Unlocking Value: What to Do After You’ve Improved Your Property

Cash flow, sale, or refinance—which monetization strategy fits your goals?

Let’s fast forward a bit and have some fun.

Imagine you have made your first investment. It has gone well.

You've done everything right—bought smart, improved the property, and now it's cash flowing.

Well done!

Your hard work, patience, and perseverance have paid off. Maybe there was even a little luck along the way.

But here's the question most investors face next: how do you actually get your money out?

There are three main ways to do this:

Enjoy the cash flow.

Sell the property.

Cash out refinance.

Each way has its pros and cons. The decision of what to do depends on the goals you are trying to achieve, which may change over time.

Let’s dig in.

Your Real Estate Investment Example

Let’s create an example to use in explaining and evaluating the three ways to monetize your investment. The math will tie to my previous post: Cap Rates: The Simple Math of Real Estate Investing

Here’s the example:

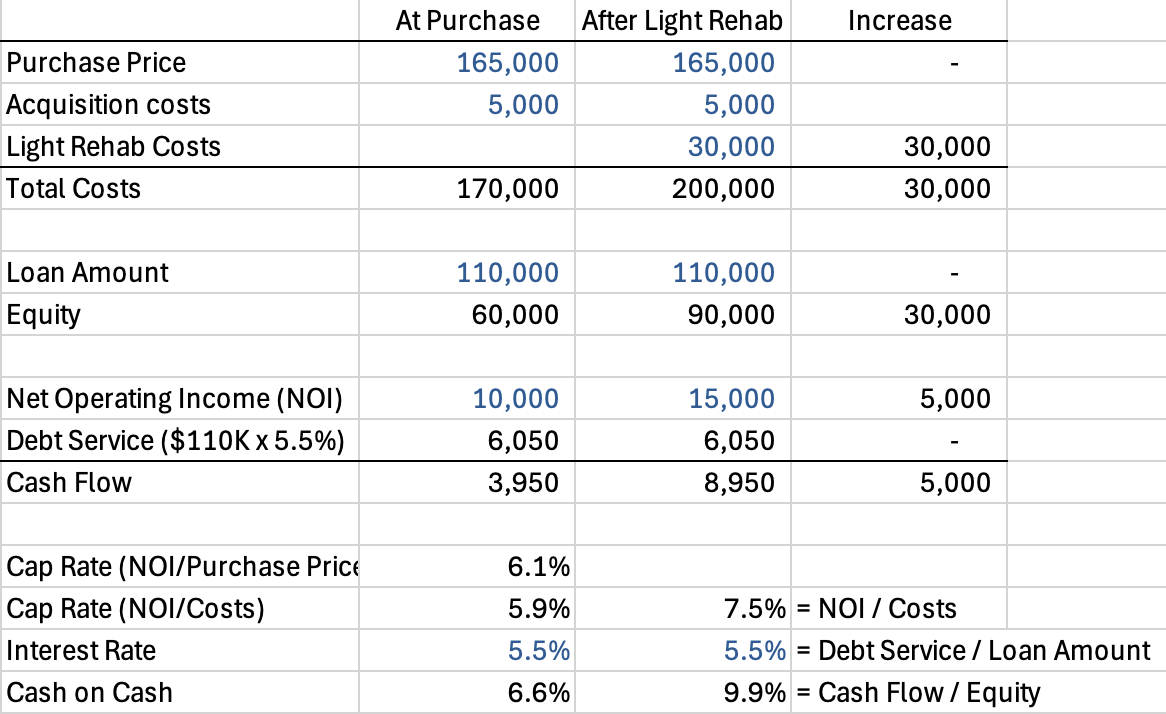

A little over two years ago, you bought a property that was 100% leased to one tenant with two years left on the lease. The NOI at time of purchase was $10,000.

You bought the property for $170,000 including your closing costs. After securing a $110,000 loan with a 5.5% interest rate, your equity was $60,000.

$170,000 - $110,000 = $60,000

The property was old and in need of some cosmetic repairs. As it was fully leased when you bought it, you waited patiently until the lease expired to completed your light rehab.

You spent $30,000 to do a light rehab (paint, carpet) and paid a commission to a broker to find a new tenant. Because the loan amount is fixed, the $30,000 cost increased your equity (aka cash investment): $60,000 original equity + $30,000 light rehab and commissions = $90,000 total equity.

After the light rehab, you were able to increase the NOI to $15,000.

Here’s a summary table to help you keep track of everything.

Real estate investment example cash flow

So what do these calculations tell us?

Cash Flow Increase

By spending a one-time cost of $30,000 for the light rehab and commissions, you went from $3,950 per year of cash flow to $8,950 per year. $30,000 to get $5,000 more per year? Well worth it.

NOI Increase = Value Increase

You have increased the NOI. NOI is a key metric buyers and lenders use to value a property. To oversimplify a bit, the value of the property has increased.

Why is this oversimplifying?

Because cap rates can go up and down depending on overall market sentiment, independent of your individual property.

For this discussion, let’s assume they stayed fixed.

Monetizing Value

Now let’s get into the fun part. How do you turn our hard work into cash? Said another way, how do you “monetize” the increase in value?

There are three main ways to do this:

Enjoy the cash flow.

Sell the property.

Cash out refinance.

Each way has its pros and cons. The decision of what to do depends on the goals you are trying to achieve, which may change over time.

Monetizing Value: Enjoy the Cash Flow

The first way is the most straightforward and passive: do nothing and enjoy the increased cash flow.

The $8,950 cash flow per year after light rehab on your $90,000 of equity is a 9.9% annual cash-on-cash return. Much of it is shielded from tax by depreciation. See 5 Tax Advantages That Make Real Estate Investing So Powerful.

If you are a cash flow investor like I am, this may be the best fit for you.

Monetizing Value: Sell the Property

Properties are typically sold based on a capitalization rate (cap rate). In this case you bought the property for a 6.1% cap rate: $10,000 NOI divided by $165,000 purchase price = 6.1%.

Let’s assume you can sell the property for the same 6.1% cap rate. $15,000 post light rehab NOI divided by 6.1% = $245,902.

This gives you a profit before commissions, closing costs, and income tax of $45,902. $245,902 - $200,000 total costs. Not a bad return in two years for your equity investment of $90,000.

If you are focused on increasing your total net worth as much as possible, this could be the path for you. You could consider a 1031 exchange to defer the taxes as I discussed in 5 Tax Advantages That Make Real Estate Investing So Powerful.

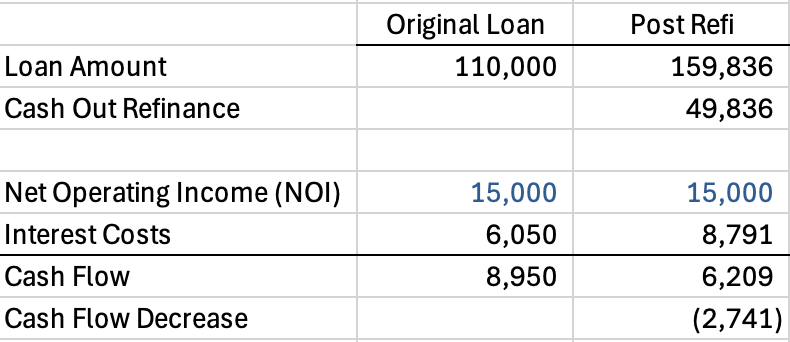

Monetizing Value: Cash Out Refinance

Refinancing the property could be a way to have the best of both worlds.

The increase in NOI will likely allow you to put a bigger loan on the property. Your original loan of $110,000 was approximately 65% of the purchase price.

Using the same 65% on the new market value we calculated above ($245,902) would give you a new loan of just under $160,000. $245,902 x 65% = $159,836. This new loan amount is almost $50,000 more than your original loan.

Doing this is known as a “cash out refinance”. There is no tax on the $50,000. You could use it to invest in a new property.

Important Caveat: Not all lenders will immediately give you a cash out refinance. Every situation is different so talk with multiple lenders.

Remember than your interest costs will go up and your cash flow will go down. If we assume the same 5.5% interest rate, your annual cash flow drops from $8,950 to $6,209.

