Closing Day: What to Expect

Documents, money flow, and key takeaways for your first closing

Over the last four weeks we have covered four topics on acquiring (aka buying) an investment property.

Now we are going to get into what happens during the actual closing, when ownership transfers from the seller to the buyer.

This will be the 5th and final newsletter on the acquisition process. Next week we will transition to how to own and manage your property.

Last week’s discussion on debt was long. This one is going to be shorter as it is a fairly straightforward process with far fewer moving parts.

Essentially, the closing process involves two things:

The exchange of money.

The signing of documents to legally transfer ownership.

Let’s dig in.

What is Closing?

When I talk about “closing”, I am referring to the day in which money and ownership transfer between the seller and the buyer.

Due diligence has been completed.

The buyer has gone non-refundable with their deposit and the closing date is here.

What happens next?

Here’s a typical closing timeline:

3-7 days before: finish up loan documents.

1-3 days before: sign documents.

0-3 days before: buyer and lender wire money into escrow. Bind insurance.

1 day before: final review of closing statement.

Closing day: last minute document signing and any other issues.

0-2 days after: notify tenants and vendors; record deed with the county.

The actual “closing day” can be anticlimactic as it may feel like you are just waiting for the escrow officer to say “we are closed”.

The Role of Escrow

As discussed in Demystifying Real Estate Purchase Agreements, the escrow officer at the escrow company plays the “referee” and lead coordinator of the sale process.

They make sure all the documents get signed and sent to them.

They arrange the legal recording (aka evidence) of the sale.

They also hold and distribute the money.

In short, they make it all happen.

Documents Get Signed

As also discussed in Demystifying Real Estate Purchase Agreements, there are a number of “form” documents that were agreed to in the purchase and sale agreement (“PSA”) and added as exhibits.

These “form” documents are then used as templates to create the actual documents that formalize the sale.

They include:

Grant Deed: this is the legally recorded document that confirms the property has been sold. Recording the document with the local municipality allows everyone to see that the property has been sold.

Bill of Sale: this documents the sale of any personal property related to the physical property. Examples: parts and materials for repairing the property such as flooring or light bulbs.

General Assignment: this documents the transfer of the various contracts such as leases, warranties, and service contracts.

There may also be other documents signed such as the one that notifies the county property tax assessor of the sale.

If the buyer is getting a loan to buy the property there will also be:

Deed of Trust: the legally recorded document that shows there is a loan on the property.

Loan Agreement and related documents: each lender has their own set of documents that they like to use.

In addition to documents getting signed, money will need to change hands.

Money Exchange

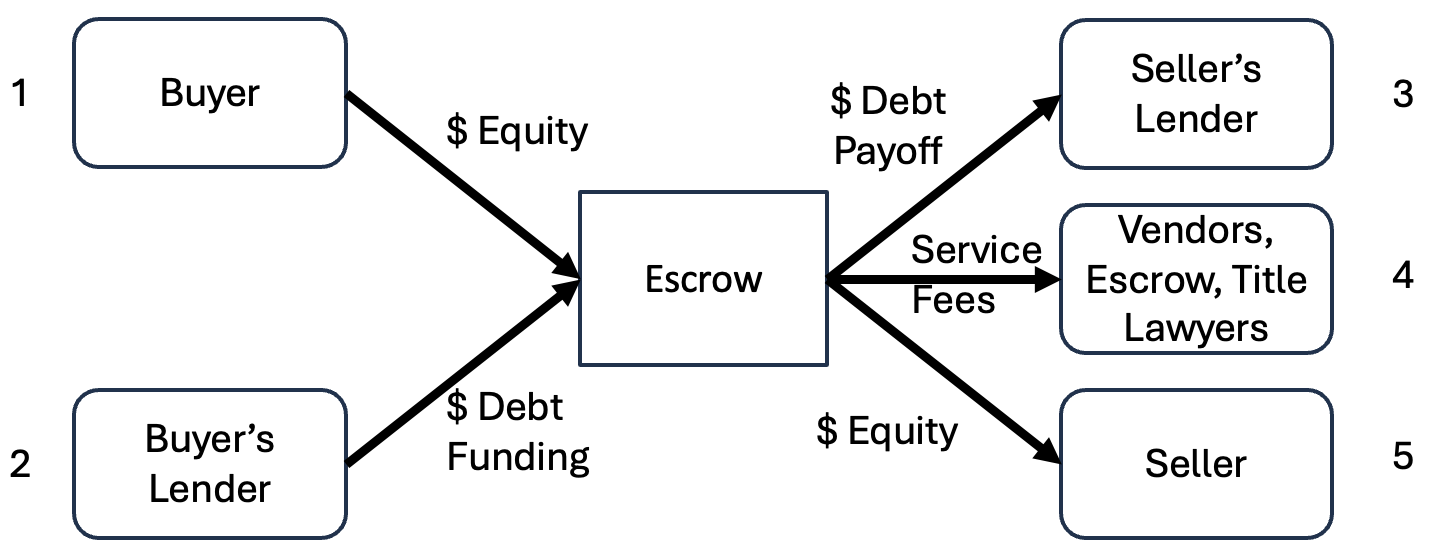

If both the buyer and the seller each have a loan on the property, then there will be five parties giving and/or receiving money.

These are the parties and this is the typical order in which money flows. Everything goes through escrow.

$ Into Escrow: Buyer sends in their equity.

$ Into Escrow: Buyer’s lender sends in their loan funds. They want to see the buyer’s money in first.

$ Out of Escrow: Seller’s lender receives money to pay off the seller’s existing loan on the property.

$ Out of Escrow: Payments to inspection vendors, escrow, title, and lawyers.

$ Out of Escrow: Seller receives the balance of the sale proceeds.

Here’s a diagram to help you understand.

Diagram: Flow of Money at Closing

Escrow officers make it all happen.

Closing day is stressful for all parties. Escrow officers live this every day! Be kind and patient with them.

Let’s move on to another critical component relative to money moving around: closing statements.

Closing Statements

Closing statements show who is getting paid what. There will be at least two closing statements:

Buyer’s Closing Statement

Seller’s Closing Statement

Think of them as an excel sheet showing “charges” and “credits” and ending in a total of how much the buyer and seller will owe and receive, respectively.

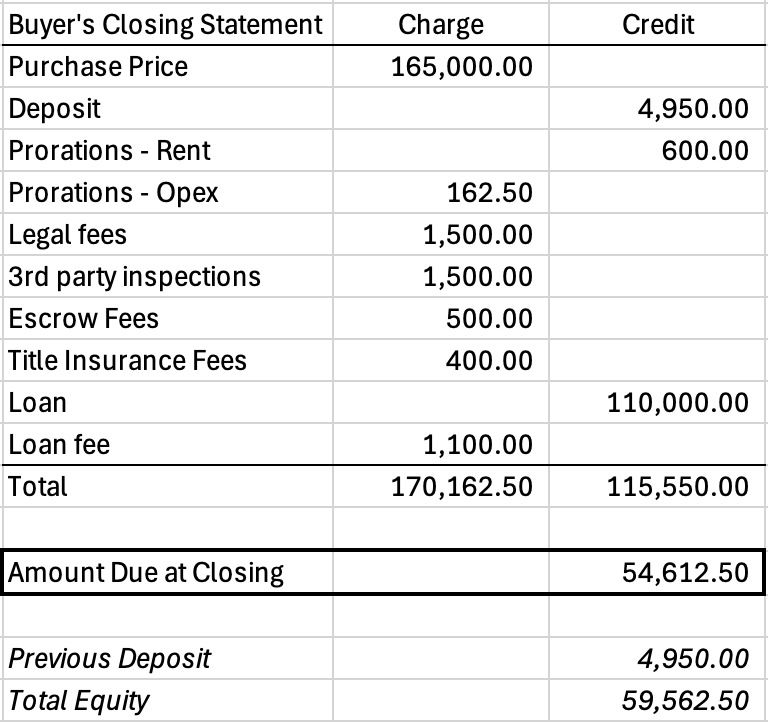

Ex. Buyer’s Closing Statement

Charges (amounts buyer has to pay)

Purchase price

Legal fees

3rd party fees for inspections

Escrow and title fees

Loan fees

Prorations*

Credits (amounts that reduce the buyer’s cash needs to close)

Deposits already made during due diligence

The loan

Prorations*

Total: at the bottom it will show how much cash the buyer will need to send into escrow to be able to close the deal.

