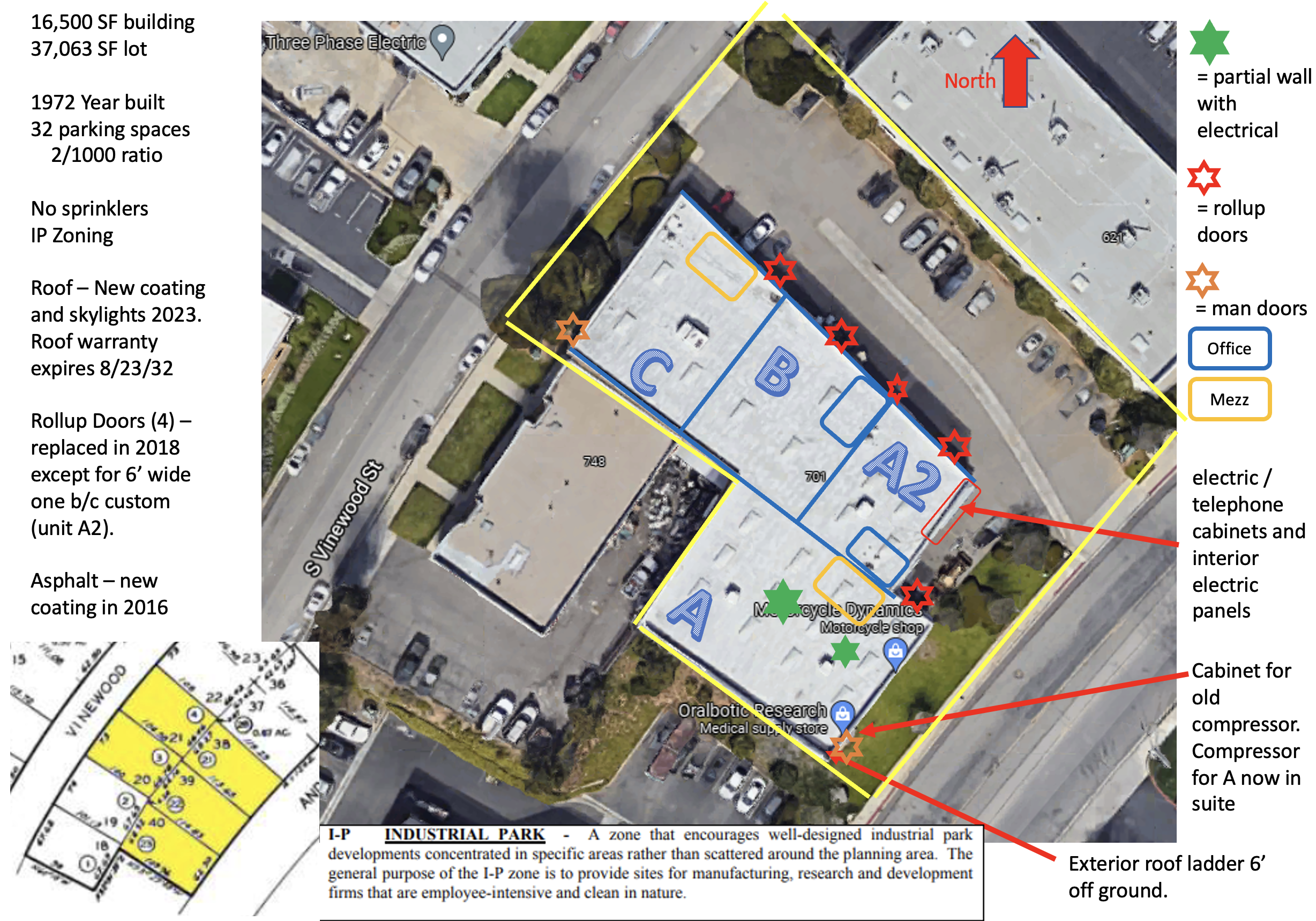

Vendor Service Contracts: What You Need To Know

A simple contract you will use over and over again

Welcome to another newsletter of Real Estate Investing Explained.