Refinance example

You also have higher fixed expenses with the new interest costs. This gives you less cushion if you lose the tenant and/or the economy gets bad.

A cash out refinance is a good option for investors who want the best of both worlds (and are comfortable with higher fixed expenses): ongoing cash flow and additional money to invest in the next deal.

Monetization Options: Sale vs Cash Out Refinance

In this example, the cash out refinance proceeds ($49,836) are more than the sales proceeds before closing costs and commissions ($45,902).

This is not always the case.

Interest rates and cap rates regularly move around depending on market conditions and market sentiment. If you are on the fence of which option is best for you, educate yourself by talking with brokers on market cap rates and lenders (or debt brokers) on loan options.

Monetization Options: Pros and Cons

So let’s put it all together to see what the best fit for you is.

Enjoy the Cash Flow

Action: none; enjoy the additional cash flow.

Pros: passive; no further execution risk.

Cons: minimal current cash compared to a sale or cash out refinance.

Good for: investors focused on cash flow.

Sell The Property

Action: sell the property.

Pros: ability to unlock value and 1031 exchange into a new property to repeat the process of a new strategy on a new property.

Cons: execution risk on the sale; sale commission costs; tax exposure if no 1031 exchange.

Good for: investors focused on creating maximum wealth by buying and adding value to multiple properties over time.

Cash Out Refinance

Action: refinance the property with a larger loan.

Pros: ability to unlock value without paying taxes and continue to benefit from (a reduced) cash flow; the proceeds from the cash out refinance could be used to buy a new property.

Cons: execution risk on the refinance; transaction costs of refinance; risk of having more debt and interest expense.

Good for: investors wanting to balance ongoing cash flow and ability to grow their real estate portfolio by buying new properties.

What Worked for Me

As with my investing strategy, my monetization strategy has changed over time.

Stage I (Years 1-10+): Buy > Add Value > Sell > Repeat

I was all about maximizing the power of the limited funds I had. The goal was to create value, sell a property, and invest it in a new one. This was an effective method to build wealth. I still have a number of investments that fit this strategy.

Stage II (Years 10+): Enjoy the Cash Flow & Cash Out Refinances

Once I had built wealth, or at least could see a path to that future with my existing investments, I started to be more focused on cash flow. I was able to build up a combination of assets under two strategies:

Cash Flow: I have one property that I own debt free. The strategy is focused on consistent cash flow.

Cash Out Refinance: Buy > Add Value > Cash Out Refinance > Repeat. The LP investments I have follow this strategy. I use the cash out refinances to buy more cash flowing assets.

These stages have worked well together. I wouldn’t have been able to focus on cash flow investing without the capital I built up through selling properties.

Finding the Monetization Option That Fits You

Let’s think about what might work for you.

Situation A: Limited Capital, Long Time Horizon

This is likely your situation if you are early in your career. You are rich in time, energy, and health, but poor in money. You have a long time horizon for the power of compounding to go to work.

The buy, add value, sell, and repeat is a path that could allow you to turn your limited funds into something more meaningful.

Situation B: Some Capital, Shorter Time Horizon

Maybe you are exploring real estate investing for the first time later in life. Your time horizon to retirement, or at least leaving a W-2 job, is shorter. You have worked hard and saved a decent amount of capital to invest.

In this case a combination of enjoying the cash flow and cash out refinances may be a better fit for you.

What is Right for You?

I have seen investors follow each of these paths successfully. It all depends on your available capital, time horizon, and goals.

Do you have an investing story that you are willing to share with me? Email me at bateman@creprofessor.org. I read every email and would like to hear from you.

Professor Bateman

The Risk-Return Spectrum: Choosing Your Real Estate Investment Strategy

From low-risk turnkey deals to high-return value-add and development—which fits you?

Here’s a question you may be asking yourself: ‘Should I buy a turnkey rental or fixer-upper?’ The answer depends on understanding risk versus return - and knowing where you sit in this spectrum.

Low Risk/Low Return ←――――――――――――→ High Risk/High Return

Last week we discussed the importance of picking a niche in terms of “how” (REIT, LP, solo, GP) and “what”. I introduced the three components of the “what”:

Asset Class: 1-4 unit residential, apartments, office, industrial, retail.

Geography: where you plan to invest.

Strategy: core/turnkey, light rehab, value add (or fix and flip), house hacking.

In today’s discussion, we are going to dive deeper into strategy.

Strategy will likely be the strongest dial you can control to determine the risk and reward that is right for you.

Risk and reward are generally inversely correlated. The more risk you take on, the higher the potential reward.

The key word here is “potential”.

Just because you have the potential to hit a home run, doesn’t mean you will. It often means you have a high chance of not hitting the home run - especially in your early days as an investor.

Successful investors have a clear understanding of risk vs. reward. The best ones pick a risk/reward niche to focus on so they can develop expertise in understanding and minimizing risk, all while trying to achieve above market returns.

Let’s dig in.

Five Strategies for Real Estate Investing

There are five strategies we will discuss today. Four apply to all asset classes. The last one only applies to 1-4 unit residential.

Low Risk/Low Return ←――――――――――――→ High Risk/High Return

Core/Turnkey → Light Rehab → Value Add → Development

Core/Turnkey: low risk, low return. You buy a property that is well leased and maintained. There is minimal work to do.

Light Rehab: medium risk, medium return. There is some work to do, but it is mainly cosmetic (paint, carpet, clean up). If you do the work, you can increase the rent and value of the property.

Value Add: high risk, high return. There is a lot of work to do. The property might even be vacant. You will be repositioning it and taking on a lot of risk for superior returns. You will either find a tenant once the work is complete or sell it (fix and flip).

Development: highest risk, highest return. You build something from scratch.

House Hacking: this option only applies to 1-4 residential. You will live in one unit (or room) of the property and rent out the other units (or rooms), allowing you to live rent free or at a reduced cost.

Each strategy has its own pros and cons. There is no right answer.

Choosing the right one for you depends on the time you have and your tolerance for risk.

Let’s discuss each one in more detail.

Core/Turnkey: Low Risk, Low Return

These type of deals require minimal work. They are fully leased and the physical building is in good condition. They are closest to stock market index fund investing in effort (low) and function similar to a bond, giving you consistent cash flow. Examples could include:

A single tenant leased building built in the last 10 years and leased for 10+ years. This could be retail, industrial, or even office.

A new four-plex in a strong housing market near a hospital or other major employer. Although the leases are not long, there is a major employer nearby who helps ensure all units will remain leased with little downtime between leases.

Core/Turnkey deals are great for investors that want steady cash flow and don’t have a lot of time.

Light Rehab: Medium Risk, Medium Return

Let’s continue up the risk/return spectrum to Light Rehab. There is some rehab to do, but it is fairly straightforward and mainly cosmetic (paint, carpet, clean up). It is the type of work that you could potentially do yourself on nights and weekends, or hire a handyman to do.

Essentially, you are freshening up the property and once complete, will enjoy some combination of higher rent, shorter time between leases, better credit tenants, or a combination of all three. Examples could include:

A well built four-plex that is 30+ years old in a good market. The paint is peeling and the carpets are stained. Both are straightforward to fix. Buildings that look cleaner and more appealing are leasing for 10%+ more rent than the in place leases at this property.

A single tenant industrial building that only has six months left on the lease. The existing tenant has been there for 10+ years, plans to vacate, and is leaving the space very dirty. Painting the walls, replacing the carpet in the office, and power washing the warehouse floors will make it look much better.

Light Rehab deals are good for investors that want to be a little more hands on in order to achieve better returns than core/turnkey. They are ok with some risk, but are not willing to spend too much additional money nor take on something too complicated.

Value Add: High Risk, High Return

Let’s continue up the risk/return spectrum. By buying a value add deal, you are signing up for a hands on investment. There will be a lot of work to do, including work that is not just cosmetic in nature. You may be redoing bathrooms or replacing roofs or even building out new rooms.

This is much more than a light freshen up. It will likely include hiring a general contractor and obtaining a building permit. All of this means more time and money.

