Due Diligence: Your Property Investigation Checklist

What to review before your deposit goes non-refundable - from leases to roofs

Due diligence.

Another piece of jargon from the real estate industry.

What does it mean?

In plain English:

Due diligence is the process of doing the investigative work to determine if what you think you are buying is what you are actually buying.

It is a way to minimize risk and avoid costly surprises.

If you are buying a 1-4 unit residential property, it is known as your inspection period.

If you are buying a commercial property, it is known as due diligence or “DD”.

You do this in the period of time before your deposit goes non-refundable, as detailed in last week’s discussion: Demystifying Real Estate Purchase Agreements

If you have bought a used car, you have experienced due diligence. You take the car for a test drive. Hopefully you followed up with an inspection or at least outsourced the inspection process by buying a “certified pre-owned” car from a dealer who completed the inspection. Maybe you even read the Carfax report.

All of this was done to determine if the car would drive OK once you owned it.

Same concept with buying real estate.

You want to make sure that you do what you can to confirm your investment property will perform as you expect it to perform.

How do you do this?

I like to use a simple cash flow statement to determine what to look for. Think of the cash flow statement as your guidebook.

By tying (almost) everything back to the cash flow statement, you minimize the risk of surprises.

Today we’ll cover:

How to use a cash flow statement as your due diligence guide

What to review for revenue (rent, vacancy)

What to check for operating expenses (utilities, insurance, property taxes, management fees)

How to evaluate capital improvements (capex, renovations, tenant improvements)

Non-cash flow items (zoning, title, environmental)

Simple vs. complicated properties

Let’s dig in.

Reminder: Refundable vs Non-Refundable

Last week we talked about the difference between the refundable (aka contingency) and non-refundable period. Let’s anchor on this concept again.

Refundable: From the date the Purchase & Sale Agreement (“PSA”) is signed through the expiration of the due diligence period, the buyer can typically back out of the deal for any or no reason and get their deposit back. No penalty. No foul. They still have to pay the consultants and advisors they may have hired and their reputation may suffer, but they don’t have to buy the property nor forfeit their deposit.

Non-Refundable: Once the due diligence period expires, everything changes. The buyer can still back out of the deal, but doing so will mean they lose their deposit.

Due diligence is one of the most important things the buyer does during the refundable stage of the acquisition process.

Cash Flow Statement as a Guide

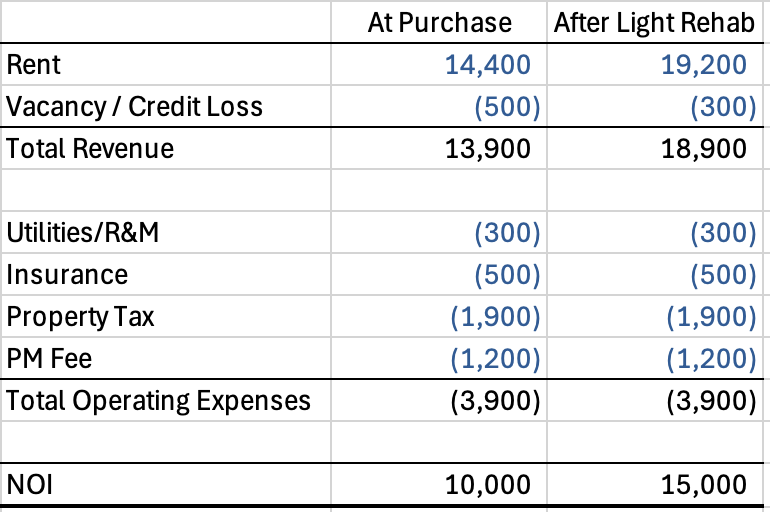

Let’s continue our property example from one of my previous newsletters: Unlocking Value: What to Do After You’ve Improved Your Property. You are buying a property with $10,000 of net operating income (“NOI”). You believe you can perform a $30,000 light rehab to increase the NOI to $15,000.

In the table below, I have expanded our example to include some assumptions on the revenue and expenses to build up to the NOI.

Revenue less operating expenses = Net Operating Income.

Table: Light Rehab Property - Annual NOI Comparison

Let’s define each line item.

Revenue

Rent: what is paid by the tenants under the leases.

Vacancy / Credit Loss: an assumption that the property will not be leased the full year and/or the tenant will not pay rent and you will need to evict them at some point.

Operating Expenses

These are your recurring costs to operate the property, regardless of whether you have a loan on the property or not.

