Unlocking Value: What to Do After You’ve Improved Your Property

Cash flow, sale, or refinance—which monetization strategy fits your goals?

Let’s fast forward a bit and have some fun.

Imagine you have made your first investment. It has gone well.

You've done everything right—bought smart, improved the property, and now it's cash flowing.

Well done!

Your hard work, patience, and perseverance have paid off. Maybe there was even a little luck along the way.

But here's the question most investors face next: how do you actually get your money out?

There are three main ways to do this:

Enjoy the cash flow.

Sell the property.

Cash out refinance.

Each way has its pros and cons. The decision of what to do depends on the goals you are trying to achieve, which may change over time.

Let’s dig in.

Your Real Estate Investment Example

Let’s create an example to use in explaining and evaluating the three ways to monetize your investment. The math will tie to my previous post: Cap Rates: The Simple Math of Real Estate Investing

Here’s the example:

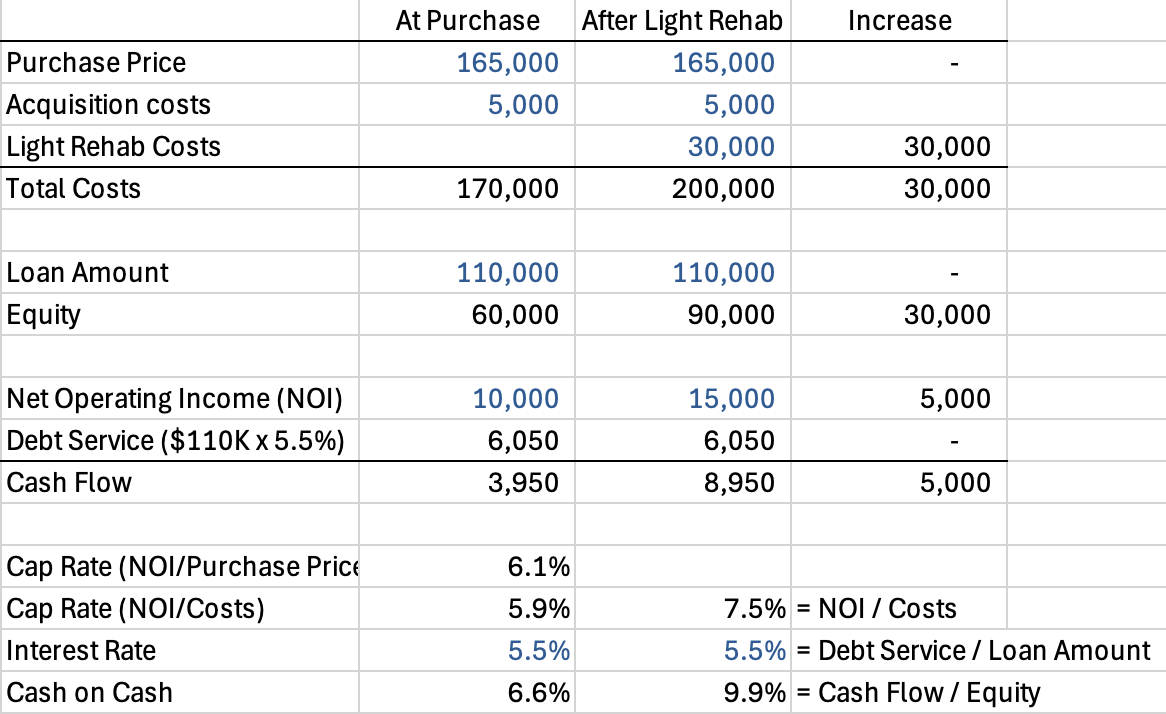

A little over two years ago, you bought a property that was 100% leased to one tenant with two years left on the lease. The NOI at time of purchase was $10,000.

You bought the property for $170,000 including your closing costs. After securing a $110,000 loan with a 5.5% interest rate, your equity was $60,000.