In exchange, you will enjoy a meaningful increase (ex. 25%+) in the value of the property through a combination of higher rent, shorter time between leases, better credit tenants, or a combination of all three. Examples could include:

A 40+ year old two story home in a zoning location that allows for up to four units. The investor will convert the property into a four plex. This will include adding three small kitchens and a new restroom, plus reconfiguring the property to create four individual private entrances.

A 20+ year old retail property that had been leased to one tenant since it was built. The investor will convert it to a three tenant building by adding demising walls, bathrooms, and storefront entrances.

Value Add deals are good for investors that have a vision for what a property could be. They have time and money to do the work and are determined to maximize the value of their investments.

Development: Highest Risk, Highest Return

Developers are a breed of their own. They are like business entrepreneurs who create something out of nothing. Development is so complicated that I could (and may) dedicate an entire newsletter to it.

For now, let’s just say that it includes (i) buying the land with a vision for what could be built, (ii) creating an initial design and getting municipal approval to build it - the entitlements, (iii) spending time and money on construction drawings, (iv) going back to the municipality for a building permit, (v) hiring a general contractor to build the property, and (vi) leasing it. Examples could include:

Buying vacant land and building a small industrial building.

Tearing down an old house and building a new four-plex.

Development is a high risk process at each step. It is not for the faint of heart or inexperienced. Each step requires specialized knowledge: architecture, engineering, municipal approvals, construction management, and market analysis. Most developers spend years learning their craft before attempting their first project.

House Hacking: 1-4 Unit Residential Only

House hacking is a way to satisfy your own housing needs and be a real estate investor. You buy a property to live in that is bigger than you need and rent out the rest, allowing you to live rent free or at a reduced cost. Here are two examples:

You buy a four-bedroom house with one kitchen and 3-4 bathrooms. You live in the master bedroom with a private bathroom and rent out the other rooms. You all share the living room, kitchen, and laundry room. Maybe you rent the rooms to friends as you will be sharing a lot of space together.

You buy a duplex. You live in one unit and rent out the other. Your tenant lives in their own unit. There is no shared space.

House hacking is a creative way to become a real estate investor. Lenders view 1-4 unit residential as personal home loans, which can be easier to qualify for if you are a first time investor.

However, you have to be comfortable living with or near your tenants. This can get messy, especially if living with friends. Example: your buddy loses his job and can’t pay the rent. Are you willing to kick him out? Just plan ahead for what you are willing and not willing to do.

Understanding Strategy

Now that we have discussed five strategies, let’s break down the characteristics that (a) determine the risk associated with an investment and (b) determine your fit for each strategy.

Risk Associated with an Investment

To oversimplify, there are four main risks associated with a real estate investment:

Occupancy: is the property leased? How soon do the leases expire?

Rent vs Market: are the existing tenants paying market rent? Is there an opportunity to increase the rent? What are the current and anticipated market conditions?

Property Condition: is the property old? Is there deferred maintenance? Are the units leasable as is or do they need to be cleaned up first?

Property Function: is the property functional as configured? Do the number of units needed to be increased or decreased?

Let’s combine these with the first three strategies (excluding development and house hacking):

Core/Turnkey: Low risk, Low return.

Occupied

Rent at or Near Market

Good Property Condition and Function

Light Rehab: Medium Risk, Medium Return.

Vacant or Occupied Short Term

Rent Below Market

Property Condition Can Be Improved

Property Functional As Is

Value Add: High Risk, High Return.

Vacant or Occupied Short Term

Rent Below Market

Property Condition and Property Function Can Be Improved

Your Fit for Each Strategy

Now let’s add in what is required for each relative to how it will impact you as an investor from a time and future dollar commitment standpoint.

Core/Turnkey: Low risk, Low return.

Most passive; minimal time commitment and ongoing capital investment.

Light Rehab: Medium Risk, Medium Return.

Active for focused periods of time; more passive after rehab; requires some investment of dollars and time after purchase.

Value Add: High Risk, High Return.

Very active for focused, extended periods of time; may be more passive after rehab; requires significant investment of dollars and time after purchase.

Development: Highest Risk, Highest Return.

Significantly time consuming for 2-3+ years; requires coordinating the efforts of many consultants and specialists; material capital commitment years before completion.

Very Important Side Note: Strategy is only one element of a real estate investment. The market you invest in will play a HUGE role in the success of the deal. Spend the time to research and understand the market before you make your first investment. Talk with brokers. Read research papers. Understand the major employers and drivers of the local economy.

My Strategy Evolution

Here’s how it evolved for me over the past 23 years of investing.

Stage I - Clueless to Strategy: I made an LP investment in a value add hotel deal. I had no idea there were different types of strategy or that I was taking on more risk than I realized. I was lucky it worked out.

Stage II - Value Add with Employer: I spent most of my career with a GP focused on value add industrial. By joining an established firm with leaders who understood value add investing, I was able to get paid to learn. When I made personal investments, it was mainly alongside seasoned investors who had “been there, done that”.

Stage III - Value Add as LP: In 2015, I started making LP investments with a multifamily GP focused on value add deals. I even spent two years working for the GP and learned the operational side of the multifamily business. Their leadership team had years of value add investing experience. They were able to minimize risk through their extensive track record.

Finding the Strategy That Fits You

So which is right for you?

If you are new to real estate investing, you don’t know what you don’t know.

Something that may look risk-free to you could be riskier than you think. Something that looks risky to you, could appear much less risky to a seasoned investor.

Unless you can work for an experienced GP and invest alongside them, I recommend starting simple with a core/turnkey or light rehab.

Get a few deals under your belt.

Make some mistakes and learn from them before you buy a value add deal.

Here’s a quick self-assessment guide. Ask yourself:

Time: Do I have time on evenings/weekends for 3-6 months?

If not, then consider a Core/Turnkey deal.

Capital: Can I set aside cash reserves for cost overruns and unexpected issues?

If not, then consider a Core/Turnkey or Light Rehab deal.

Experience: Have I completed 2+ deals through stabilization and/or sale?

If not, then consider starting with a Core/Turnkey or Light Rehab deal.

Tolerance: Can I sleep at night with a property that is filled with uncertainty?

If not, avoid Value Add and Development.

Be honest with yourself. Miscalculating risk and how you will handle it can turn your side hustle into a 20-40 hour per week commitment.

Investing takes time and patience.

You can always become a value add investor later down the road. Just recognize that you need to put in your reps with simpler deals first.

Learn the fundamentals of operating real estate: market analysis, the acquisition process, securing a loan, executing a business plan, property management, tenant relations, and property accounting.

Doing this on a simple, low-risk deal really has its benefit.

There are no shortcuts.

You have to put in the work.

Professor Bateman

Stop Chasing Every Deal: Why Successful Investors Pick a Niche

How to choose your asset class, geography, and strategy—and why focus beats FOMO

Here's an uncomfortable truth: most beginning real estate investors fail because they chase every shiny opportunity instead of focusing on one niche.

Yes, there will be times to veer from your niche temporarily or even pivot entirely, but keeping focus will yield the best results in the long run.

Successful investing in real estate requires building expertise. Expertise is MUCH easier to build if you focus on a specific niche.

Why is this true?

Why not just look at a whole variety of opportunities and pick the ones with the best risk adjusted returns for you?

The answer: developing expertise takes focused repetition. Focused repetition is only possible if you pick a niche.

Let me explain.

What is a Niche?

In reference to real estate investing, let’s define a “niche” as a combination of (a) how you are going to invest and (b) what you are going to invest in.

The “how” was discussed in detail in 5 Ways to Invest in Real Estate (From $60 to All-In). Here is a quick recap of the ways, from least time consuming to most time consuming:

Owning shares of a REIT.

Investing as a limited partner (LP).

Buying a property by yourself.

Buying a property with someone as equal partners.

Buying a property as the general partner and raising money from LPs.

The “what” is new to our discussion. It is made up of three components.

Asset Class: 1-4 unit residential, apartments, office, industrial, retail.

Geography: where you plan to invest.

Strategy: core/turnkey, light rehab, value add (or fix and flip), house hacking.

When you combine these combinations, there are literally 100’s of niches to choose from.

It may seem overwhelming.

Help!!!!

Don’t worry.

As with any big issue, the key is to break it down into parts.