Today’s topic will mark the end of the series on Operating & Managing Real Estate. In this series we covered the foundation of operations including:

Next week we will be moving on to the series on Executing Your Business Plan where we will cover leasing, construction, and ways to add value.

But before we get there we need to cover service contracts. These are legal documents that are used to engage another company to do work at your property. It could be one-time or on a recurring basis.

Examples include landscaping, pest control, cleaning, HVAC service, and many other services.

If you own a home, you might be used to bringing in vendors and technicians to fix something. You are unlikely to sign a contract. You simply pay them when the work is done.

With real estate investment properties, particularly commercial, a better practice is to use a service contract to document the details in advance including:

Who is the owner.

Scope of work. How the work will be performed and to what quality.

Whether there is a warranty.

Costs and payment timing.

Duration, frequency and termination.

Insurance required.

Many other “legal” sections if prepared by a larger real estate company such as confidentiality, indemnities, dispute resolution, notices, limitations of liability, non-discrimination, OFAC compliance, and some others. Don’t worry about these sections for this discussion. You can understand them later if you develop a larger portfolio.

Yes, it is more cumbersome. But a little bit of paperwork up front will save you misunderstandings and problems in the future.

Today I will explain each of these and why they matter.

Let’s dig in.

Who is the Owner

Do you own the property as an individual or through a separate legal entity such as an LLC? There are pros and cons to each.

Individual:

Pros: easier to get a loan for a 1-4 unit residential property. Lower annual tax cost.

Cons: more risk of personal liability.

Legal Entity Such as a LLC:

Pros: additional layer of legal protection.

Cons: annual LLC tax and separate tax return.

Whatever you choose, you need to make sure the service contract lists the “Owner” correctly. If you own a property through an LLC (ex. 123 Main Street Owner, LLC), don’t list and sign the contract under your name individually. Sign it under the LLC. In this case, the LLC is the owner.

Scope of Work, How the Work Will Be Performed and To What Quality

This describes what the vendor is going to do. It might be monthly landscaping or repairing a broken HVAC unit.

A simple approach can be to ask the vendor for a proposal and then include the proposal as an exhibit to the service contract. The exhibit serves as the details of the scope of work. This way, everyone is clear and in agreement.

You could also consider adding language saying something like: “work shall be performed in a professional manner to industry standard quality”. It is not perfect, but it does set some basic expectations beyond what is written in the proposal.

Whether There is a Warranty

Not all work will include a warranty, but some should.

Anything new, such as an HVAC unit, should include a warranty. You want at least one year.

The contract is where you agree what the warranty will be, what it will cover, and how long it will last. The vendor may also give you a separate warranty document once the work is complete.

Costs and Payment Timing

A clearly documented scope of work and list of costs will reduce the chances of there being disputes after the work is complete. They go hand in hand.

If the scope is not clear, the vendor may hit you with “change orders”. Change orders are a fancy way of saying that the vendor is going to charge you more than the amount in the contract for various reasons including (i) increased scope of work or (ii) unforeseen or unanticipated conditions.

Unscrupulous people may even try to hit you with a change order because they feel they aren’t charging enough or this is part of their strategy (low bid to get the work then multiple change orders).

Avoid the risk of change orders by being clear on the scope, the costs, and the timing under which you, as owner, will pay them.

And don’t necessarily take the lowest bid if it is materially below the others. This can be an indicator of a vendor who doesn’t understand the scope.

Let’s move on.

Duration, Frequency, & Termination

This describes how long the agreement lasts and the frequency of the work. This varies depending on the type of work. Examples:

Landscape Maintenance: this could be a one year contract where the frequency of service is bi-weekly or weekly.

HVAC Repair: this could be a one-time service that needs to be done in 30 days, after which the contract is done.

For recurring services such as landscape maintenance, the practical approach is to have a one year contract that can be renewed at an agreed upon rate (example 3% increase) with 30 days notice.

There should also be language that either party can terminate with 30 days notice if one party is not following the agreed upon terms of the contract.

Let’s transition to insurance.