*See discussion below for the meaning of “prorations”.

Here’s what the math would look like based on our ongoing example discussed in previous newsletters.

Diagram: Example Buyer’s Closing Statement

The amounts in italics would not be part of the closing statement. I added it to show the total equity the buyer actually funds which is:

$54,612.50 - amount due at closing to escrow

$ 4,950.00 - previously paid deposit

$59,562.50 - total equity paid to escrow

So why doesn’t it equal exactly $60,000 from our previous newsletter discussions?

Because of “prorations”.

Prorations

Prorations are the split of rent and operating expense between the buyer and the seller based on (a) the days of that month the buyer and seller will each own the property and (b) the timing of the rent or expense.

Simple example used in the closing statement above: you close on June 16th, halfway through the 30 day month.

Rent Proration

Tenant paid $1,200 rent to the seller on June 1st.

But the buyer (you) owns the property June 16th to 30th (16 days).

Seller owes you the rent for your 16 days: $1,200 x 16/30 = $600.

This $600 is credited to you on the closing statement.

Operating Expenses

Buyer paid $625 in operating expenses on June 1st.

But the buyer (you) owns the property June 16th to 30th (16 days).

You owe the seller for your 16 days: $625 x 16/30 = $162.50.

This $162.50 is charged to you on the closing statement.

Here are some things to note on these calculations:

Buyer’s ownership of the property starts on the day of closing, in this example the 16th of a 30 day month.

Prorations are based on amounts actually collected (rent) and paid (operating expenses) by the seller. If the tenant hasn’t paid the rent yet that month, the rent is not prorated. This often happens when the closing occurs in the first five days of the month. Same concept for operating expenses.

Insurance is not included in the proration as the buyer will need to get their own insurance. This is often paid through closing. Ask your insurance broker as the amount paid through closing will often be 6-12 months of premiums.

Not all operating expenses are paid monthly. This is especially true for property taxes. The proration will be adjusted for the timing of the payments.

Don’t worry if this is confusing. The escrow officer will do all the math.

What Happens Immediately After Closing

Once closing is complete, a number of things will happen right away.

Receive keys or access codes

Change locks (important for security)

Transfer utilities to your name

Contact tenants to introduce yourself and send them notices with contact information and rent payment instructions

Set up property management/accounting and maintenance vendors

This is because YOU are now the property owner!

Congratulations!

So what do you takeaway from all of this?

Key Takeaways

The closing process is when multiple parties come together to formalize the closing. Here’s what you should remember.

The escrow officer makes it all happen. They are the referee and the coordinator.

You will need to sign many documents: make sure your government-issued photo ID is current. Documents include:

One set to buy the property.

One set if you are getting a loan on the property.

Be 100% available the day before and of closing. There are often last minute documents that need to be signed. Sometimes they cannot be signed electronically, so it is ideal to have a local escrow company.

Many closings now happen remotely using electronic signatures and wire transfers. You may never meet your escrow officer in person. This is normal and perfectly safe - just verify wiring instructions carefully.

Scammers impersonate escrow officers and send fake wiring instructions. ALWAYS call your escrow officer at a verified number to confirm wiring details before sending money. Never rely on emailed wiring instructions alone.

The amount of cash you send to escrow will likely be different than the amount you have in your internal analysis. The difference will be prorations. Most of the time this is a minor issue, but property tax prorations can be big. So can the initial insurance payment. Talk to your escrow officer well in advance to understand this. You can also do the math yourself.

As discussed last week in the newsletter on debt, lender reserves can significantly reduce the amount of initial funding from the lender. A $110,000 loan with $10,000 of reserve holdbacks will only result in $100,000 of funds at closing. Read the loan documents. Understand this in advance. It is no fun to be jammed on the day of closing by not having enough cash to close because of reserve holdbacks by the lender that you should have known about.

Closing can get delayed for multiple reasons: title issues, lender funding delays, missing signatures, wire transfer problems, and other last minute issues. As long as all parties are reasonable and want to make the deal happen, you will be able to overcome these issues.

Stay calm and carry on. It will be stressful, but you will get through it. Don’t get frustrated and send a nasty email you will regret.

You’ve got this.

Follow the lead of your escrow officer (and lawyer if you are using one).

You will complete the closing and own your first property.

Owning the property is where the fun and work really begin.

That is the series we will begin next week.

Debt: An Amazing Tool with Strings Attached

How loans work, what lenders charge, and how to use leverage wisely

Debt. Loan. LTV. Lender.

These are all terms relating to borrowing money to own a property.

If you own a home as your primary residence, chances are that you have a loan on the property.

Why?

Because debt allows you to buy something that costs more than you can afford at that moment in time. It relies on at least two things:

People want more stuff. A bigger house. A bigger investment. Better returns.

There are groups willing to lend people money to get that stuff in exchange for a promise of future payments.

Here are two examples:

First Time Home Buyer

You want to buy a $170,000 home, but you don’t have $170,000. You have built up $60,000 in cash, but you need another $110,000 to buy the home.

Enter the lender.

The lender, often a bank, will loan you the $110,000 in exchange for an agreed upon set of future payments over 5-30 years, inclusive of a certain interest rate and fees. The interest rate and fees are how the lender makes money.

They will do this based on your personal income profile (salary, bonus) and personalcredit score. This is how they determine how risky you are as a borrower.

Investor Buying an Industrial Building

There is a similar structure when you are buying a commercial building with two main differences: (1) how the lender determines risk and (2) how long a loan they will give you.

With a commercial building, the lender looks at the property (in this example the industrial building). They value (aka appraise) the property and look at the income the property generates to make the monthly debt payments. Additionally, they will only give you a 2-15 year loan.

Stay tuned. I will explain this in more detail.

We will cover the basics of debt including:

How a lender makes money.

The niches lender have - just like investors do.

The types of lenders that focus on real estate investment properties.

How a lender determines how much to lend and what interest rate to charge.

The typical timeline to close a loan.

The benefits and risks of borrowing money to own real estate.

Professor Bateman’s key takeaways.

Let’s dig in.

How a Lender Makes Money

Lenders make money in three ways: (i) fees, (ii) interest, and (iii) by getting paid back at the end of the loan term.

#1 Fees: Fees are one-time charges lenders make to the borrower. Examples include:

Origination Fee: To give you the loan.

When: At the time the loan is funded to the borrower.

Amount: A percentage of the loan amount. Ex. 1% of $110K = $1.1K.

Extension or Payoff Fee: A time of extension or payoff.

When: At the time the loan is extended or paid back.

Amount: A percentage of the loan amount. Ex. 1% of $110K = $1.1K.

“Processing Fee”: this is a catch all for the many fees lenders may charge such as underwriting fee, processing fee, application fee, credit fee, appraisal fee, legal fee.

When: At the time (or before) the loan is funded to the borrower.

Amount: These are normally specific dollar amounts. Sometimes they are to reimburse the lender for fees they are paying a 3rd party such as an appraiser or lawyer. Make sure to ask what fees the lender will be charging.

Broker Fee: this is when a broker helped find you the lender and the loan. The fee goes to the broker, not the lender.

When: At the time the loan is funded to the borrower.