$170,000 - $110,000 = $60,000

The property was old and in need of some cosmetic repairs. As it was fully leased when you bought it, you waited patiently until the lease expired to completed your light rehab.

You spent $30,000 to do a light rehab (paint, carpet) and paid a commission to a broker to find a new tenant. Because the loan amount is fixed, the $30,000 cost increased your equity (aka cash investment): $60,000 original equity + $30,000 light rehab and commissions = $90,000 total equity.

After the light rehab, you were able to increase the NOI to $15,000.

Here’s a summary table to help you keep track of everything.

Real estate investment example cash flow

So what do these calculations tell us?

Cash Flow Increase

By spending a one-time cost of $30,000 for the light rehab and commissions, you went from $3,950 per year of cash flow to $8,950 per year. $30,000 to get $5,000 more per year? Well worth it.

NOI Increase = Value Increase

You have increased the NOI. NOI is a key metric buyers and lenders use to value a property. To oversimplify a bit, the value of the property has increased.

Why is this oversimplifying?

Because cap rates can go up and down depending on overall market sentiment, independent of your individual property.

For this discussion, let’s assume they stayed fixed.

Monetizing Value

Now let’s get into the fun part. How do you turn our hard work into cash? Said another way, how do you “monetize” the increase in value?

There are three main ways to do this:

Enjoy the cash flow.

Sell the property.

Cash out refinance.

Each way has its pros and cons. The decision of what to do depends on the goals you are trying to achieve, which may change over time.

Monetizing Value: Enjoy the Cash Flow

The first way is the most straightforward and passive: do nothing and enjoy the increased cash flow.

The $8,950 cash flow per year after light rehab on your $90,000 of equity is a 9.9% annual cash-on-cash return. Much of it is shielded from tax by depreciation. See 5 Tax Advantages That Make Real Estate Investing So Powerful.

If you are a cash flow investor like I am, this may be the best fit for you.

Monetizing Value: Sell the Property

Properties are typically sold based on a capitalization rate (cap rate). In this case you bought the property for a 6.1% cap rate: $10,000 NOI divided by $165,000 purchase price = 6.1%.

Let’s assume you can sell the property for the same 6.1% cap rate. $15,000 post light rehab NOI divided by 6.1% = $245,902.

This gives you a profit before commissions, closing costs, and income tax of $45,902. $245,902 - $200,000 total costs. Not a bad return in two years for your equity investment of $90,000.

If you are focused on increasing your total net worth as much as possible, this could be the path for you. You could consider a 1031 exchange to defer the taxes as I discussed in 5 Tax Advantages That Make Real Estate Investing So Powerful.

Monetizing Value: Cash Out Refinance

Refinancing the property could be a way to have the best of both worlds.

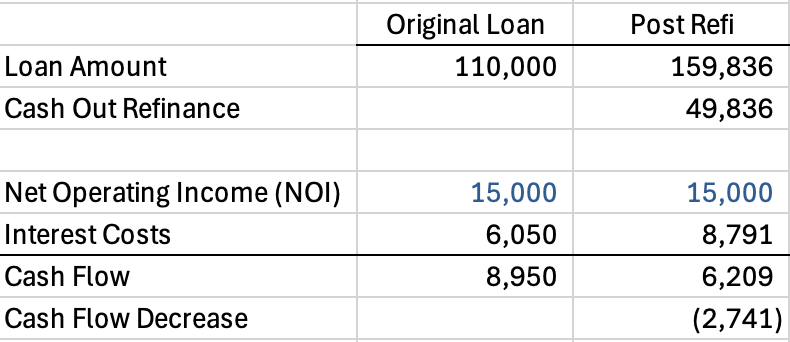

The increase in NOI will likely allow you to put a bigger loan on the property. Your original loan of $110,000 was approximately 65% of the purchase price.

Using the same 65% on the new market value we calculated above ($245,902) would give you a new loan of just under $160,000. $245,902 x 65% = $159,836. This new loan amount is almost $50,000 more than your original loan.