Insurance

We talked about insurance in Real Estate Insurance: The Transfer of Risk.

Any time someone is coming to work on your property, there is the risk that (a) they could hurt themselves or someone else or (b) they could damage your property.

You want to require each vendor to have some basic types of insurance such as worker’s compensation to protect their employees and commercial general liability to protect you and your property. There are many other types of insurance that could be requested, but these are the two major ones.

Now that we have covered the components of a service contract, let’s discuss where to find one and how to use it on a day to day basis.

[Note: I am not discussing the “legal” sections referenced in the introduction as giving legal advice is not part of my scope.]

How to Get a Service Agreement Template

Now that you understand the basics of what is in a service contract, what do you do with the information? How do you get a contract?

As discussed in The Property Manager: On the Front Line of Your Property, I believe there is real benefit to hiring a property manager.

A good property manager will have a standard service contract that they use. The great ones will be able to talk you through their form and explain it to you.

Don’t feel you need to reinvent the wheel. Review their template. If it looks good, use it or make the edits you need to make it work for you.

My Perspective

I believe in using service contracts, but I like them to be short and easy to understand.

I am also mindful that asking a vendor to sign a form they are not familiar with slows down the process. Sometimes the vendor will even have to talk with a lawyer to confirm they are ok with this. This can really slow down the process when you are trying to get work done.

I try to be reasonable.

If the vendor has their own form, I am willing to read it based on the information described above. If it is clear, then I am willing to sign it. Other times I might hand-write edits to the document to make something more clear or to make a small change.

I try not to get caught up in going back and forth on language in a document. I want to focus the majority of our efforts on getting work down at the property, not negotiating documents.

Some might say this is taking on more risk than I need to. Fair enough.

But remember that real estate investing is not risk-free. There are always things that could go wrong. If that scares you, real estate investing may not be for you.

Don’t be reckless.

Be practical and reasonable.

I try to do business with vendors (and people in general) I trust. If an issue comes up outside of the contract, we work it out as two reasonable people.

Property Tax: The Expense That Never Goes Away

The ongoing expense that varies from state to state

Last week we discussed insurance in detail. Today we are getting into property taxes.

My original plan was to do them as a combined newsletter, but when I started writing about insurance I realized just how many layers of information there are.

Why was I planning to cover them in a single newsletter? Because they share multiple similarities:

The amount of each expense is largely outside of your control.

They are generally permanent. You could get rid of almost every other expense, but property taxes and insurance will always be with your property.

They are specialized subjects that benefit from the owner having a certain amount of knowledge and expertise.

But…property taxes are simpler to explain than insurance. Phew!

Today we will discuss:

Why property taxes exist and what they fund.

How they are determined.

Ways to reduce your property taxes.

Owner best practices.

That’s it. Much more simple than insurance.

Let’s dig in.

Why Property Taxes Exist and What They Fund

Property taxes are revenue for the county the property is located in.

Read that word carefully: county. Not the state.

They are the way each county (in each state in the U.S.) funds basic services such as public schools, police, and libraries. A portion of the revenue is sometimes distributed to each city within that county. [Yes, this is a U.S. centric newsletter.]