Amount: Typically a percentage of the loan amount. Ex. 1% of $110K = $1.1K.

#2 Interest: Interest is the ongoing amount that the lender charges the borrower for the loan. Ex. 7% per year.

7% x $110K = $7,700 per year. Divide by 12 to get the monthly amount of $641.67.

There are two important factors to consider with interest rates, as there are different structures with different types of loans.

Fixed vs. Floating Interest Rate

Fixed: The interest rate remains the same for the entire loan.

Floating: The interest rate changes during the loan, normally based on a fixed amount (ex. 3.50% - known as the “spread”) over a publicly available benchmark such as SOFR or Prime. Ex. If SOFR is at 4.00% and the spread is 3.50%, then the interest the borrower pays is 7.50%. If SOFR increases to 5.00%, then the borrower’s interest rate goes to 8.50% (5.00% SOFR + 3.50% spread).

Why this Matters: You get interest cost stability with a fixed rate loan. With a floating rate loan, you are adding an element of risk (both upside and downside) to your investment based on what interest rates do.

Interest Only vs. Amortizing

Interest Only: Each month the borrower only pays the interest costs.

Amortizing: In addition to the interest costs, the borrower also pays down the principal balance (i.e. a portion of the $110K loan) each month. This makes the borrower’s monthly payment more than an interest only loan payment.

Why this Matters: If you are tight on cash each month, an interest only loan can help a lot, but you will have to pay the full loan amount back at the end of the loan. In an amortizing loan structure, you will “chip away” at the principal balance each month.

#3 Getting Paid Back at the End of the Loan: this one is fairly obvious. If the borrower doesn’t pay the lender back at the end of the loan, then the lender is not going to make money.

To summarize the three ways lenders make money:

Fees

Interest Rate

Getting Paid Back at the End of the Loan

Keep in mind that a lender is not an equity investor. They are not going to benefit from the property being a home run.

In exchange for a lower return, they have lower risk. If the property goes bad and the borrower can’t make interest payments, the lender can take over ownership of the property. This is called foreclosing and the investors lose all their money.

Low risk, low return, better protection. It is a fair trade-off.

Lenders Have Niches Just Like Investors Do

Just as investors pick a niche, lenders pick one or more niches to focus on. Let’s oversimplify a bit and say there are four niche criteria for lenders:

Asset Class: 1-4 unit residential, multifamily, industrial, retail, office.

Geography

Strategy: core/turnkey, light rehab, value add, development.

Recourse vs. Non-Recourse

We should be familiar with the first three as discussed in Stop Chasing Every Deal: Why Successful Investors Pick a Niche.

The fourth one is unique to lending: recourse vs. non-recourse.

A recourse loan means that you are personally responsible to pay back the loan. If you get a home loan, it is almost certain that it is a recourse loan.

A non-recourse loan means that you are not personally responsible to pay back the loan (unless you commit fraud or there is an environmental issue). If there is an issue with the non-recourse loan in the industrial building example, the lender can’t come after your personal assets (cash, home, stock, other real estate, etc.)

In an ideal world, as a borrower you would only get a non-recourse loan.

Why? Here’s an example of a recourse loan gone bad.

You buy a $500K property with $400K loan. The market crashes and the property is now worth $300K. You can't make payments. The lender forecloses AND can come after your personal savings, home, other assets for the $100K shortfall ($400K loan amount less $300K current value).

With a non-recourse loan the lender can only look to the $300K property value, not your personal assets.

So why do some borrowers get recourse loan? For several reasons:

Scarcity: It may be the only type of loan available. There is not a non-recourse option. This is almost always true if you are doing a new development.

Economics: The loan has better economics than the non-recourse option (fees, interest rate, loan amount/proceeds).

1-4 Unit Residential: Lenders view 1-4 unit residential investment properties as personal properties by relying on a borrower’s personal income and credit score. This can be helpful if you are a first time buyer.

Let’s do a quick sidebar to point out three characteristics of loans for value add and development deals, as they are the highest risk and lenders treat them differently.

Loan Term (aka Length): Loans for these type of investments tend to be shorter - say 3-5 years. They are often called “bridge” loans. The idea is that they are more temporary in nature as the property is in transition.

Floating Interest Rate: For the same reasons as the loan term, these are more likely to have a floating interest rate.

Reserve Holdbacks: These are funds the lender “holds back” from the initial loan funding to pay for future costs such as construction, leasing, and even interest rate reserves. This reduces the amount of the loan at closing and allows the lender to make sure you spend their money on what you said you were going to spend it on.

So who are these mysterious “lenders”?

Types Of Lenders

There are four main types of lenders:

Banks & Insurance Companies

Debt Funds

Securitized

Fannie Mae and Freddie Mac (Government Sponsored Enterprises)

Banks & Insurance Companies: These groups lend their own money. Both have excess cash they want to earn a return on: banks from deposits and insurance companies from insurance premiums.

Debt Funds: Debt funds raise money from various investors such as pension funds, insurance companies, and university endowments. Debt funds tend to do riskier loans than banks in exchange for higher interest rates and fees.

Securitized: Securitized lenders function differently in that they plan to sell the loan to one or more investors after the loan closes. They effectively act as a middleman earning a fee. Sometimes they are mainly concerned with how the loan will be viewed by the ultimate buyer of the loan. Watch or read The Big Short to see this go to the extreme.

Fannie Mae and Freddie Mac: Fannie and Freddie are government sponsored enterprises created by congress to support the U.S. housing market (residential properties only). Similar to a securitized loan, a lender originates the loan and then the lender sells the loan to Fannie or Freddie. This allows the original lender to have more money to make new loans. Don’t worry about the details. Just know that they exist.

Key Takeaway: If you are a first time investors, you will likely work with a bank.

With that covered, let’s get to the next big question of how lenders evaluate a loan.

How a Lender Determines How Much to Lend and What Interest Rate to Charge

So how do they do it? With a magic lender calculator?

Quite simply: by assessing risk and pricing accordingly.

More risk, more costs to the borrower.

Assuming the property fits in the lender’s niche, the lender will generally (a) charge more fees and a higher interest rate and (b) provide a lower loan amount for properties the lender views as riskier.

Here’s an overview of the financial tools a lender uses to assess risk:

Appraisal: An appraisal is an assessment of the fair market value of a property as determined by some combination of (i) replacement / construction cost, (ii) similar properties that have sold recently aka “sales comps”, and (iii) the capitalized value. It is completed by a licensed third party appraiser.

The lender will normally have some max amount of appraised value they will lend up to. Ex. 65%. This is referred to as the “loan-to-value” or “LTV”. Here are some LTV rough guidelines. More risk to lender = lower LTV = more equity/cash you need.

Primary residence: 80-97% (3-20% equity)

Investment property (1-4 unit): 75-85% (15-25% equity)

Commercial (turnkey): 65-75% (25-35% equity)

Commercial (value-add): 55-70% (30-45% equity)

Development: 50-65% (35-50% equity)

DSCR: This stands for debt service coverage ratio. Think of this as the lender’s “cushion” in the property’s ability to generate enough income to pay interest. Mathematically it is NOI divided by Interest Costs. Ex. A property generates $10,000 NOI. Loan is $110,000 at 5.5% interest = $6,050 annual interest. DSCR = $10,000 / $6,050 = 1.65x.

The lender normally wants this to be at least 1.20. Remember, they are in the low risk, low return business.

Debt Yield: Think of this a the lender’s cap rate. Mathematically it is NOI divided by Loan Amount. Ex. $10,000 / $110,000 = 9.1%.

The lender will have a minimum target.

Personal Credit & Income: If a recourse loan.

Each lender has their own special formula or hot buttons they use based on some combination of these criteria.

Side note: did anything stand out to you relative to the LTVs above? Even on the riskiest deals, they are all 50% or higher. This means the lender is funding 50%+ of the cost of each real estate investment. The real estate industry would be very different without their support. Thank you to all the lenders out there!