For this discussion, let’s assume the “how” of your niche will be to buy the property by yourself. This will allow us to focus on the “what”. Even if you decide to invest with a partner (or raise money) or invest as an LP, the same principles will apply in thinking about the “what”.

Asset Class

Choosing an asset class is probably the most foundational decision you need to make. I discussed asset classes in detail in Asset Classes Explained: Industrial, Office, Retail, Multifamily, and 1-4 Unit Residential. Here’s a short recap:

Industrial: Simple to operate, low ongoing capital needs, good cash flow.

Office: Complicated to operate, high ongoing capital needs, challenging cash flow.

Retail: Reasonable to operate, moderate ongoing capital needs, good cash flow.

Multifamily/Apartments: Intensive to operate, varied ongoing capital needs, good cash flow.

1-4 Unit Residential: Easier than apartments to operate, varied ongoing capital needs, good but lumpy cash flow due to the limited number of tenants.

If you are just starting out and have more limited funds, the most accessible asset classes will be:

1-4 unit residential.

A small industrial property.

A small single-tenant retail property.

The reason to pick one asset class is because each type has its own nuances and characteristics. If you jump from type to type, you will never develop any expertise. Without expertise you will miss opportunities and misjudge risk.

Geography

Geography is just as it sounds: where are you going to invest? Think of it in terms of:

Region: example coastal markets or the sunbelt states or the midwest.

Markets: a specific area within a region. Example: Charlotte, NC.

Submarket: this gets even more specific. What micro areas do you like in your market?

You don’t have to start with a submarket specifically. For example, maybe you have $30,000 to invest. You are limited to lower cost markets and can’t afford coastal areas.

You might pick the midwest U.S. as your region and then focus on Detroit over time. As you learn more about Detroit, you could then pick the submarkets you like.

Remember, you don’t have to limit yourself to the market you live in. You can find a good broker and property manager in another market who will do all the work for you while you direct the overall strategy. See You Don’t Have to Do Everything Yourself: Building Your Real Estate Team.

It is OK to have multiple geographies to focus on. It just means more areas to keep up with. I recommend starting with one. Or doing some research on two to three with the goal of ultimately focusing on one.

Strategy

Strategy is the approach you are going to take to operating your property. We will explore this in detail next week. For now let’s start with the following options:

Core/Turnkey: low risk, low return. You buy a property that is well leased and maintained. There is minimal work to do.

Light Rehab: medium risk, medium return. There is some work to do, but it is mainly cosmetic (paint, carpet, clean up). If you do the work, you can increase the rent and value of the property.

Value Add: high risk, high return. There is a lot of work to do. The property might even be vacant. You will be repositioning it and taking on a lot of risk for superior returns. You will either find a tenant once the work is complete or sell it (fix and flip).

House Hacking: this option only applies to 1-4 residential. You will live in one unit (or room) of the property and rent out the other units (or rooms), allowing you to live rent free or at a reduced cost.

Each strategy has its own pros and cons. There is no right answer.

You can see that choosing the right one for you depends on the time you have and your tolerance for risk.

Now let's see how this works in practice. Here are four real-world niche examples that combine these elements differently.

Creating Your Niche: Putting It All Together

Option 1: Good for a W-2 employee with no spare time who wants passive income.

Asset Class: Retail

Geography: Pacific Northwest

Strategy: Turnkey

You decide to buy single tenant leased fast food buildings that are leased long-term (ex. 10+ years). The tenants are responsible for maintaining the buildings so there is very little work for you to do. You have always liked the Pacific Northwest because you grew up there and saw businesses like Amazon, Costco, and Microsoft drive the economy.

Option 2: Good for a W-2 employee with limited time who wants passive income.

Asset Class: 1-4 Unit Residential

Geography: Southeast U.S.

Strategy: Turnkey

You don’t have a ton of free time, so you want to buy turnkey assets that don’t need a lot of work. You live in a more expensive coastal market, but can’t afford to buy there so you find a good broker and property manager who will find and manage your future out-of-state properties that will be in a more affordable market in the southeast. You are starting with a one or two unit residential property because that is all you can afford. Over time, you hope to assemble a collection of duplexes and four-plexes.

Option 3: Good for someone with time to be more active in managing their investment.

Asset Class: Industrial

Geography: San Antonio, TX

Strategy: Light Rehab

You like the simplicity of industrial. You are targeting an older, well located building that needs to be repositioned with some paint and new signage. You like San Antonio because it is near the fast growing market of Austin.

Option 4: Good for someone ready to give their evenings and weekends to fixing up the property.

Asset Class: 4 Unit Residential

Geography: Los Angeles, CA

Strategy: Value Add

You have lived in LA all your life and have seen that there is never enough housing. You have researched the rent control laws of California and understand how to navigate them. You scrape together all the money you have to buy a 50+ year old four-plex in West Los Angeles that needs a major rehab. You plan to hold this property forever and pass it on to your children.

Why Having a Niche Matters

As you can see, these four options are very different strategies.

Finding a property to invest in takes work. You will likely have to look at 10-100+ potential properties before you find one to buy.

It is through this repetition that you start to (a) learn more about your niche and (b) see the one or two properties that are a better deal than the others.

Without this level of focus and repetition, you are like an athlete playing many different sports. You may be adequate at each, but you will never develop expertise.

The most successful investors focus and become experts in their niche. If they have multiple niches it is because they mastered the first and expanded into additional niches.

How to Choose Your Niche: A Simple Framework

Ask yourself three questions:

Money: How much capital do I have to invest? (This limits your asset class and geography options)

Time: How much ongoing time can I dedicate? (This determines your strategy)

Interest: What excites me? (You are more likely to stick with what you find interesting)

Closing Thoughts

There are at least two ways to look at the concept of having a niche.

Feeling Constrained

Feeling a Sense of Freedom

Some will feel constrained. They are the type who have FOMO, feeling there are always better opportunities that they are missing out on. They hear of someone making a successful investment outside of their niche. They decide to pivot. 18 months and five pivots later, they have either failed to make an investment or worse, made an impulsive investment decision that may or may not work out.

Distraction is the enemy of progress.

I encourage you to view it from the other perspective, as freedom. By focusing on a niche you will have freedom.

Freedom to develop expertise.

Freedom to focus.

Freedom to ignore temptations outside of your niche.

Once you build expertise and momentum in your niche, you can expand and add to it.

I didn’t start with expertise in multiple asset classes, markets, and strategies. I developed and grew expertise over my 20+ year career in real estate and being an investor.

But ask me about a market I don’t have any experience in (ex. Miami or New Jersey) and I will acknowledge I don’t know much.

This is fine. Humility is a good thing.

What you don’t want to do is be an investor who makes bets without doing the research or having focus. You won’t be an expert on your first deal, but you will build momentum over time if you stick to a niche.

My Niche Evolution

Here’s how it evolved for me over the past 23 years of investing.

Stage I - No Niche: I made an LP investment in a hotel in Los Angeles without any investment focus. I made this investment because the GP was (and still is) my friend. Luckily, it worked out.

Stage II - Western U.S., Value Add, Industrial: For the 20 years I was at Westcore, we primarily focused on this niche. Yes we did some retail and office deals, but we were primarily focused on industrial. After 20 years we actively expanded our geography to Texas and further east while maintaining a focus on value add industrial.

Stage III - Western U.S., Value Add, Multifamily as an LP: In 2015, I started making LP investments with a multifamily GP. I actively pursued this focus to build up passive income and diversify outside of industrial. I even spent two years working for the GP and learned the operational side of the multifamily business.

In stage I, I was clueless. I was lucky to invest with a GP who was very capable and honest.

My time at Westcore (stage II) allowed me to develop real expertise in a niche.

It was only after 10+ years at Westcore that I added an additional niche as a multifamily LP investor (stage III). The expansion came after mastering the previous niche - not before.

Today, my personal investment portfolio is still industrial and multifamily with strategies I understand and in markets I know well. These are my niches. What happens when I see an office deal? I am a quick no.

Focus doesn’t mean you never change. It means you build expertise before expanding your focus.

Do you have a story you want to share of sticking to a niche or veering outside of it? Email me at bateman@creprofessor.org. I read every email and would enjoy hearing your story.