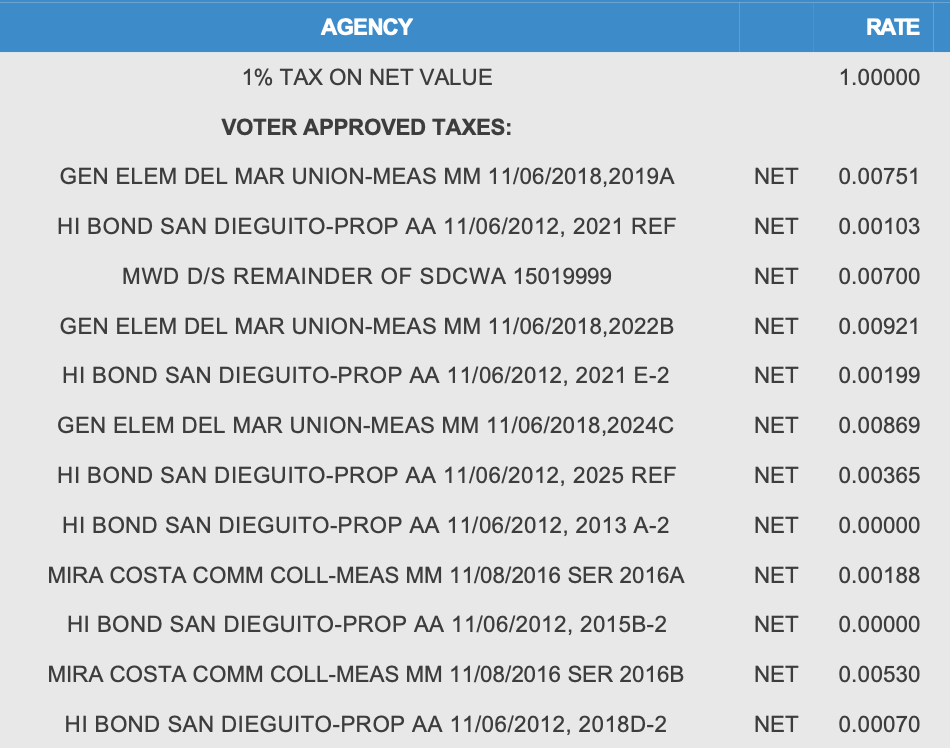

You may have seen a proposition or other measure on your local election ballot that talks about adding an additional fee to homeowners to fund XYZ. If passed, this would add to every homeowner’s property tax expense. Here’s an example of a property tax bill with propositions and measures that passed the voting ballot and were added to each homeowner’s property tax bill:

Table 1: Example of Propositions on a Property Tax Bill (California). Each one increased the “rate”. More on this later.

To add another layer of complexity, property taxes are determined at the state level but administered, collected, and used at the county level.

Your main takeaway should be that property taxes fund your local government and services. They are never going away. All 50 states have some type of property taxes.

But wait - some of you may be thinking that certain states don’t have property taxes. This is not correct. Some states don’t have income taxes or sales tax, but every state has property taxes.

Let’s transition to how they are determined.

How Property Taxes Are Determined

As I said above, every state has property taxes. But unfortunately every state calculates them in a different way.

Here are the similarities across all states:

County Assessor: the team at each county that determines, administers, and collects property taxes.

Assessed Value: the value of the property and land as determined by the county assessor.

Rate: a percentage that is applied to the assessed value to determine the property tax.

Here are the differences:

Assessment Methodology: how the assessed value is determined (generally, but not always, via fair market value appraisal).

Assessment Frequency: how often the assessed value is determined (every 1-4 years).

Payment Timing: frequency and timing of payment throughout year (1-4 times per year).

Payment Period: whether the payment is in advance or in arrears.

Appeal Options: whether and how the property taxes can be appealed with the goal of reducing them.

So we have a basic framework (the similarities), but a unique way of implementing it within each state (the differences).

Here are some examples:

California

Assessment Methodology: the value is determined by the most recent purchase price and then grown at 2% per year. That’s it. Super simple. That is why you hear of people that have owned their property for 30+ years and have a low property tax basis (and expense), while the person next door who recently bought their property has a much higher property tax basis (and expense).

Assessment Frequency: July 1 every year add the 2% increase and adjust for propositions and measures.

Rate: a little over 1%. Example: $1,000,000 x 1.132% = $11,320.00 per year.

Payment Timing: twice per year in December and April.

Payment Period: December covers the second half of the year (7/1 to 12/31). April covers the first half of the year (1/1 to 6/30).

Appeal Options: through property tax consultants, who do not need to be licensed.

Texas

Assessment Methodology: fair market value appraisal.

Assessment Frequency: beginning of each year.

Rate: changes each year.

Payment Timing: January of the year after assessment.

Payment Period: 100% in arrears.

Appeal Options: typically through a lawyer.

These are just two examples. Each of the 50 states in the U.S. has a different approach.