So how long does it take to get a loan? That is our next topic.

Typical Timeline

Finding the right lender (1-4 weeks).

Negotiating a term sheet (1-2 weeks).

Negotiating the loan agreement (1-4 weeks).

Closing the loan (1 week).

Total 4-11 weeks (plan for 6-8 weeks typical).

This can be tight if you don’t start the process until you are already under contract to buy a property, especially if it is your first deal.

Remember that your due diligence period may only be 30 days. You don’t want to be in position where you put your deposit at risk by going non-refundable without certainty on your loan.

Start early. Establish relationships with potential lenders that fit your niche before you have your first property. This will make the whole process much easier.

Now that we have a basic foundation, let’s zoom out a bit to talk about debt on real estate in general.

The Benefits and Risks of Borrowing Money to Own Real Estate

So should you get a loan to buy real estate?

The reality for most new investors is that they will end up getting one to be able to afford their first property. And most seasoned investors will see too much benefit to their returns and scale to not want to borrow.

There are two main benefits to real estate loans:

Benefit #1 - Lower Equity Requirement

You don't need to have or raise as much equity when you have a loan for 50% to 75% of the amount needed to buy a property. An investor may simply not be able to come up with the cash needed to buy a property without a loan or they may want to buy more with the money they have.

Benefit #2 - The Power of Leverage

Leverage is the mathematical and financial benefit of borrowing money at a cheaper rate than the rate of return for the equity investors. If you borrow money at 5.50% and can earn 9.0%, then you have positive leverage.

9.0% earnings is greater than 5.50% cost of borrowing.

Positive leverage is a good thing because you are earning more than the cost of your interest rate.

If you borrow money at 5.50% and can earn 4.50%, then you have negative leverage.

4.50% earnings is less than 5.50% cost of borrowing.

Negative leverage is a bad thing because you are being charged more than you can earn.

If you are a professional real estate GP raising money from LPs you will find it hard not to use debt to be competitive in the marketplace to raise LP capital.

When you believe your investment can earn a 9% total return (IRR) over the full 5-10 year investment, it is too tempting not to turn that into a 12%+ total return by adding positive leverage.

So what are the negatives of borrowing money?

Negative #1 - Increased Risk

Borrowing money increases your risk by (i) increasing your monthly costs in the form of interest payments and (ii) requiring you to pay back the full loan amount on a specific date. Things don’t always go as planned.

Did you know the Empire State Building was under construction at the start of the Great Depression of the early 1930’s? The developer was able to finish the development and keep ownership of the property partly because he built it all cash without debt. If he had a loan, he would have almost certainly lost it to the lender at some point.

Negative #2 - Reduced Control

Not only will the lender charge fees and a monthly interest rate, but they may also have certain approval rights for things like larger leases, major capital improvements, and other operating choices. You limit what you can do when you have a loan on the property.

So what do you make of everything I have discussed here?

Professor Bateman’s Key Takeaways Regarding Debt

Understand that debt and leverage can be a wonderful tool to boost returns, but come with added risk and costs.

Accept that you will likely need a loan on your first deal.

Start early and identify lenders in advance. Not all lenders are created equal. Take the time to find the lender that fits your property profile. Using a debt broker can help.

Form relationships with good lenders to do repeat business.

Become familiar with the lender’s perspective on DSCR, debt yield, and appraisals. This will help you speak their language.

Look beyond just fees, interest costs, and proceeds. These are the financial cost of debt, but there may be operational implications and restrictions. Think about what is most important to you on a particular deal.

Be careful with floating interest rates and short-term loans. These can lead to challenges.

Watch out for pre-payment restrictions or penalties if you pay the loan off early. These limit your flexibility.

Understand reserve holdbacks may reduce your initial loan amount. Ex. A $110K loan with $15K of reserve holdbacks results in $95K of initial loan proceeds. This could mean more equity is required up front to close the loan.

Become familiar with loan documents. Learn more on my downloads page.

Acknowledge the benefit of working with lenders that hold the loans “on their books”. Be eyes wide open on whether the lender will sell / securitize the loan after they make it. Challenges will happen during the loan term. It is a lot better to be able to work problems through with original lender than one that bought it from that lender.

Avoid recourse loans when you can. You may need to take on recourse for your first duplex, but set a goal to avoid it as soon as you are financially able. One bad recourse loan could personally bankrupt you.

In my opinion, owning a property debt free without any LP investors is a fantastic place to be. It gives you the ultimate freedom.

You may not be able to start there, but I encourage each of you to think of it as a goal worth considering over the long term.

Professor Bateman

Due Diligence: Your Property Investigation Checklist

What to review before your deposit goes non-refundable - from leases to roofs

Due diligence.

Another piece of jargon from the real estate industry.

What does it mean?

In plain English:

Due diligence is the process of doing the investigative work to determine if what you think you are buying is what you are actually buying.

It is a way to minimize risk and avoid costly surprises.

If you are buying a 1-4 unit residential property, it is known as your inspection period.

If you are buying a commercial property, it is known as due diligence or “DD”.

You do this in the period of time before your deposit goes non-refundable, as detailed in last week’s discussion: Demystifying Real Estate Purchase Agreements

If you have bought a used car, you have experienced due diligence. You take the car for a test drive. Hopefully you followed up with an inspection or at least outsourced the inspection process by buying a “certified pre-owned” car from a dealer who completed the inspection. Maybe you even read the Carfax report.

All of this was done to determine if the car would drive OK once you owned it.

Same concept with buying real estate.

You want to make sure that you do what you can to confirm your investment property will perform as you expect it to perform.

How do you do this?

I like to use a simple cash flow statement to determine what to look for. Think of the cash flow statement as your guidebook.

By tying (almost) everything back to the cash flow statement, you minimize the risk of surprises.

Today we’ll cover:

How to use a cash flow statement as your due diligence guide

What to review for revenue (rent, vacancy)

What to check for operating expenses (utilities, insurance, property taxes, management fees)

How to evaluate capital improvements (capex, renovations, tenant improvements)

Non-cash flow items (zoning, title, environmental)

Simple vs. complicated properties

Let’s dig in.

Reminder: Refundable vs Non-Refundable

Last week we talked about the difference between the refundable (aka contingency) and non-refundable period. Let’s anchor on this concept again.

Refundable: From the date the Purchase & Sale Agreement (“PSA”) is signed through the expiration of the due diligence period, the buyer can typically back out of the deal for any or no reason and get their deposit back. No penalty. No foul. They still have to pay the consultants and advisors they may have hired and their reputation may suffer, but they don’t have to buy the property nor forfeit their deposit.

Non-Refundable: Once the due diligence period expires, everything changes. The buyer can still back out of the deal, but doing so will mean they lose their deposit.

Due diligence is one of the most important things the buyer does during the refundable stage of the acquisition process.

Cash Flow Statement as a Guide

Let’s continue our property example from one of my previous newsletters: Unlocking Value: What to Do After You’ve Improved Your Property. You are buying a property with $10,000 of net operating income (“NOI”). You believe you can perform a $30,000 light rehab to increase the NOI to $15,000.

In the table below, I have expanded our example to include some assumptions on the revenue and expenses to build up to the NOI.

Revenue less operating expenses = Net Operating Income.

Table: Light Rehab Property - Annual NOI Comparison

Let’s define each line item.

Revenue

Rent: what is paid by the tenants under the leases.

Vacancy / Credit Loss: an assumption that the property will not be leased the full year and/or the tenant will not pay rent and you will need to evict them at some point.

Operating Expenses

These are your recurring costs to operate the property, regardless of whether you have a loan on the property or not.

Utilities: any utilities the tenant doesn’t pay. Remember that you will have to pay utilities in the time between one tenant moving out and the next one moving in.

