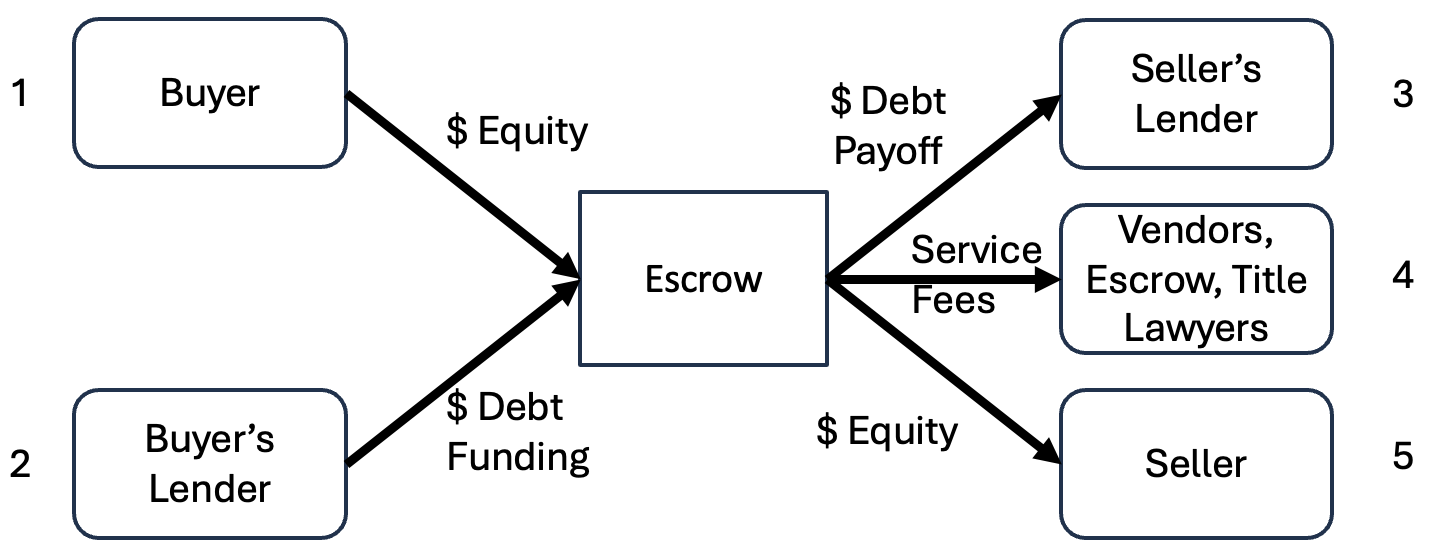

If both the buyer and the seller each have a loan on the property, then there will be five parties giving and/or receiving money.

These are the parties and this is the typical order in which money flows. Everything goes through escrow.

$ Into Escrow: Buyer sends in their equity.

$ Into Escrow: Buyer’s lender sends in their loan funds. They want to see the buyer’s money in first.

$ Out of Escrow: Seller’s lender receives money to pay off the seller’s existing loan on the property.

$ Out of Escrow: Payments to inspection vendors, escrow, title, and lawyers.

$ Out of Escrow: Seller receives the balance of the sale proceeds.

Here’s a diagram to help you understand.

Diagram: Flow of Money at Closing

Escrow officers make it all happen.

Closing day is stressful for all parties. Escrow officers live this every day! Be kind and patient with them.

Let’s move on to another critical component relative to money moving around: closing statements.

Closing Statements

Closing statements show who is getting paid what. There will be at least two closing statements:

Buyer’s Closing Statement

Seller’s Closing Statement

Think of them as an excel sheet showing “charges” and “credits” and ending in a total of how much the buyer and seller will owe and receive, respectively.

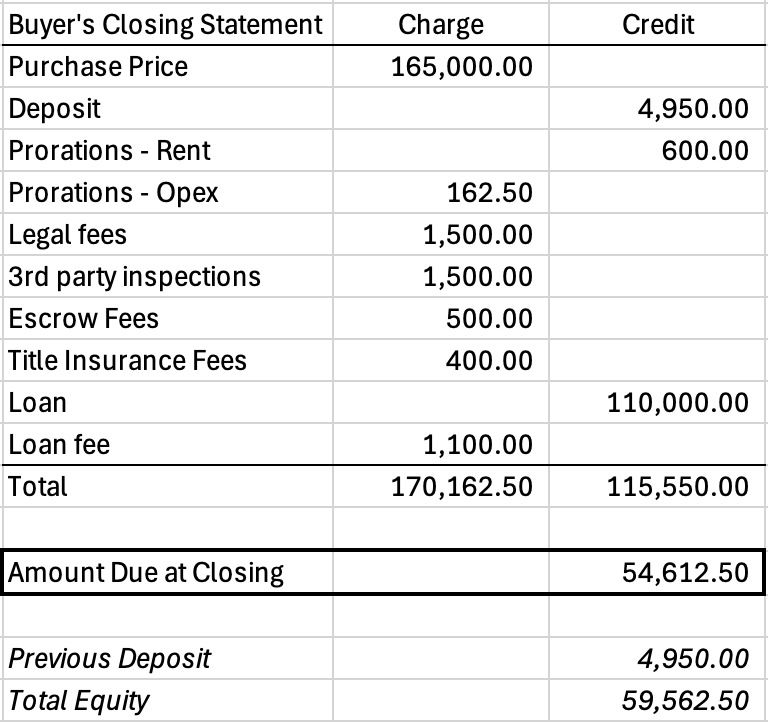

Ex. Buyer’s Closing Statement

Charges (amounts buyer has to pay)