Ways to Reduce Your Property Taxes

There are ways to appeal and reduce your property taxes. Why would you want to do this? To reduce your operating expense. And you may feel the assessed value is unreasonable.

If you own properties in multiple states with different rules, it may be helpful to use a property tax consultant such as Ryan.

The typical structure will be that they work on 100% contingency. They only get paid if your property taxes are reduced. Example: they might keep 10% - 30% of the reduction as their fee.

My personal opinion is that property tax consultants serve an important role in the industry as this is a specialized area of expertise that varies from state to state. These consultants can help save you money and estimate your future property taxes for properties you are purchasing.

My approach has been:

Personal Home: I appealed this one myself because (i) I understood the California process and (ii) I live in a 100+ home community where the homes are very similar, making it easy to supply sales comparables. I had bought my home a couple years before the Great Financial Crisis of 2008. By successfully appealing my property taxes, I saved quite a bit of money each year.

Industrial Portfolio: when I worked for a company with 100+ properties across many states, we used property tax consultants. It was too complex and labor intensive to justify using one of our internal team members.

Educate yourself by talking with a property tax consultant. If you own a small property (less than $5M), find a smaller local property tax consultant who may give you more focus than a larger, national firm.

Owner Best Practices

Here are my recommended best practices when working on property taxes for your investment property.

Due Diligence & Underwriting - Assessment Methodology

Remember, these vary from state to state. Don’t assume the seller’s property taxes will be your property taxes growing at inflation each year.

Do the research and/or talk to a property tax consultant before you commit non-refundable money towards the purchase of the property. You need to understand how they will change during your ownership.

Propositions & Measures - Expiration Dates

These often have an expiration date. This is especially important when you see a very large additional charge on a property tax bill.

My former company once bought a property where the additional charges were as much as the base property tax bill. This was related to a fee that would expire two years after our acquisition. Knowing the near term expiration changed the way we thought about the deal.

Closing Statement - Payment Timing

The timing of the payment will determine how the property tax expense is prorated in the closing statement on closing day. This could be a big charge or credit.

For example, if property taxes are paid in advance, you (as buyer) could find yourself owing the seller for their prepayment and have to pay this amount through the closing statement.

What would this mean? You could be short on cash on the day of closing. Understand this in advance to avoid surprises.

Appeals

Be proactive. It doesn’t cost you anything to have a conversation with a property tax consultant. If there is a way to save money on your property taxes, you should consider this.

Pro tip: there is usually a deadline by which you must file the appeal. Do the research so you don’t miss it.

Remember, property taxes vary from state to state. Take the time to understand how things work in the state you are buying the property.

As always, have a learning mindset. Be patient. Talk to experts. Take the time to understand it.

Real Estate Insurance: The Transfer of Risk

A breakdown of the different ways you can (and should) insure against risk

Today we are going to dive into the world of real estate insurance.

I have spent a LOT of time on this subject in the 20+ years I worked full time for real estate companies.

Insurance is a fascinating financial product that shares similarities to:

Private equity, venture capital, and stock investing.

Investment banking.

Sports betting and assembling a professional sports team.

In each case someone is making a calculated and well researched investment (or bet) in hopes that they will make money.

Insurance is a financial instrument where insurance companies earn smaller guaranteed payments (premiums) while putting big dollars at risk (claims). Their goal is to make more money on the premiums than they pay out in claims over years and decades.

I will break down the basics of real estate insurance in a way you can understand and use. As a real estate investor, you will need (and likely be required to carry) insurance to protect you, your investors, your lender, and your property.

Today we will cover:

What insurance actually is

Types of real estate insurance

Premiums, limits, deductibles, policy term, & exclusions

Insurance policies

Insurance certificates

Lender insurance requirements

Working with an insurance broker

How to handle an insurance claims

Why you should strive to be a good customer to the insurance carriers

Let’s dig in.

What Insurance Actually Is

At its most basic level, insurance is a financial transaction: small amounts of guaranteed money for major risk protection.