Repair & Maintenance (“R&M”): you may need to pay for some costs even if the tenant is leasing your property. Example: plumbing repairs.

Insurance: property and liability insurance.

Property Taxes: these are determined by the state and county in which the property is located.

Property Management Fee (“PM Fee”): if you are using a 3rd party to manage the property, you will need to negotiate what fee you pay them. Some GPs choose to act as the property manager and charge a PM fee.

Let’s run through how we can use this as a guide for our due diligence.

Revenue: Rent

There are two ways to look at rent: in place and market.

In place rent is determined by any leases for current tenants. The due diligence process involves reading the leases to confirm the rent and rent increases, any additional rent charges (ex. monthly utility reimbursements), the lease expiration, and any renewal options.

You will also want to note any landlord obligations (ex. replacing an HVAC unit by a certain date), any tenant obligations, and any other items that could affect the performance of the property.

Ideally you will want to interview the existing tenants to ask them how they like the property and if there are any problems with it and/or the landlord.

Market rent is totally different.

You will need to talk with brokers to get their opinion of market rent. In the example above, you are doing the light rehab so you want to talk with multiple brokers to get their opinion on what they think the property will lease for after you complete the light rehab.

Revenue: Vacancy / Credit Loss

Understanding the market and the likelihood (and duration) of vacancy will come from your conversations with the brokers. Simply ask: “How long do you expect the property to be vacant after I complete the light rehab?” By asking multiple brokers the same question, you will develop your own opinion.

Credit loss will be a combination of (a) reviewing the rent payment history of the existing tenants and (b) making an assumption. To review the existing tenants, the seller should provide you an “accounts receivable” report showing any rent that hasn’t been paid by the existing tenants. This is often referred to as the “A/R report”.

Ideally you also get a copy of the “tenant ledger” for the last 3-12 months which shows the payment history and timing of all tenant charges and payments, regardless of whether they currently owe delinquent rent or not. This is key to seeing when the tenants pay each month.

Your loan payment will likely be due in the first 5-10 days of the month. If your tenants don’t pay until the 20th, you will need to build up more cash to be able to pay the loan payment before you get the rent.

Operating Expenses: Utilities, R&M

These are determined by multiple methods:

Review of the seller’s historical income statements: ideally past two years. You want to see what has been paid in the past to determine the future.

Review of any service contracts in place. Examples: pest control, landscaping. The contracts will list the monthly payments amounts.

Review of historical utility statements. This will allow you to see the seasonality of the charges so you can do a monthly cash flow. It will also show you if there were any unusually high or low months. You will want to investigate these. Example: there may have been a water leak that caused the water bills to be high one month.

Operating Expenses: Insurance

You will need to get your own insurance for the property. You can’t use the seller’s insurance. Get quotes for property and liability insurance from an insurance broker. Property insurance if for physical damage to the buildings. Liability insurance is to protect you if get sued.

Operating Expenses: Property Taxes

Property taxes are determined by each state and administered at the county level.

Each state has a different method of calculating property taxes as well as a different frequency at which the amount of the property taxes are both paid and recalculated (aka re-assessed).

Review the seller’s property tax bills. Talk with the county assessor’s office and/or a property tax consultant to determine the specifics of that state and county.

Don’t assume your property taxes will be the same as the seller’s. Every state has different rules.

Operating Expenses: Property Management Fee (“PM Fee”)

The amount of the PM fee will be based on a new contract you negotiate with whomever you hire to manage the property and do the property accounting. It could be the same party as the seller used. It could be a new group.

Fees range from 1% - 8% of revenue depending on the size and complexity of the property.

NOI = Revenue minus Operating Expenses

That’s it.

You have done the due diligence to validate NOI. Well done!

But we are not finished yet.

Now let’s move on to the “below the NOI” items by discussing capital improvements.

Capital Improvements

Capital improvements are physical improvements to the buildings. They fall into three main categories:

Capex: repairing or replacing existing building systems such as the roof or HVAC in a “like for like” way.

Renovations: upgrading the existing building with light rehab or value add improvements.

Tenant Improvements & Leasing Commissions: costs to customize a space for a specific tenant and pay a broker commission for finding the tenant.

Capex

Due diligence is done on capex by:

Hiring consultants to review the existing building systems.

Getting bids from contractors for specific work.

Some consultants specialize in property condition assessment (aka property inspection or PCA) reports. They will give you an overview of the condition of the property with rough cost estimates by year.

But they won’t actually do the work to repair the property.

You need to get specific bids for the work from someone who will actually do the work.

This is key.

If the PCA says the roof needs to be replaced in the first three years, talk with a roof vendor to confirm this assumption and tell you how much it will actually cost if you engage that roof vendor to do the work.

This is where you get real pricing.

Renovations

You have a plan for what you want to do in your light rehab. Hopefully you validated and/or evolved it by talking with local brokers.

Now you need to price it out.

Just as you did with the roof vendor, meet with a contractor who will price out the light rehab and tell you a realistic time frame to complete the work.

Tenant Improvements & Leasing Commissions

This also comes from conversations with local brokers.

1-4 Unit Residential & Multifamily: there will be no or minimal tenant improvement.

Commercial (office, retail, and industrial): tenant improvements are very common. So are leasing commissions. Talk with local leasing brokers to develop realistic estimates. These are often significant ongoing costs for office and retail properties.

Non-Cash Flow Due Diligence

Although everything has the risk of ultimately impacting the property cash flow, there are some items that fall outside our “cash flow statement as a guide” concept.

These generally have the commonality of making sure you can operate the property as expected without interruption from the local municipality.

Zoning: check with the city to confirm the legal zoning for the property and that the property you are buying conforms with that zoning.

Title: most properties have some legal rights placed upon them by 3rd parties. Example: the local utility may have an easement to bring their electric lines to your property. The title report and the ALTA survey will tell you these.

Environmental: if you are buying an industrial or retail property, getting an environmental report is critical. You want to see if there are any issues (ex. old dry cleaner or manufacturer that contaminated the soil). There are consultants that specialize in this and create a “Phase I” report to summarize the environmental condition of a property.

Bringing it All Together

If this feels to you like a lot to review, then you are correct. It is a lot.

A typical due diligence timeline might be:

Week 1: review materials, order reports (PCA, title, environmental)

Week 2: property inspections, broker interviews

Week 3: review reports, contractor bids

Week 4: update your financial analysis and make final decisions

Things move fast. You owe it to yourself to be thorough so you need to be focused, prepared, and methodical. Don’t cut corners.

Here are some common issues that might come up in your due diligence:

Major capex discovered (immediate roof replacement)

Tenants not paying rent (A/R report shows major delinquencies)

Zoning violations (the property cannot be operated as is)

Environmental contamination (discovered in the Phase I report)

Title problems (liens, easements that restrict use)

Sometimes these can be negotiated with a price reduction or time to fix an issue. Sometimes they kill a deal.

If you find a problem, be transparent and solution oriented with the seller. You want to find solution that works for all parties.

Do I Really Have the Time for This?

If you are intimidated by the time involved, note that not all properties require the same level of time in your due diligence review.

Let’s give two examples.

Simple: 2-Unit Residential in Established Neighborhood

Revenue: there are just two leases to review. It is in a neighborhood with a lot of similar properties, some of which have been rehab’d and some of which have not. There are lots of similar properties to reference and talk with brokers about.

Capital Improvements: all you really need to do is confirm the condition of the property and price out your light rehab.

Non-Cash Flow Due Diligence: this will be straightforward as there shouldn’t be any issues.

Complicated: 50 Year Old Industrial Building with 50+ Tenants

Revenue: lots of leases to review. If the units are different sizes and configuration, determining market rent for each will also be complicated.

Capital Improvements: the building systems are old. There may be a variety of tenant improvements that are unique for each suite.