Professor BatemanHere's an uncomfortable truth: most beginning real estate investors fail because they chase every shiny opportunity instead of focusing on one niche.

Yes, there will be times to veer from your niche temporarily or even pivot entirely, but keeping focus will yield the best results in the long run.

Successful investing in real estate requires building expertise. Expertise is MUCH easier to build if you focus on a specific niche.

Why is this true?

Why not just look at a whole variety of opportunities and pick the ones with the best risk adjusted returns for you?

The answer: developing expertise takes focused repetition. Focused repetition is only possible if you pick a niche.

Let me explain.

What is a Niche?

In reference to real estate investing, let’s define a “niche” as a combination of (a) how you are going to invest and (b) what you are going to invest in.

The “how” was discussed in detail in 5 Ways to Invest in Real Estate (From $60 to All-In). Here is a quick recap of the ways, from least time consuming to most time consuming:

Owning shares of a REIT.

Investing as a limited partner (LP).

Buying a property by yourself.

Buying a property with someone as equal partners.

Buying a property as the general partner and raising money from LPs.

The “what” is new to our discussion. It is made up of three components.

Asset Class: 1-4 unit residential, apartments, office, industrial, retail.

Geography: where you plan to invest.

Strategy: core/turnkey, light rehab, value add (or fix and flip), house hacking.

When you combine these combinations, there are literally 100’s of niches to choose from.

It may seem overwhelming.

Help!!!!

Don’t worry.

As with any big issue, the key is to break it down into parts.

For this discussion, let’s assume the “how” of your niche will be to buy the property by yourself. This will allow us to focus on the “what”. Even if you decide to invest with a partner (or raise money) or invest as an LP, the same principles will apply in thinking about the “what”.

Asset Class

Choosing an asset class is probably the most foundational decision you need to make. I discussed asset classes in detail in Asset Classes Explained: Industrial, Office, Retail, Multifamily, and 1-4 Unit Residential. Here’s a short recap:

Industrial: Simple to operate, low ongoing capital needs, good cash flow.

Office: Complicated to operate, high ongoing capital needs, challenging cash flow.

Retail: Reasonable to operate, moderate ongoing capital needs, good cash flow.

Multifamily/Apartments: Intensive to operate, varied ongoing capital needs, good cash flow.

1-4 Unit Residential: Easier than apartments to operate, varied ongoing capital needs, good but lumpy cash flow due to the limited number of tenants.

If you are just starting out and have more limited funds, the most accessible asset classes will be:

1-4 unit residential.

A small industrial property.

A small single-tenant retail property.

The reason to pick one asset class is because each type has its own nuances and characteristics. If you jump from type to type, you will never develop any expertise. Without expertise you will miss opportunities and misjudge risk.

Geography

Geography is just as it sounds: where are you going to invest? Think of it in terms of:

Region: example coastal markets or the sunbelt states or the midwest.

Markets: a specific area within a region. Example: Charlotte, NC.

Submarket: this gets even more specific. What micro areas do you like in your market?

You don’t have to start with a submarket specifically. For example, maybe you have $30,000 to invest. You are limited to lower cost markets and can’t afford coastal areas.

You might pick the midwest U.S. as your region and then focus on Detroit over time. As you learn more about Detroit, you could then pick the submarkets you like.

Remember, you don’t have to limit yourself to the market you live in. You can find a good broker and property manager in another market who will do all the work for you while you direct the overall strategy. See You Don’t Have to Do Everything Yourself: Building Your Real Estate Team.

It is OK to have multiple geographies to focus on. It just means more areas to keep up with. I recommend starting with one. Or doing some research on two to three with the goal of ultimately focusing on one.

Strategy

Strategy is the approach you are going to take to operating your property. We will explore this in detail next week. For now let’s start with the following options:

Core/Turnkey: low risk, low return. You buy a property that is well leased and maintained. There is minimal work to do.

Light Rehab: medium risk, medium return. There is some work to do, but it is mainly cosmetic (paint, carpet, clean up). If you do the work, you can increase the rent and value of the property.

Value Add: high risk, high return. There is a lot of work to do. The property might even be vacant. You will be repositioning it and taking on a lot of risk for superior returns. You will either find a tenant once the work is complete or sell it (fix and flip).

House Hacking: this option only applies to 1-4 residential. You will live in one unit (or room) of the property and rent out the other units (or rooms), allowing you to live rent free or at a reduced cost.

Each strategy has its own pros and cons. There is no right answer.

You can see that choosing the right one for you depends on the time you have and your tolerance for risk.

Now let's see how this works in practice. Here are four real-world niche examples that combine these elements differently.

Creating Your Niche: Putting It All Together

Option 1: Good for a W-2 employee with no spare time who wants passive income.

Asset Class: Retail

Geography: Pacific Northwest

Strategy: Turnkey

You decide to buy single tenant leased fast food buildings that are leased long-term (ex. 10+ years). The tenants are responsible for maintaining the buildings so there is very little work for you to do. You have always liked the Pacific Northwest because you grew up there and saw businesses like Amazon, Costco, and Microsoft drive the economy.

Option 2: Good for a W-2 employee with limited time who wants passive income.

Asset Class: 1-4 Unit Residential

Geography: Southeast U.S.

Strategy: Turnkey

You don’t have a ton of free time, so you want to buy turnkey assets that don’t need a lot of work. You live in a more expensive coastal market, but can’t afford to buy there so you find a good broker and property manager who will find and manage your future out-of-state properties that will be in a more affordable market in the southeast. You are starting with a one or two unit residential property because that is all you can afford. Over time, you hope to assemble a collection of duplexes and four-plexes.

Option 3: Good for someone with time to be more active in managing their investment.

Asset Class: Industrial

Geography: San Antonio, TX

Strategy: Light Rehab

You like the simplicity of industrial. You are targeting an older, well located building that needs to be repositioned with some paint and new signage. You like San Antonio because it is near the fast growing market of Austin.

Option 4: Good for someone ready to give their evenings and weekends to fixing up the property.

Asset Class: 4 Unit Residential

Geography: Los Angeles, CA

Strategy: Value Add

You have lived in LA all your life and have seen that there is never enough housing. You have researched the rent control laws of California and understand how to navigate them. You scrape together all the money you have to buy a 50+ year old four-plex in West Los Angeles that needs a major rehab. You plan to hold this property forever and pass it on to your children.

Why Having a Niche Matters

As you can see, these four options are very different strategies.

Finding a property to invest in takes work. You will likely have to look at 10-100+ potential properties before you find one to buy.

It is through this repetition that you start to (a) learn more about your niche and (b) see the one or two properties that are a better deal than the others.

Without this level of focus and repetition, you are like an athlete playing many different sports. You may be adequate at each, but you will never develop expertise.

The most successful investors focus and become experts in their niche. If they have multiple niches it is because they mastered the first and expanded into additional niches.

How to Choose Your Niche: A Simple Framework

Ask yourself three questions:

Money: How much capital do I have to invest? (This limits your asset class and geography options)

Time: How much ongoing time can I dedicate? (This determines your strategy)

Interest: What excites me? (You are more likely to stick with what you find interesting)

Closing Thoughts

There are at least two ways to look at the concept of having a niche.

Feeling Constrained

Feeling a Sense of Freedom

Some will feel constrained. They are the type who have FOMO, feeling there are always better opportunities that they are missing out on. They hear of someone making a successful investment outside of their niche. They decide to pivot. 18 months and five pivots later, they have either failed to make an investment or worse, made an impulsive investment decision that may or may not work out.

Distraction is the enemy of progress.

I encourage you to view it from the other perspective, as freedom. By focusing on a niche you will have freedom.

Freedom to develop expertise.

Freedom to focus.

Freedom to ignore temptations outside of your niche.

Once you build expertise and momentum in your niche, you can expand and add to it.

I didn’t start with expertise in multiple asset classes, markets, and strategies. I developed and grew expertise over my 20+ year career in real estate and being an investor.

But ask me about a market I don’t have any experience in (ex. Miami or New Jersey) and I will acknowledge I don’t know much.

This is fine. Humility is a good thing.