Utilities: any utilities the tenant doesn’t pay. Remember that you will have to pay utilities in the time between one tenant moving out and the next one moving in.

Repair & Maintenance (“R&M”): you may need to pay for some costs even if the tenant is leasing your property. Example: plumbing repairs.

Insurance: property and liability insurance.

Property Taxes: these are determined by the state and county in which the property is located.

Property Management Fee (“PM Fee”): if you are using a 3rd party to manage the property, you will need to negotiate what fee you pay them. Some GPs choose to act as the property manager and charge a PM fee.

Let’s run through how we can use this as a guide for our due diligence.

Revenue: Rent

There are two ways to look at rent: in place and market.

In place rent is determined by any leases for current tenants. The due diligence process involves reading the leases to confirm the rent and rent increases, any additional rent charges (ex. monthly utility reimbursements), the lease expiration, and any renewal options.

You will also want to note any landlord obligations (ex. replacing an HVAC unit by a certain date), any tenant obligations, and any other items that could affect the performance of the property.

Ideally you will want to interview the existing tenants to ask them how they like the property and if there are any problems with it and/or the landlord.

Market rent is totally different.

You will need to talk with brokers to get their opinion of market rent. In the example above, you are doing the light rehab so you want to talk with multiple brokers to get their opinion on what they think the property will lease for after you complete the light rehab.

Revenue: Vacancy / Credit Loss

Understanding the market and the likelihood (and duration) of vacancy will come from your conversations with the brokers. Simply ask: “How long do you expect the property to be vacant after I complete the light rehab?” By asking multiple brokers the same question, you will develop your own opinion.

Credit loss will be a combination of (a) reviewing the rent payment history of the existing tenants and (b) making an assumption. To review the existing tenants, the seller should provide you an “accounts receivable” report showing any rent that hasn’t been paid by the existing tenants. This is often referred to as the “A/R report”.

Ideally you also get a copy of the “tenant ledger” for the last 3-12 months which shows the payment history and timing of all tenant charges and payments, regardless of whether they currently owe delinquent rent or not. This is key to seeing when the tenants pay each month.

Your loan payment will likely be due in the first 5-10 days of the month. If your tenants don’t pay until the 20th, you will need to build up more cash to be able to pay the loan payment before you get the rent.

Operating Expenses: Utilities, R&M

These are determined by multiple methods:

Review of the seller’s historical income statements: ideally past two years. You want to see what has been paid in the past to determine the future.

Review of any service contracts in place. Examples: pest control, landscaping. The contracts will list the monthly payments amounts.

Review of historical utility statements. This will allow you to see the seasonality of the charges so you can do a monthly cash flow. It will also show you if there were any unusually high or low months. You will want to investigate these. Example: there may have been a water leak that caused the water bills to be high one month.

Operating Expenses: Insurance

You will need to get your own insurance for the property. You can’t use the seller’s insurance. Get quotes for property and liability insurance from an insurance broker. Property insurance if for physical damage to the buildings. Liability insurance is to protect you if get sued.

Operating Expenses: Property Taxes

Property taxes are determined by each state and administered at the county level.

Each state has a different method of calculating property taxes as well as a different frequency at which the amount of the property taxes are both paid and recalculated (aka re-assessed).

Review the seller’s property tax bills. Talk with the county assessor’s office and/or a property tax consultant to determine the specifics of that state and county.

Don’t assume your property taxes will be the same as the seller’s. Every state has different rules.

Operating Expenses: Property Management Fee (“PM Fee”)

The amount of the PM fee will be based on a new contract you negotiate with whomever you hire to manage the property and do the property accounting. It could be the same party as the seller used. It could be a new group.

Fees range from 1% - 8% of revenue depending on the size and complexity of the property.

NOI = Revenue minus Operating Expenses

That’s it.

You have done the due diligence to validate NOI. Well done!

But we are not finished yet.

Now let’s move on to the “below the NOI” items by discussing capital improvements.

Capital Improvements

Capital improvements are physical improvements to the buildings. They fall into three main categories:

Capex: repairing or replacing existing building systems such as the roof or HVAC in a “like for like” way.

Renovations: upgrading the existing building with light rehab or value add improvements.

Tenant Improvements & Leasing Commissions: costs to customize a space for a specific tenant and pay a broker commission for finding the tenant.

Capex

Due diligence is done on capex by:

Hiring consultants to review the existing building systems.

Getting bids from contractors for specific work.