Non-Cash Flow Due Diligence: this could be complicated. Zoning may have changed over time. There is also risk of environmental issues.

In the simple example, you should have plenty of time to complete the due diligence before the period expires.

In the complicated example, you will be working non-stop to get it done.

Walk Before You Run

If you are new to real estate investing, start simple.

The complicated example may look attractive from a theoretical cash flow perspective, but the due diligence will be hard and full of risk for a new investor.

And remember, there are other things you will need to do before your due diligence period expires.

If you are getting a loan to buy the property, this will consume a lot of your time. You need time to figure this out and get the right loan.

Set yourself up for success by starting with a simple property.

Get in your reps.

Become an expert in due diligence.

What you learn in the due diligence process will form the foundation of your understanding of the property and pay dividends in the future.

Take the time to do it right.

For those of you that want to dig deeper, there are more resources on my downloads page.

Professor Bateman

Demystifying Real Estate Purchase Agreements

What's in a Letter of Intent and Purchase & Sale Agreement - and why you shouldn't be intimidated by them

Last week we discussed the process of finding your first real estate investment.

Building market knowledge.

Establishing broker relationships.

Finding and analyzing the right property for you.

The process is simple, but by no means easy. It requires focus and persistence.

Stick with the process. You will find a deal that works for you.

But what do you do once you have found a deal you want to buy?

Do you tell the broker or seller you are interested in buying the property?

Yes!

Do you have to send them something in writing?

Yes! A letter of intent.

Will you have to sign a legally binding document?

Yes! A purchase and sale agreement.

(It’s OK. We sign legally binding documents all the time. It you lease an apartment or a car, you have signed one.)

Will you have time to back out of the deal if you discover a problem?

Yes…up to a certain deadline. The due diligence period.

Never fear! I will walk you through the documents and the steps.

Let’s dig in.

The Letter of Intent: A Non-Binding Agreement

As with many real estate (and non-real estate) transactions, the process of buying a property from a seller usually includes two documents:

Letter of intent: a non-binding agreement.

Purchase & Sale Agreement: a binding agreement.

There are also a series of closing documents signed by each party just before closing, but these tend to be standard forms that are not as actively negotiated. Let’s not worry about the closing documents in this discussion.

So what is a letter of intent?

Think of the letter of intent (LOI) as a “handshake” agreement in 1-5+ pages. It will address the following:

Property Description

Names of Buyer and Seller

Purchase Price

Key Dates: due diligence start and end (aka the contingency period); closing date; extension options (if any)

Deposit - typically around 3% of the purchase price (ex. 3% x $500,000 = $15,000)

Name(s) of Broker(s) Involved

Escrow and Title Company

Confidentiality Requirement by Buyer and Seller

That the LOI is Non-Binding: make sure you check that it is!

Contingencies (if any): examples - loan assumption, tenant signing a lease, physical repairs

That’s about it.

It can be done in as little as one page.

Bigger firms may have more extensive LOI forms that include the list of due diligence items they require or other specifics, but the list above is the core of an LOI.

Most of the time lawyers are not involved as the buyer and seller, with the assistance of their brokers, prepare the LOIs.

The LOI goes back and forth between the buyer and the seller as the way to track the offer and counteroffers. This could happen one or many times.

Once the LOI is agreed to, the parties sign the LOI and move to the purchase and sale agreement.

Purchase and Sale Agreement: The Official Binding Agreement

The purchase and sale agreement (“PSA”) is both (a) much more extensive document than the LOI and (b) legally binding.

When you sign a LOI, you are putting your reputation on the line.

When you sign a PSA, you are putting your reputation AND your money on the line.

Even though most PSA’s give you a 15-30+ day due diligence period before your deposit goes non-refundable (i.e. you can’t get it back), you need to be very serious about buying the property if you sign a PSA.

You don’t want to build up a reputation as someone who signs a PSA but “can’t perform” - never actually buys (i.e closes on) a property. Brokers and sellers won’t take you seriously. The real estate community in most markets is surprisingly small.

So what’s in a PSA?

A PSA has all the components of an LOI plus (i) a more detailed description of the LOI terms, (ii) many additional terms and descriptions, and (iii) the PSA is binding.

Important Note: Refundable vs Non-Refundable

As we discuss the PSA agreement and the purchase process, let’s anchor in on the difference between the refundable (aka contingency) and non-refundable period.

Refundable: From the date the PSA is signed (the “effective date”) through the expiration of the due diligence period, the buyer can typically back out of the deal for any or no reason and get their deposit back. No penalty. No foul. They still have to pay the consultants and advisors they may have hired and their reputation may suffer, but they don’t have to buy the property nor forfeit their deposit.

Non-Refundable: Once the due diligence period expires, everything changes. The buyer can still back out of the deal, but doing so will mean they lose their deposit. Additionally, at this stage they are normally 15-30+ days into the process and emotionally invested in the deal. In my 20+ years of investing in real estate, I have seen less than a handful of cases where someone backs out of the deal after the due diligence period expires.

With that important foundation, let’s run through the additional terms and descriptions contained in a PSA that builds off the LOI.

Operating Conditions During the Purchase Process (aka Escrow)

The seller will continue to operate the property during escrow. Leases and contracts may be signed. Invoices will need to be paid. This section addresses how the buyer and seller will work together during escrow.

Contracts & Leases: the buyer will often have rights to approve contracts and leases during the due diligence process. Once the buyer is non-refundable, they may have controlling rights.

Leasing Costs: the buyer typically pays for commissions and tenant improvements from leases executed after the effective date.

Due Diligence

The buyer will want to review everything they can about the property before they put their deposit at risk by going non-refundable.

Materials: list of materials the seller will supply to buyer. Typical materials include: (i) leases and contracts, (ii) historical income statements, (iii) list of vendors and utilities, (iv) warranties, (v) list of ongoing capital improvements, (vi) details on any outstanding insurance claims, property tax issues, municipal correspondence, and/or legal claims, (vii) seller disclosures of issues affecting the property, and (viii) any other items both parties agree upon.

Inspections: the buyer will have the right to inspect the property, including with their consultants, in a non-invasive way. They will need to get explicit approval from the seller to be able to perform invasive testing.

Representations & Warranties

This is a fancy way of saying (a) what is each party saying is true <a “rep”> and (b) what will each party agree to do <a “warranty”>. They generally focus on the seller and include:

Reps: the seller has the authority to sell the property. The seller is not bankrupt nor has any pending litigation. There are no tenants, leases, and contracts other than the ones provided in due diligence. The due diligence materials provided are true and correct.

Warranties: the seller will maintain insurance. The seller will continue to operate the property in a professional manner leading up to closing.

Damage & Destruction, Condemnation

Damage or Destruction: what happens in the event the premise is damaged or destroyed? The buyer may have the right to back out and keep their deposit if more than 5% of the property is destroyed.

Condemnation: what happens in the event the premise is condemned? The buyer may have the right to back out and keep their deposit.

Closing Process

The PSA documents the details of the closing process including:

Closing Conditions - Buyer: waived due diligence contingency; received title policy from title company.

Closing Conditions - Seller: maintained reps and warranties; delivered required closing documents to escrow.

Closing Costs: list of what buyer and seller will each pay. Seller typically pays the broker commission.

Closing Steps: description of how the escrow company will handle the closing logistics.

Exhibits

Although PSA may be only 15+ pages, there could be 20+ pages of exhibits. These can include:

Legal Description of the Property.

List of Due Diligence Materials.

Form of Deed: this is the legally recorded document that confirms the property has been sold.

Form of Bill of Sale: this documents the sale of any personal property related to the physical property. Examples: parts and materials for repairing the property such as flooring or light bulbs.

Form of General Assignment: this documents the transfer of the various contracts such as leases, warranties, and service contracts.