Purchase price

Legal fees

3rd party fees for inspections

Escrow and title fees

Loan fees

Prorations*

Credits (amounts that reduce the buyer’s cash needs to close)

Deposits already made during due diligence

The loan

Prorations*

Total: at the bottom it will show how much cash the buyer will need to send into escrow to be able to close the deal.

*See discussion below for the meaning of “prorations”.

Here’s what the math would look like based on our ongoing example discussed in previous newsletters.

Diagram: Example Buyer’s Closing Statement

The amounts in italics would not be part of the closing statement. I added it to show the total equity the buyer actually funds which is:

$54,612.50 - amount due at closing to escrow

$ 4,950.00 - previously paid deposit

$59,562.50 - total equity paid to escrow

So why doesn’t it equal exactly $60,000 from our previous newsletter discussions?

Because of “prorations”.

Prorations

Prorations are the split of rent and operating expense between the buyer and the seller based on (a) the days of that month the buyer and seller will each own the property and (b) the timing of the rent or expense.

Simple example used in the closing statement above: you close on June 16th, halfway through the 30 day month.

Rent Proration

Tenant paid $1,200 rent to the seller on June 1st.

But the buyer (you) owns the property June 16th to 30th (16 days).

Seller owes you the rent for your 16 days: $1,200 x 16/30 = $600.

This $600 is credited to you on the closing statement.

Operating Expenses

Buyer paid $625 in operating expenses on June 1st.

But the buyer (you) owns the property June 16th to 30th (16 days).

You owe the seller for your 16 days: $625 x 16/30 = $162.50.

This $162.50 is charged to you on the closing statement.

Here are some things to note on these calculations:

Buyer’s ownership of the property starts on the day of closing, in this example the 16th of a 30 day month.

Prorations are based on amounts actually collected (rent) and paid (operating expenses) by the seller. If the tenant hasn’t paid the rent yet that month, the rent is not prorated. This often happens when the closing occurs in the first five days of the month. Same concept for operating expenses.

Insurance is not included in the proration as the buyer will need to get their own insurance. This is often paid through closing. Ask your insurance broker as the amount paid through closing will often be 6-12 months of premiums.

Not all operating expenses are paid monthly. This is especially true for property taxes. The proration will be adjusted for the timing of the payments.

Don’t worry if this is confusing. The escrow officer will do all the math.

What Happens Immediately After Closing

Once closing is complete, a number of things will happen right away.

Receive keys or access codes

Change locks (important for security)

Transfer utilities to your name

Contact tenants to introduce yourself and send them notices with contact information and rent payment instructions

Set up property management/accounting and maintenance vendors

This is because YOU are now the property owner!

Congratulations!

So what do you takeaway from all of this?

Key Takeaways

The closing process is when multiple parties come together to formalize the closing. Here’s what you should remember.

The escrow officer makes it all happen. They are the referee and the coordinator.

You will need to sign many documents: make sure your government-issued photo ID is current. Documents include:

One set to buy the property.

One set if you are getting a loan on the property.

Be 100% available the day before and of closing. There are often last minute documents that need to be signed. Sometimes they cannot be signed electronically, so it is ideal to have a local escrow company.

Many closings now happen remotely using electronic signatures and wire transfers. You may never meet your escrow officer in person. This is normal and perfectly safe - just verify wiring instructions carefully.

Scammers impersonate escrow officers and send fake wiring instructions. ALWAYS call your escrow officer at a verified number to confirm wiring details before sending money. Never rely on emailed wiring instructions alone.

The amount of cash you send to escrow will likely be different than the amount you have in your internal analysis. The difference will be prorations. Most of the time this is a minor issue, but property tax prorations can be big. So can the initial insurance payment. Talk to your escrow officer well in advance to understand this. You can also do the math yourself.

As discussed last week in the newsletter on debt, lender reserves can significantly reduce the amount of initial funding from the lender. A $110,000 loan with $10,000 of reserve holdbacks will only result in $100,000 of funds at closing. Read the loan documents. Understand this in advance. It is no fun to be jammed on the day of closing by not having enough cash to close because of reserve holdbacks by the lender that you should have known about.

Closing can get delayed for multiple reasons: title issues, lender funding delays, missing signatures, wire transfer problems, and other last minute issues. As long as all parties are reasonable and want to make the deal happen, you will be able to overcome these issues.

Stay calm and carry on. It will be stressful, but you will get through it. Don’t get frustrated and send a nasty email you will regret.

You’ve got this.

Follow the lead of your escrow officer (and lawyer if you are using one).

You will complete the closing and own your first property.

Owning the property is where the fun and work really begin.

That is the series we will begin next week.