Some consultants specialize in property condition assessment (aka property inspection or PCA) reports. They will give you an overview of the condition of the property with rough cost estimates by year.

But they won’t actually do the work to repair the property.

You need to get specific bids for the work from someone who will actually do the work.

This is key.

If the PCA says the roof needs to be replaced in the first three years, talk with a roof vendor to confirm this assumption and tell you how much it will actually cost if you engage that roof vendor to do the work.

This is where you get real pricing.

Renovations

You have a plan for what you want to do in your light rehab. Hopefully you validated and/or evolved it by talking with local brokers.

Now you need to price it out.

Just as you did with the roof vendor, meet with a contractor who will price out the light rehab and tell you a realistic time frame to complete the work.

Tenant Improvements & Leasing Commissions

This also comes from conversations with local brokers.

1-4 Unit Residential & Multifamily: there will be no or minimal tenant improvement.

Commercial (office, retail, and industrial): tenant improvements are very common. So are leasing commissions. Talk with local leasing brokers to develop realistic estimates. These are often significant ongoing costs for office and retail properties.

Non-Cash Flow Due Diligence

Although everything has the risk of ultimately impacting the property cash flow, there are some items that fall outside our “cash flow statement as a guide” concept.

These generally have the commonality of making sure you can operate the property as expected without interruption from the local municipality.

Zoning: check with the city to confirm the legal zoning for the property and that the property you are buying conforms with that zoning.

Title: most properties have some legal rights placed upon them by 3rd parties. Example: the local utility may have an easement to bring their electric lines to your property. The title report and the ALTA survey will tell you these.

Environmental: if you are buying an industrial or retail property, getting an environmental report is critical. You want to see if there are any issues (ex. old dry cleaner or manufacturer that contaminated the soil). There are consultants that specialize in this and create a “Phase I” report to summarize the environmental condition of a property.

Bringing it All Together

If this feels to you like a lot to review, then you are correct. It is a lot.

A typical due diligence timeline might be:

Week 1: review materials, order reports (PCA, title, environmental)

Week 2: property inspections, broker interviews

Week 3: review reports, contractor bids

Week 4: update your financial analysis and make final decisions

Things move fast. You owe it to yourself to be thorough so you need to be focused, prepared, and methodical. Don’t cut corners.

Here are some common issues that might come up in your due diligence:

Major capex discovered (immediate roof replacement)

Tenants not paying rent (A/R report shows major delinquencies)

Zoning violations (the property cannot be operated as is)

Environmental contamination (discovered in the Phase I report)

Title problems (liens, easements that restrict use)

Sometimes these can be negotiated with a price reduction or time to fix an issue. Sometimes they kill a deal.

If you find a problem, be transparent and solution oriented with the seller. You want to find solution that works for all parties.

Do I Really Have the Time for This?

If you are intimidated by the time involved, note that not all properties require the same level of time in your due diligence review.

Let’s give two examples.

Simple: 2-Unit Residential in Established Neighborhood

Revenue: there are just two leases to review. It is in a neighborhood with a lot of similar properties, some of which have been rehab’d and some of which have not. There are lots of similar properties to reference and talk with brokers about.

Capital Improvements: all you really need to do is confirm the condition of the property and price out your light rehab.

Non-Cash Flow Due Diligence: this will be straightforward as there shouldn’t be any issues.

Complicated: 50 Year Old Industrial Building with 50+ Tenants

Revenue: lots of leases to review. If the units are different sizes and configuration, determining market rent for each will also be complicated.

Capital Improvements: the building systems are old. There may be a variety of tenant improvements that are unique for each suite.

Non-Cash Flow Due Diligence: this could be complicated. Zoning may have changed over time. There is also risk of environmental issues.

In the simple example, you should have plenty of time to complete the due diligence before the period expires.

In the complicated example, you will be working non-stop to get it done.

Walk Before You Run

If you are new to real estate investing, start simple.

The complicated example may look attractive from a theoretical cash flow perspective, but the due diligence will be hard and full of risk for a new investor.

And remember, there are other things you will need to do before your due diligence period expires.

If you are getting a loan to buy the property, this will consume a lot of your time. You need time to figure this out and get the right loan.

Set yourself up for success by starting with a simple property.

Get in your reps.

Become an expert in due diligence.

What you learn in the due diligence process will form the foundation of your understanding of the property and pay dividends in the future.

Take the time to do it right.

For those of you that want to dig deeper, there are more resources on my downloads page.

Professor Bateman