Form of Estoppel: very briefly, an estoppel is a unilateral statement signed by the tenant for the benefit of a buyer and their lender confirming the key terms of a lease. Estoppels are common in larger commercial transactions.

Any other specifics details relevant to the property such as the status of ongoing capital improvements.

At a Glance: LOI vs. PSA

LOI

Legally Binding: no

Length: 1-5 pages

Purpose: handshake agreement before legal documentation

At Risk: reputation

Lawyer needed: no

PSA

Legally Binding: yes

Length: 15-35+ pages

Purpose: legal contract

At Risk: reputation and money

Lawyer needed: if not using standard forms

How to Digest All of This

That was a lot to cover.

Some of you may be overwhelmed with the amount of detail and feel that it can’t be this complicated. Some of you may feel I am only scratching the surface.

You are both correct.

The level of complexity mainly depends on whether you a buying a 1-4 unit residential property or a commercial property (industrial, retail, office, or multifamily).

1-4 Unit Residential

If you buy a 1-4 unit residential property, whether for your personal residence or as an investment, you will likely use a templated agreement that is literally “fill in the blanks”. You won’t even use a letter of intent.

Everything will be done using the PSA offer and counter offer templates.

No lawyers. No negotiating items you are struggling to understand.

Some of you can breathe a sigh of relief.

Commercial Properties: Industrial, Retail, Office, Multifamily

For the rest of you, you will likely need to take the time to develop a basic understanding of what I described in the LOI and PSA documents.

For deals under $10 million, you may still use standard form PSA agreements like those created by AIR CRE. This is referred to as “using an AIR form”.

The benefit of this approach is that the buyer and seller are each agreeing to most of the items that get negotiated. They can focus their efforts on adding exhibits for items that either (i) fall outside the AIR form or (ii) they want to more actively negotiate.

This can be a great approach and one I support for smaller deals.

For those of you buying larger commercial deals and using customized PSAs, here’s my advice:

Find a Good Lawyer: work with a lawyer who understand the issues that will come up AND is business minded - i.e. they want to figure out a reasonable solution to each item that is negotiated as opposed to proving how smart they are by over negotiating every item.

Get Smart: spend the time needed to understand the issues from a business perspective as opposed to just relying on what the lawyer says. Think through what the issue really means. Ask your lawyer to explain issues in simple language and give you examples of real situations where this language would apply. As the buyer, you make the call on the final language. Not the lawyer. It is your money and reputation.

Red Flags to Watch For

While most sellers are honest, watch out for red flags such as:

Seller resistant to reasonable contingencies > make sure you protect yourself.

Significant items missing from due diligence materials > dig in to make sure the seller is not hiding something important.

Seller rushing you through due diligence > take the time you need but understand that you can never make a “risk free” investment.

Trust your gut and don't proceed with the deal if it doesn’t feel right.

The Purchase Process in 5 Steps

The LOI and PSA are integral steps in the overall purchase process:

Find property (last week’s newsletter)

Submit and agree on a LOI (handshake agreement): 3-7 days

Negotiate and sign a PSA (binding contract): 7-14+ days

Complete the due diligence and go non-refundable (next week’s newsletter): 15-30 days

Close: 15-30+ days

Yes it gets more complicated with additional investors and obtaining a loan, but this is the basic process. A fast process takes 30 days. A more typical process takes 45-90 days.

My Two Cents on How to Think About a PSA

I tend to find the heavy negotiation of PSAs to be overkill.

Why?

If there are issues that come up in the purchase process, reasonable buyers and sellers are normally motivated to work it out regardless of what the PSA says.

View the PSA as your purchase process handbook. It should guide you in the process.

But, remember that your most important asset is your word and your reputation.

Over negotiating the PSA as a way to plant trip wires to out maneuver your counterparty (whether buyer or seller) may help you on an individual deal, but will set you up for being known as a bad actor in the long run.

Be as good as your handshake.

Be a good person.

Life is better that way.

Professor Bateman

How To Find Your First Real Estate Deal: A Step-by-Step Guide

From online research to broker relationships—putting in the reps that lead to your first investment

We have covered a lot so far. Today we are going to dig into how to find your first deal.

Before we do this, let’s do a quick recap of what we have covered:

HOW to invest - REITs, LPs, self, with a partner, or as a GP: 5 Ways to Invest in Real Estate (From $60 to All-In)

WHAT to invest in: Asset Classes Explained: Industrial, Office, Retail, Multifamily, and 1-4 Unit Residential

TAX advantages: 5 Tax Advantages That Make Real Estate Investing So Powerful

BUILDING A TEAM: You Don’t Have to Do Everything Yourself: Building Your Real Estate Team

Finding your NICHE: Stop Chasing Every Deal: Why Successful Investors Pick a Niche

Choosing your STRATEGY: The Risk-Return Spectrum: Choosing Your Real Estate Investment Strategy

How to UNLOCK VALUE: Unlocking Value: What to Do After You’ve Improved Your Property

The simple MATH of real estate: Cap Rates: The Simple Math of Real Estate Investing

Moving forward we are going to address the practical realities of:

BUYING real estate investments: picking a market; working with a broker; analyzing deals; purchase and sale agreements; debt and equity; due diligence; and closing.

OPERATING the property: value add initiatives; leasing; property management; construction; reporting; insurance; and property taxes.

SELLING your property: working with a broker; preparing the property for sale; due diligence; purchase and sale agreements; debt and equity considerations; and closing.

Today marks the start of the series of several newsletters that will explain buying real estate investments.

Let’s dig in.

Understanding What You are Looking For

If you don’t know what you are looking for, you will be like a blind squirrel searching for a nut. You may find it eventually, but you will waste a lot of time in the process.

A few weeks ago I discussed the importance of finding your niche and determining your investment strategy. Let’s build off these concepts and our previous examples.

In the niche newsletter I created four examples of different combinations of asset class, geography, and strategy based on an investor’s time availability:

No spare time: Retail - Tacoma, WA - Turnkey.

No spare time: 1-4 Unit Residential - Nashville, TN - Turnkey.

Some time to be more active: Industrial - San Antonio, TX - Light Rehab.

Time on evenings & weekends: 4 Unit Residential - Los Angeles, CA - Value Add.

Regardless of the asset class, geography, and strategy, the methodology is the same.

Getting in Your Reps

The first step is to start looking at deals. The great news is that you can do this after hours and on the weekend from the comfort of your own home.

How?

By using the power of the internet, your time, and (to quote the musical Hamilton) your “top-notch brain”!

There are many websites out there that list properties for sale:

LoopNet.com - best for commercial properties (industrial, retail, office, larger apartments/multifamily).

Redfin.com or Zillow.com - best for 1-4 unit residential.

Realtor.com - MLS-connected; comprehensive for residential.

Note that Redfin, Zillow, and Realtor will also be filled with properties for sales to homebuyers to live in.

Pick one or two and set the filters to the parameters that fit your asset class and geography niche, as well as your price range. You won’t be able to filter by strategy (turnkey, light rehab, value add). To figure this part out, you will need to review the details of the property listings.

Step 1 - Go Down the Rabbit Hole

In your first pass, dedicate 1-2 hours to click around. Think of this like doom scrolling. You are reviewing the information in a general way to get a lay of the land.

Pay attention to how the assets (and the process) make you feel. Is there real interest in this niche? Do you get excited? Does this put you to sleep?

Do you feel like you could come up with the equity (cash) to buy the property - assume you need 35% of the purchase price - example: $300,000 property x 35% = approximately $100,000 of equity.

If it puts you to sleep or is out of your price range, consider exploring another niche.

Don’t give up. Finding your niche is an interactive process that takes time.

Step 2 - Bring Some Structure

Now it is time to be more methodical by bringing structure to the process.

Get a pencil and a piece of paper (or open excel). Create a simple grid that lists the following details as columns for each property. Each property will be a row.