For example, you own a property that would cost $200,000 to re-build if it were destroyed. You don’t have $200,000 sitting around, so you would be in a bind if the property were destroyed.

Enter the insurance company aka carrier (ex. State Farm, Liberty, Allstate, etc).

They offer to insure the property for $1,000 per year.

You pay the $1,000 at the beginning of the one year policy.

The insurance carrier will pay the cost to rebuild the property IF it is destroyed. Either way, they keep the money you paid them.

This same concept applies to many other types of insurance: auto, life, health.

The person buying insurance pays a small fixed amount. The insurance carrier keeps the money and only pays if there is a claim (damage, a medical procedure, etc.).

Now let’s get specific to real estate insurance.

Types of Real Estate Insurance

I am going to focus on insurance you would have as a personal real estate investor.

[Note: if you own a real estate company (or any other company) with employees, there are many other types of “corporate” insurance you would want such as worker’s compensation, crime, etc. Talk with your insurance broker to learn more.]

There are two types of insurance you will want as a real estate investor: property and liability.

Property Insurance - Insuring Physical Objects

Property insurance covers physical objects from damage, theft, and destruction. Effectively, anything that could harm the object. In the case of real estate, “objects” are:

The building and anything attached to it such as HVAC and lighting.

Any supplies stored in the building such as light bulbs and carpeting.

12-24 months of rental income you could lose while the building is being repaired if the tenants are unable to occupy the building and pay rent.

Think of property insurance as insuring against damage. How could the property be damaged? Fire, theft, hail, storm, wind, earthquake. It could be anything.

Liability insurance is totally different.

Liability Insurance - Insuring You From Being Sued

Liability insurance covers you if you are sued.

Let’s say your tenant or one of their customers/employees trips just in front of the entrance to the tenant’s suite. They break their arm and have medical bills. They could sue you.

If you are sued, the liability insurance coverage kicks in to defend the lawsuit and pay for damages (if any).

In summary, property insurance protects the building and rents. Liability insurance protects you if you are sued.

Pro tip: For additional liability protection beyond your standard policy, consider an umbrella policy that provides extra coverage (typically $1-5M) for a relatively low premium.

Additional Pro Tip: If you are developing a property from the ground up, property insurance will be known as “Builder’s Risk” and liability insurance will be known as “Owner’s Interest”.

So far, so good.

Now let’s dive a level deeper.

Premiums, Limits, Deductibles, Policy Term, & Exclusions

There are five key factors that come into play with insurance:

Premiums: how much you have to pay for insurance each year.

Limits: the maximum amount the insurance carrier will pay if there is a claim.

Deductibles: a small amount you pay if there is a claim (in addition to the premiums).

Policy Term: the length of the policy (ex. 12 months).

Exclusions: what is NOT covered.

Let’s briefly discuss each one.

Premiums

Premiums are the fees you as the person buying insurance pay. It is the insurance carrier’s revenue.

Limits

Limits are the maximum amount the insurance carrier will pay if there is a claim. Two examples:

$200,000 property claim and the policy limit is $150,000.

The carrier will pay $150,000 (policy limit < claim).

$100,000 property claim and the policy limit is $150,000.

The carrier will pay $100,000 (policy limit > claim).

Pay attention to your limits to make sure they give you adequate coverage.

Deductibles

If you have ever paid attention to a health insurance claim, you are probably familiar with a deductible. It is the additional amount you have to pay (in addition to your premium) in the event there is a claim. In the $200,000 example above, the deductible might be $1,000. You would pay this as part of the claim, but you only pay it in the event that there is a claim. The concept is that you will have to cover minor costs and the insurance carrier only steps in for more “major” claims.

Policy Term

This is the length of the policy. Most policies for real estate are 12 months.

Exclusions

Certain events will not be covered under your typical property or liability policy. If you want this coverage, you will need to buy a separate (and often more expensive) policy for this specific risk. Sometimes they are included in your property policy with higher deductibles. Examples of exclusions include: (i) earthquake risk in California, Oregon, and Washington, (ii) hurricane risk in the Gulf of Mexico region, (iii) hail risk in Colorado and Texas, and (iv) environmental pollution.