What you don’t want to do is be an investor who makes bets without doing the research or having focus. You won’t be an expert on your first deal, but you will build momentum over time if you stick to a niche.

My Niche Evolution

Here’s how it evolved for me over the past 23 years of investing.

Stage I - No Niche: I made an LP investment in a hotel in Los Angeles without any investment focus. I made this investment because the GP was (and still is) my friend. Luckily, it worked out.

Stage II - Western U.S., Value Add, Industrial: For the 20 years I was at Westcore, we primarily focused on this niche. Yes we did some retail and office deals, but we were primarily focused on industrial. After 20 years we actively expanded our geography to Texas and further east while maintaining a focus on value add industrial.

Stage III - Western U.S., Value Add, Multifamily as an LP: In 2015, I started making LP investments with a multifamily GP. I actively pursued this focus to build up passive income and diversify outside of industrial. I even spent two years working for the GP and learned the operational side of the multifamily business.

In stage I, I was clueless. I was lucky to invest with a GP who was very capable and honest.

My time at Westcore (stage II) allowed me to develop real expertise in a niche.

It was only after 10+ years at Westcore that I added an additional niche as a multifamily LP investor (stage III). The expansion came after mastering the previous niche - not before.

Today, my personal investment portfolio is still industrial and multifamily with strategies I understand and in markets I know well. These are my niches. What happens when I see an office deal? I am a quick no.

Focus doesn’t mean you never change. It means you build expertise before expanding your focus.

Do you have a story you want to share of sticking to a niche or veering outside of it? Email me at bateman@creprofessor.org. I read every email and would enjoy hearing your story.

Professor Bateman

You Don’t Have to Do Everything Yourself: Building Your Real Estate Team

How to assemble the right specialists so you can focus on what matters

In my previous post 5 Ways to Invest in Real Estate (From $60 to All-In), I discuss the passive and active ways to invest in real estate. A quick overview:

Passive: buying REIT shares or investing as a limited partner (LP) with someone that puts together and manages the investment - the general partner (GP).

Active: buying a property on your own, with a partner, or by raising money from multiple LPs.

Both are good ways to invest and, as with almost everything in life, they each have their trade offs.

Passive Investing

Passive investing requires minimal effort. Someone else does the work. Once you make the investment, you don’t have to do much. Read the quarterly reports. File your tax return. In exchange, you have little control and pay the REIT or GP to run the investment (we will get into the details of fees and promotes another week).

Active Investing

Active investing gives you more control and allows you to collect fees and promote. In exchange, you have to do all the work.

Unless you are part of a company that acts as the GP, this can be an overwhelming amount of work. Just like a business owner, you have to wear many hats and deal with a vast variety of issues.

The Many Demands of Owning a Real Estate Investment

Regardless of the type of investment property you buy, you will be faced with many, many issues as a real estate owner. Calls from tenants with plumbing leaks, tenants not paying rent, insurance policies, loan expirations, vendors and contractors, tax returns…the list is seemingly endless.

This can be daunting as you think of making this your side-hustle.

Don’t worry.

There are ways for you to handle this and keep your sanity.

The key is to assemble the right team.

And for those who want to go all-in and create a company, this will be an essential guide of who you need as your employees and advisors.

Let’s dig in.

An Industry of Specialists

The real estate industry is full of people that specialize in various niches within the industry. I break down the industry in my discussion on CRE 101.

The groups in green have a financial interest in a property. Said another way, they write a check to invest.

The groups in blue provide services to the groups in green for a fee. Sometimes the fee is one time. Sometimes it is on a monthly basis. Sometimes the owner creates a company and hires people in the blue group to be their employees. Example: property management and accounting.

Each group is made up of people that have chosen to specialize in their given niche based on their skills and interests.

Be the Leader. Don’t Do Everything Yourself.

As the owner of a property, it is up to you to decide what you want to do yourself and what you want to pay a specialist to do. Do you want to:

Get calls from tenants or pay a property manager to handle this?

Do the accounting/bookkeeping or hire an accountant?

Lease the vacant space or hire a broker?

Fix the leaky faucet or hire a handyman?

Oversee the construction or hire a general contractor?

Everyone is different. You need to decide what works for you.

For the property I own with a partner, I pay a property manager to interface with the tenants, manage the vendors, and do the property accounting.

But when it came to replacing the roof a few years ago, I decided to work directly with the roof company as it would only be done every 10 years and it is so critical to the performance of the building.

So who does what and how do they get paid?

Let’s break it down.

Here are the key roles you need to understand, roughly in the order you'll need them:

Mentor

Role: A mentor is someone who (a) has already achieved what you want to achieve and (b) is interested in helping you. They are your vision of yourself in 5-10 years. Your mentor was helped by others in their journey. They want to pay it forward. They will be your guide, especially in challenging situations.

Compensation: None. You shouldn’t need to pay a mentor. This will only work if you demonstrate you are someone worth the mentor spending time on.

How to Find One: Ask around. Contact someone on LinkedIn. Meet someone at an industry event. Be specific about what you want to learn and respect their time. Come prepared with questions and updates on your progress.

Business Partner

Role: They are your investing partner. You do the deal together. You keep each other accountable and share the ups and downs.

Compensation: None. You each invest in the property as partners.

How to Find One: Only do a deal with someone you know and trust. It is like a marriage. See Option 4 in 5 Ways to Invest in Real Estate (From $60 to All-In).

Acquisition Broker / Realtor / Real Estate Agent

Role: They find the property for you. The good ones help you navigate the acquisition process, from the purchase contract to due diligence to escrow and title to the loan and to closing. They have been there, done that. They are licensed by the state they reside in. Note that most of the time they are selling the property on behalf of the owner. Make sure you ask who they are representing. They will either be representing the seller or both of you. Either is fine. Just know that if they are only representing the seller, they may be giving you an (overly) optimistic vision of the market conditions. Make sure you ask the opinion of other brokers not part of this transaction.

Compensation: Commission. They earn 1-6% of the purchase price, depending on the size of the deal and asset class. Example: $3M x 6% = $180,000. The commission is paid at closing and typically paid by the seller. You pay nothing as the buyer unless this is pre-agreed upon by you and the broker.

How to Find One: Check loopnet.com and other websites to see properties for sale. They will list the broker. Contact the broker and tell them what you are looking for. There are national brokerage companies that specialize in industrial, retail, office, and larger apartment buildings (CBRE, JLL, Newmark, Marcus & Millichap, Cushman & Wakefield, Voit, and Lee & Associates). Brokers that specialize in 1-4 unit residential tend to be more locally focused. If the latter, you want to find one that specializes in investment properties, not traditional home sales.

Leasing Broker

Role: Same as an acquisition broker, except they specialize in leasing. This is typically only applicable to industrial, retail, and office. Property management companies tend to do the leasing for apartments and 1-4 unit residential.

Compensation: Commission.

How to Find One: Through the acquisition broker.

Property Manager and Property Accountant

Role: Manages the day-to-day of a property, from interfacing with tenants to managing vendors and maintenance needs to overseeing smaller construction jobs. This role is critical to running a property as well as being the most time consuming on an ongoing basis. They also provide accounting to track the monthly financial performance of a property.

Compensation: A percentage of monthly revenue with a minimum or it could be a flat fee. Example 3-5% of monthly revenue with a $1,000 per month minimum. There could also be additional charges for overseeing construction and renewing tenants.

How to Find One: Through the acquisition broker.

Lender / Loan Broker

Role: The lender provides the debt to help you buy the property. A loan broker helps you find the right lender for you by marketing the property to many different lenders.

Compensation: The lender may charge you not only a fee for the loan at closing (example 1% of the loan amount), but will also pass through the amounts they pay to their attorneys and due diligence consultants. The loan broker is paid just like an acquisition broker (example 1% of the loan amount).

How to Find One: Through the acquisition broker.

Insurance Broker / Agent

Role: Connects you with the right insurance carrier for you to get insurance to protect you against costs related to property damage (property insurance) and being sued (liability insurance).

Compensation: Commission that is imbedded into the cost you pay the insurance carrier.

How to Find One: Through the acquisition broker.