Doing this is known as a “cash out refinance”. There is no tax on the $50,000. You could use it to invest in a new property.

Important Caveat: Not all lenders will immediately give you a cash out refinance. Every situation is different so talk with multiple lenders.

Remember than your interest costs will go up and your cash flow will go down. If we assume the same 5.5% interest rate, your annual cash flow drops from $8,950 to $6,209.

Refinance example

You also have higher fixed expenses with the new interest costs. This gives you less cushion if you lose the tenant and/or the economy gets bad.

A cash out refinance is a good option for investors who want the best of both worlds (and are comfortable with higher fixed expenses): ongoing cash flow and additional money to invest in the next deal.

Monetization Options: Sale vs Cash Out Refinance

In this example, the cash out refinance proceeds ($49,836) are more than the sales proceeds before closing costs and commissions ($45,902).

This is not always the case.

Interest rates and cap rates regularly move around depending on market conditions and market sentiment. If you are on the fence of which option is best for you, educate yourself by talking with brokers on market cap rates and lenders (or debt brokers) on loan options.

Monetization Options: Pros and Cons

So let’s put it all together to see what the best fit for you is.

Enjoy the Cash Flow

Action: none; enjoy the additional cash flow.

Pros: passive; no further execution risk.

Cons: minimal current cash compared to a sale or cash out refinance.

Good for: investors focused on cash flow.

Sell The Property

Action: sell the property.

Pros: ability to unlock value and 1031 exchange into a new property to repeat the process of a new strategy on a new property.

Cons: execution risk on the sale; sale commission costs; tax exposure if no 1031 exchange.

Good for: investors focused on creating maximum wealth by buying and adding value to multiple properties over time.

Cash Out Refinance

Action: refinance the property with a larger loan.

Pros: ability to unlock value without paying taxes and continue to benefit from (a reduced) cash flow; the proceeds from the cash out refinance could be used to buy a new property.

Cons: execution risk on the refinance; transaction costs of refinance; risk of having more debt and interest expense.

Good for: investors wanting to balance ongoing cash flow and ability to grow their real estate portfolio by buying new properties.

What Worked for Me

As with my investing strategy, my monetization strategy has changed over time.

Stage I (Years 1-10+): Buy > Add Value > Sell > Repeat

I was all about maximizing the power of the limited funds I had. The goal was to create value, sell a property, and invest it in a new one. This was an effective method to build wealth. I still have a number of investments that fit this strategy.

Stage II (Years 10+): Enjoy the Cash Flow & Cash Out Refinances

Once I had built wealth, or at least could see a path to that future with my existing investments, I started to be more focused on cash flow. I was able to build up a combination of assets under two strategies:

Cash Flow: I have one property that I own debt free. The strategy is focused on consistent cash flow.

Cash Out Refinance: Buy > Add Value > Cash Out Refinance > Repeat. The LP investments I have follow this strategy. I use the cash out refinances to buy more cash flowing assets.

These stages have worked well together. I wouldn’t have been able to focus on cash flow investing without the capital I built up through selling properties.

Finding the Monetization Option That Fits You

Let’s think about what might work for you.

Situation A: Limited Capital, Long Time Horizon

This is likely your situation if you are early in your career. You are rich in time, energy, and health, but poor in money. You have a long time horizon for the power of compounding to go to work.

The buy, add value, sell, and repeat is a path that could allow you to turn your limited funds into something more meaningful.

Situation B: Some Capital, Shorter Time Horizon

Maybe you are exploring real estate investing for the first time later in life. Your time horizon to retirement, or at least leaving a W-2 job, is shorter. You have worked hard and saved a decent amount of capital to invest.

In this case a combination of enjoying the cash flow and cash out refinances may be a better fit for you.

What is Right for You?

I have seen investors follow each of these paths successfully. It all depends on your available capital, time horizon, and goals.

Do you have an investing story that you are willing to share with me? Email me at bateman@creprofessor.org. I read every email and would like to hear from you.

Professor Bateman