Address

City or submarket

Square feet or number of units*

Asking (purchase) price

Price per square foot or per unit*

Rough calculation of annual net operating income (NOI, which equals revenue minus operating expenses). This should be on the listing or you can make an estimate.

Cap rate: NOI divided by price.

*Use units for multifamily and 1-4 unit residential. Use square feet for retail, industrial, and office.

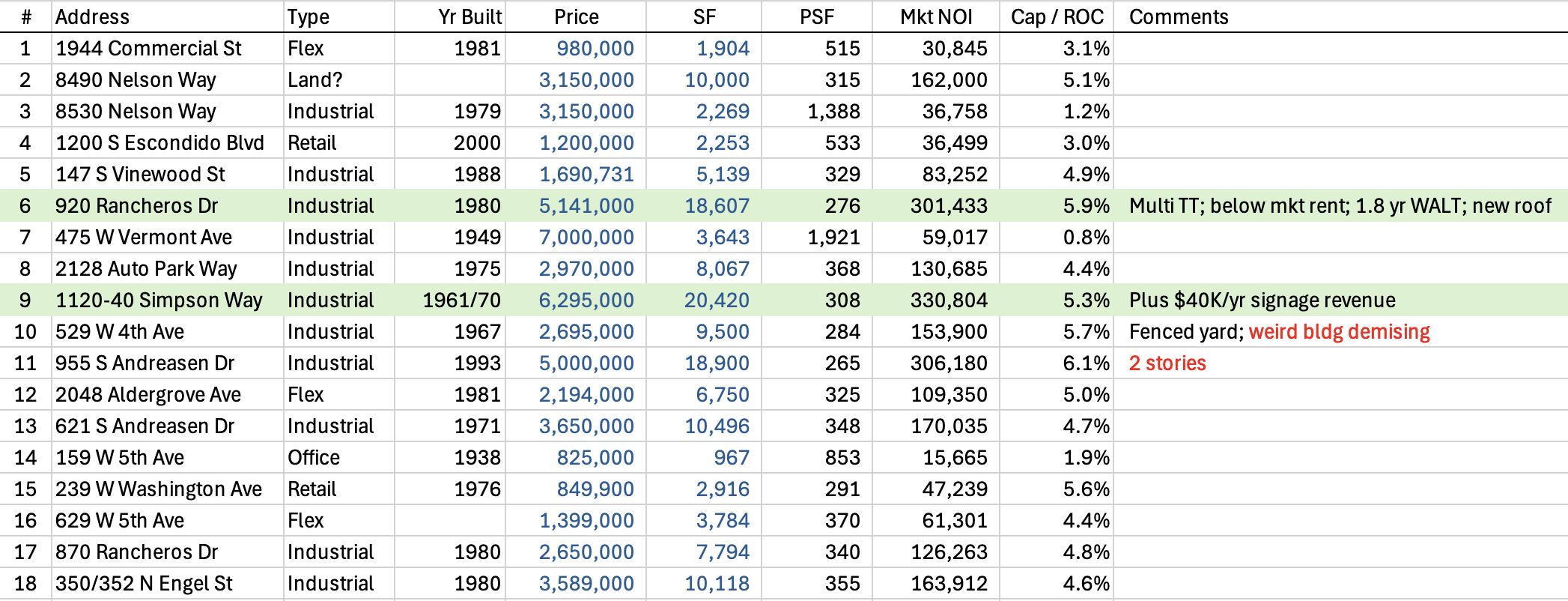

I did something similar for industrial properties in Escondido, CA on LoopNet last summer.

Example: My Escondido Industrial Property Search (Summer 2025)

What you are looking for is the properties that are a little better than the rest. In this case I was using cap rate (aka return on cost) as my main guide (column header is “Cap / ROC” in the table above.

Alternatively, I could have used price per square foot (“PSF” in the table above).

For each of the properties that had the higher cap rates (#s 6,9,10, and 11), I reviewed the materials on LoopNet in more detail and added some comments.

I didn’t like #10 and 11 because of some of the physical characteristics shown in red in my Comments column.

This left me to focus on #s 6 and 9.

The whole process took me a few hours.

Step 3 - Talk with Brokers

What?!?!

You mean I have to call someone I don’t know?!

Yes. You can do it. It is just another human being on the other end of phone.

To set you up for success, let’s breakdown the role of a broker.

In regards to looking at a property for sale, the broker that is listed on LoopNet or similar websites is hired by the seller to market the property for sale. The broker only gets paid (by the seller) if the property is sold. Said another way, they are spec’ing their time in hopes that they can successfully sell the property at a price that is acceptable to the seller.

Part of the role of a broker is to talk with prospective buyers about the property they are trying to sell.

They are working through the traditional sales funnel.

They have to talk with many potential buyers.

Some of those will turn into actual leads that spend time focusing on the property.

A smaller amount will actually make offers.

And one will (hopefully) be acceptable to the seller and buy the property.

So what does this mean for you?

If you call a broker and come across as being clueless and unorganized, the broker will see right through you and be unlikely to want to give you any time. A broker’s most precious resources are their time and reputation.

Don’t waste their time.

Be respectful.

Brokers are an essential part of the real estate investing process. A good relationship with 1-3 good brokers may turn out to be the most critical part of your personal real estate team. They are the source of the majority of investing opportunities out there.

But what if you are just starting out? What is realistic for you?

Here’s a script that I recommend:

You: Hello [broker’s name]. I am reaching out to learn more about [XYC property] I saw on [LoopNet]. I have spent the last X weeks researching properties like this in this market and this one stood out to me as one I want to learn more about.

Broker: Good to hear from you. Can you tell me about yourself before I walk you through the property? [Translation: are you someone I should spend my time on?]

You: Happy to. I am newer to real estate investing, but am ready to buy my first deal. I picked this market because XXX. I have the equity to buy a deal of this size (or have lined up investors). I have some ideas on putting a loan on the property, but would also welcome your perspective on loan options. I am looking to establish one or two key broker relationships with the goal of buying multiple properties over the next X years. What questions should I be asking about this property and the market?

—

What works about the script above?

You are being candid in the realities of being new.

You are showing that you have put in the time to focus on a niche.

You are making it clear that you have a path to getting the equity.

You are opening the door to a long-term relationship with this broker.

So what’s next?

Step 4 - Patience and Repetition

Now you need to keep doing steps 2 and 3 until you find a deal that works for you.

Expect to take 3-6+ months until you find a deal that works for you that you can get under contract. This includes:

Building market knowledge (4-8 weeks).

Establishing broker relationships (2-6 weeks).

Finding and analyzing the right property (4-12 weeks).

Expect to review 20-100+ properties online and dive deep into 5-20 of these before you find the right deal for you.

New properties become available for sale all the time. Establish a routine where you check for new properties for sale every two days.

By putting in your reps, you will start to better understand your niche and what works best for you. At some point you will see a property that checks all your boxes and is priced at a level that makes sense to you.

By then you will have talked with multiple brokers and seen many deals. Some of these brokers will even start sending you deals proactively, possibly even before they hit the market.

Important note on 1-4 unit residential deals: make sure you work with a broker that specializes in investment properties, not the homebuyer market. Investment brokers will understand how to analyze a property from an investment perspective.

You will have built a level of micro expertise in your market and established some small level of credibility with brokers in that market.

Most people have very little staying power. They try something and quickly give up.

Be the exception.

Pick a niche.

Be respectful of brokers’ time. Leverage their market expertise.

Put in the time and focus to understand the market.

Before you know it, you will have found a deal that looks like it works for you.

So what do you do when this happens?

Call the broker immediately - good deals move fast.

Ask for the offering memorandum or marketing package that provides the details about the property.

Request a tour if you are local to the market (or even a video tour if you are not).

We’ll cover the purchase process in detail next week.

Professor Bateman