Handyman or Contractor

Role: Handles repairs and construction, ranging from fixing a leaking faucet to painting a vacant unit to replacing a roof.

Compensation: Fixed or percentage fee.

How to Find One: Through the property manager.

Escrow & Title

Role: An escrow agent is the “referee” between the buyer and the seller. They make sure each party follows what is required under the purchase and sale agreement as well as manage the exchange of money. Title makes sure that what everyone thinks is being bought and sold is actually being bought and sold. They also provide title insurance to protect against future issues.

Compensation: One time fees.

How to Find One: Through the acquisition broker.

Attorney

Role: Advises you on legal issues. On larger deals (ex. $5M+), attorneys are used to negotiate purchase and sale agreements, loan agreements, and partnerships agreements involving GPs and LPs. They are also used on larger leases. Some owners won’t do a deal without advice from an attorney. Others rely on standard form documents without using an attorney (Example: AIA Contracts).

Compensation: Paid based on an hourly rate.

How to Find One: Through the acquisition broker or property manager.

Tax Accountant

Role: Prepares your tax return and advises on tax strategy. Remember, the property manager only does monthly property accounting that tells you about the monthly performance of your property (income statement, balance sheet, and cash flow). This is different from a tax return you file with the IRS.

Compensation: Paid based on an hourly rate.

How to Find One: Through the acquisition broker or property manager.

Summary

That was a lot to cover. Let’s try to make it more digestible by providing two examples of how you could approach this.

Option 1: Keep it Simple - Outsource Everything

Find a broker that works for a company that also does property management, accounting, and construction management. Even brokers that work for companies without these services know of other companies that can provide them.

A good broker will help you find a property to invest in and bring together the team to both help you buy it and run it once you own the property.

Once you own it, be clear on what you want to approve and what you are delegating to the property management team. Example: the property manager has discretion to proceed with all maintenance issues < $250 without owner’s approval. Increase or decrease your delegation threshold over time. Dive into specific issues if needed. And be willing to change teams if the existing property manager is not working for you.

Option 2: Active Control

Do any or all of the above functions yourself. You will still likely want to use a broker, but everything else you can do yourself.

You will save money but you will pay for it with your time and energy. You will experience first hand what it is like to get an emergency call from a tenant in the middle of the night or while you are on vacation.

It is not for everyone, but it does have the advantage of teaching you what it is like to really run a property.

You Can Change Your Approach Over Time

Remember that none of this needs to be permanent. You could start with the active approach and then switch to the outsource approach.

This is what I did with my industrial property.

Active: I did the property management and accounting myself for a year and then decided this was not for me.

Hybrid: I then hired a group to do the property management only while I continued with the property accounting.

Outsource: Finally, I decided they did not manage the property in the way I wanted it managed, so I hired a new property manager and increased the scope so that they did the property accounting as well. They have been excellent. I happily pay them their monthly fee.

There is no universal right answer.

Be a student of yourself and observe what works for you.

Professor Bateman

Asset Classes Explained: Industrial, Office, Retail, Multifamily, and 1-4 Unit Residential

Which real estate type matches your investment goals, time, and capital?

It’s funny. The term “commercial” is my least favorite way to describe a particular individual property, yet it is the most accurate to describe the industry as a whole.

In my experience, “commercial” real estate is any property that is operated as an investment; where the business plan is to make money.

The home you live in is not commercial real estate.

The house you rent out for income is commercial real estate.

There are many types of commercial real estate known as “asset classes”.

Understanding how they differ is critical to becoming a successful real estate investor. In my last newsletter (5 Ways to Invest in Real Estate), I discussed the “how”. Now we are describing the “what” you can invest in.

I’ve invested in six of these over the past 20+ years and talked with investors who have focused on the others.

By the end of this newsletter, you’ll know which asset class aligns best with your goals, risk tolerance, and available time.

Let’s dig in.

The Major Asset Classes

Industrial

Office

Retail

Multifamily aka Apartments

1-4 Unit Residential: single-family home rentals, duplexes, triplexes, fourplexes.

Other: Medical Office, Shopping Malls, Biotech, Data Centers, Hotels, Self-Storage, Industrial Outdoor Storage (IOS)

Each of these has different characteristics in terms of:

Physical Characteristics: What they look like physically and how they function.

Tenants: Which tenants they attract and what those tenants are looking for.

Operational Complexity: The demands on owner to operate them.

Capital Needs: The ongoing capital they require to operate.

Lease Structure: Whether the tenant pays anything in addition to rent.

Investment Profile: Cash flow and investment characteristics.

Summary: key takeaways.

We are going to cover a lot of information here. See below for a list of the main asset classes with a “cheat sheet” of their characteristics added.

Industrial: Simple to operate, low capital needs, good cash flow.

Office: Complicated to operate, high capital needs, challenging cash flow.

Retail: Reasonable to operate, modest capital needs, good cash flow.

Multifamily: Intensive to operate, varied capital needs, good cash flow.

1-4 Unit Residential: Easier than apartments to operate, varied capital needs, good but lumpy cash flow due to the limited number of tenants.

The goal is to find the right fit for you as an investor.

Quick Note: I had to err on the side of oversimplifying to summarize all of this information. Those of you who have spent years focused on one asset class may find I missed tons of the nuances of that asset.

I would probably agree with you.

Think of this as the starter to see where you want to dig in.

Industrial

Photo by Point3D Commercial Imaging Ltd. on Unsplash

Physical Characteristics

Industrial buildings are generally single story warehouse buildings that have 5-50% of the interior of each individual suite built out as office. Buildings and suite sizes can range from 5,000 square feet (SF) to 500,000+ SF. Sometimes one tenant occupies the entire building. Sometimes it is broken up into smaller suites. The ceiling heights can range from 12’ to 40’. They normally have large warehouse doors for backing large trucks into to load and unload products.

Tenants

Tenants that lease industrial buildings are typically storing products, manufacturing, conducting e-commerce, or running a small business that requires storage of parts (ex. plumbing, HVAC).

Operational Complexity

Industrial buildings are relatively easy to operate, particularly the larger buildings. The larger the tenant (by SF), the more self-sufficient they tend to be. Most leases require the tenants to handle everything inside their suite (ex. light bulbs and HVAC).

Capital Needs

Industrial buildings don’t require much capital to operate. The tenant improvements (costs to fix up the suite for the next tenant) tend to be relatively low due to the low percentage of office. The most expensive thing to replace on an industrial building is a roof.

Lease Structure

Most industrial leases are 3-10 years in length and triple-net (NNN). NNN means that in addition to the tenant paying base rent, it also pays its share (defined by % of total SF) of the expenses to operate the building such as maintenance contracts, insurance, and property tax. We will get into NNN more in another newsletter.

Investment Profile

The combination of the duration of the leases, the NNN lease structure, and the low capital needs make industrial a good asset for cash flow and an attractive one for investors.

Summary

Simple to operate, low capital needs, good cash flow. I am a big fan of industrial.

Office

Photo by Rahul Bhogal on Unsplash

Physical Characteristics

Office buildings are generally multi-story buildings with the interior built out for knowledge workers. You have probably been in one. They tend to be broken up into smaller suites ranging from 1,500 SF to 5,000 SF, although some suites can be much bigger.

Tenants

Tenants that lease office buildings are made up of knowledge workers who sit at desks on computers, meet in conference rooms, and congregate around a water cooler to chat. Think of the show “Suits”, the drama that takes place in the office of a law firm.

Operational Complexity

Office is demanding to operate. Not only do tenants expect the owner to change lightbulbs and fix the HVAC in their suite, but there are also major building systems to be maintained, repaired and replaced: elevators, glass exteriors, centralized HVAC systems, and other systems.

Capital Needs

Office buildings are capital pigs: they constantly need money. To lease up an office building for the first time, the owner needs to invest $100+ per square foot (psf) in tenant improvements (TIs) to do 5-10 year leases. At the end of these leases, the next tenant likely wants a different build out, requiring $25-50 psf in new TIs.

Then there are the building systems, which last for about 20 years if well maintained. Replacing an elevator or HVAC system can cost millions in an office high-rise.

Can you tell I am not really a fan of office? I was the asset manager on a suburban office portfolio for years and was constantly amazed by how much we had to spend to get a tenant in our buildings (even on renewals). Proceed with caution.

Lease Structure

This varies from market to market. Some are NNN like industrial buildings. Some are what’s known as a “base year” structure where the tenant only pays their share of increases in operating expenses. Again, don’t worry about this for now.

Investment Profile

I like to think of office as a trading asset. Once the tenants are in place and the rent roll is stable, it can be sold as a good value. But the high ongoing capital needs make it a challenging asset for cash flow.

Summary

Complicated to operate, high capital needs, challenging cash flow. I am unlikely to ever invest in office again.

Retail

Physical Characteristics

Ever been to a grocery store, restaurant, or a coffee shop? Then you have experienced retail. It could be a grocery anchored shopping center like the one in the picture above, or it could be an indoor mall. Suite sizes range from 1,000 SF to 50,000+ SF. It is where you go to buy goods and services.

Tenants

Tenants that lease retail buildings sell goods and services. Examples include: grocery and drug stores, fitness centers, restaurants, clothing stores and general retailers.

Operational Complexity

Retail can be demanding to operate, but for different reasons than office. It is similar to industrial in that most leases require the tenants to handle everything inside their suite (ex. light bulbs and HVAC).

The more challenging part comes with many of the tenants being smaller with limited credit. Owners are constantly managing through tenants struggling to pay rent. There is also an art to creating the right tenant mix that is synergistic and helps increase each tenant’s sales. The right anchor can make or break the whole retail center.

Capital Needs

If we think of a grocery anchored shopping center, capital needs are fairly reasonable. More than industrial, but less than office. Tenants generally need a rectangular box to outfit with their furniture, fixture, and equipment (FF&E). Capital requirements would be much more for a mall that has elevators, escalators, and even HVAC.

Lease Structure

Most are NNN, similar to industrial.

Investment Profile

Retail can be a good cash flowing asset. The performance is highly contingent on the anchor tenant(s). They are the main draw to bring in shoppers. If the anchor vacates, the smaller tenants will struggle.

Summary

Reasonable to operate, modest capital needs, good cash flow.

Multifamily aka Apartments

Physical Characteristics

As you read this newsletter, you may be sitting in your apartment. They are where so many of us live. These are typically built out with a kitchen, bathroom, living room, and one or more bedrooms. They have shared walls and often include common area amenities such as pools, gyms, and dog parks. They are in suburban locations like the picture above, or can be built as high-rises in urban areas.

Tenants

You and me.

Operational Complexity

Multifamily is probably the most complicated asset to operate. Tenants live in them 24/7, not just during business hours. Leases are 6-12 months long, so tenants are constantly moving in and out. Kitchen fires and other events happen all the time.

Be kind to your apartment property manager. It is a very tough job.

Capital Needs

They can be minimal or extensive, depending on how the owner chooses to operate. The floor plans and interior build outs don’t change from tenant to tenant as they do in office. Owners may choose to paint and carpet or refresh a kitchen or bath, but they rarely reconfigure a floor plan.

However, the volume and coming and going of tenants beats up the common areas, which can require constant maintenance.

Lease Structure

To oversimplify, multifamily leases are “gross” in structure. Tenants pay the rent and none of the operating expenses. But as those of you who have lived in apartments know, there are often additional charges such as internet, trash, and utilities.

Investment Profile

The multi-tenant nature of multifamily can be magic for steady cash flow. Most owners of 100+ unit multifamily have a target occupancy (ex. 95%) and adjust the rent each day to hit that target.

Summary

Intensive to operate, varied capital needs, good cash flow. I am a big fan of apartments as an LP investor. I think it is an excellent option for cash flow.

1-4 Unit Residential: Single-family Home Rentals, Duplexes, Triplexes, Fourplexes

Photo by Ferdinand Asakome on Unsplash

Physical Characteristics

Duplexes, Triplexes, and Fourplexes are 2, 3, and 4 unit buildings similar to apartments without the common areas amenities. Single-family home rentals are houses that are rented out to a tenant by the homeowner.

Tenants

You and me.

Operational Complexity

Same as apartments, without the common area amenities.

Capital Needs

Same as apartments, without the common area amenities.

Lease Structure

Same as apartments.

Investment Profile

Same as apartments, without the ability to set a target occupancy because of the limited number of tenants.

Summary

Easier than apartments to operate, varied capital needs, good but lumpy cash flow due to the limited number of tenants.

This could be your on-ramp to real estate investing. Here’s why I break it out as its own asset class.

It is much more accessible to individual investors with limited funds. One can buy a single-family home to rent for less than $100,000 in some markets.

If a building is four units or less, lenders view it as a personal loan. They will evaluate your personal credit as opposed to calculating the cash flow on the property. This can be helpful if you are just starting out.

If you want to start investing in properties on your own in an active way (as opposed to as an LP), this will likely be the most realistic path for you.

Other: Medical Office, Shopping Malls, Biotech, Data Centers, Hotels, Self-Storage, Industrial Outdoor Storage (IOS)

As the newsletter is already fairly long, I will give a brief description of these “specialty” assets.

Medical Office: similar to office, but for medical professionals (ex. dentist). TIs are even higher.

Shopping Malls: complicated to operate, high capital needs, challenging cash flow.

Biotech: similar to office, but for the biotech industry. TIs are veryhigh due to the lab build outs.

Data Centers: think of a warehouse full of computer servers. High power and cooling needs. Very expensive.

Hotels: imagine an apartment where the tenants only stay for 1-3 nights at a time and the owner provides cleaning and room service. This is a hotel. It is more like running an operating business than a real estate investment. I have two LP investments in hotels, but I recognize that operating one as a GP would require a tremendous amount of time and focus.

Self-Storage: very small, open industrial suites for storage leased 1-12 months at a time.

Industrial Outdoor Storage (IOS): land leased to tenants to store products.

Summary

Wow! That was a lot to cover.

Is your head spinning?

Don’t worry. There will be no tests.

All you need to do is pick the one or two that you want to explore:

Industrial: Simple to operate, low capital needs, good cash flow.

Office: Complicated to operate, high capital needs, challenging cash flow.

Retail: Reasonable to operate, modest capital needs, good cash flow.

Multifamily: Intensive to operate, varied capital needs, good cash flow.

1-4 Unit Residential: Easier than apartments to operate, varied capital needs, good but lumpy cash flow due to the limited number of tenants.

Intimidated by the operational intensity of any of these? No problem.

Invest in a REIT or as an LP.

If you are just getting started, I recommend you pick a niche that works for you. It would be a combination of:

Asset class.

Geography.

Investment method (REIT, LP, self, partnership, or GP as discussed last week).

Successful real investing requires focus.

Distraction is the enemy of progress.

Use the guide to narrow your focus.

Pick one asset class. Learn everything you can about it. Make your first investment and you will learn so much more.

Your needs will evolve over time. I started with a hotel, then focused on industrial, office and retail, and eventually made my way to multifamily.

Now most of my investments are in industrial and multifamily.

Success requires focus. Diversification can come later.

Email me at bateman@creprofessor.org to tell me which asset class resonates with you and why. I read every response.

Good luck!

Professor Bateman

Cap Rates: The Simple Math of Real Estate Investing

Cap Rate - this is probably the first and most fundamental concept to understand as a real estate investor. You may have heard someone say something like, “I bought the property for an 8% cap rate and sold it for a 5% cap rate” and found yourself nodding but on the inside you had no clue what this meant.

Don’t worry! Like most of real estate, it sounds complicated but it’s actually straightforward once you understand the jargon. (Side note, this is true for many things in life.)

Cap rates are the simple math that drive so much of real estate analysis. And fortunately you don’t need to be a “math” person to understand it. You learned all you need in Algebra I. It can literally be done on the back of a napkin.

Now that I have hopefully eased the concerns of all the math haters, let’s dig in.

Cap Rate is a commercial real estate term. It is short for “capitalization rate”. It is often used interchangeably with “Return on Costs”. Both refer to the investor’s annual return (example 5% per year) on their investment. It changes, and hopefully grows, over time.

Cap rates are also the key method through which real estate investments are valued.

Cap Rate = Net Operating Income Divided by Cost