Note that “wear and tear” is almost never covered by insurance. The 20 year old HVAC unit that stops working will not be a covered claim.

Pro Tip: Look out for “vacancy exclusions”. Vacant buildings are at higher risk for theft and vandalism. Most policies exclude coverage for vandalism and theft for buildings (not suites) that have been vacant for 90+ days. Make sure you read your policy to understand this risk and consider better lighting and/or security for vacant buildings.

Let’s transition to the actual policy.

Insurance Policies

An insurance policy is the document provided by the insurance carrier. It is a legal document that outlines all the terms of the policy.

In an ideal world you would receive a draft of the document 30 days before the start of your policy period. In the real world, these normally come 10-60 days after the policy starts.

A good insurance broker will help you negotiate the best deal points of the policy and compare the options from multiple insurance carriers.

Think of the insurance policy as adding all the specific details of the items we have discussed so far (premiums, limits, deductibles, etc.).

The policies are long and written as legal documents. For the industrial property I own, the policy is 50+ pages. A practical approach for those of you who cringe at the idea of reading one is to focus on the following:

Is your name and/or legal entity correct?

Is the property address correct?

Are the dates in the policy term correct?

Review the premium, limits, deductibles, policy term, & exclusions.

Review the vacancy exclusion language.

Make sure you know who to contact if you have a claim.

Most of the time you won’t have a claim. But when you do, you don’t want to be caught discovering that you didn’t have the coverage you thought you did.

Is there an easier way to understand your policy?

Yes.

Enter insurance certificates.

Insurance Certificates

Whereas a policy includes all the legal language of your policy, an insurance certificate is a one page document that summarizes your policy.

It will list the type of coverage (property, liability), limits, deductibles, policy term, and sometimes exclusions.

It is also where the insurance carrier will add “additional insured” parties as required by other documents you sign such as a property management agreement or loan agreement.

An “additional insured” has limited coverage under your policy in the event of a claim without having to pay anything for this coverage.

This is especially true for lenders.

Lender Insurance Requirements

If you have a loan on your property, you will have a set of loan documents as discussed in Debt: An Amazing Tool with Strings Attached.

The loan documents will list various lender insurance requirements that must be met for the lender to give you the loan.

These could include:

The types of coverage: property, liability, earthquake, etc.

The amount of coverage: example - property insurance equal to the full replacement cost of the building.

The maximum deductible allowed: example - $1,000 or $5,000.

Make sure you price out insurance coverage that meets the lender requirements BEFORE you sign the loan agreement.

An insurance broker can be very helpful in this process

Working With an Insurance Broker

You want to work with an insurance broker that specializes in real estate insurance.

They will help you compare insurance options to find the best combination of price and coverage. They know what is “market” and they will help you find the right fit for you.

Ask people you know who have invested in similar properties for a referral. A good insurance broker will make a world of difference.

They will also help you work your way through a claim.

How to Handle Insurance Claims

Insurance claims are a whole separate animal. They can be simple or long and tedious.

I won’t go into much detail, but here are what I believe are the best practices having navigated claims ranging in size from $25,000 to $10,000,000+.

Communicate early. If you think there MAY be a claim, let your insurance broker and carrier know immediately. There is no penalty or risk of an increased premium next year if there doesn’t end of being a claim.

Ask questions. You will likely be assigned a “claims adjuster” by the insurance carrier. Ask for clarification of the process and timeline.

Be persistent. Claims adjusters often have an unmanageable workload. Don’t be a jerk, but be persistent.

It is a process. Not a fun one, but one that can be navigated. It will help if you are already a good customer.

A note on asset classes and claims. Different asset classes tend to have different types of claims and frequency of those claims.

Multifamily and 1-4 Unit Residential: highest claim volume from “slip and falls” and kitchen fires.

Retail and Office: “slip and falls” are most common claims.

Industrial: theft of copper and other “recyclable” materials are most common claims.

Go in eyes wide open as you consider your asset class and strive to be a good customer.

Why You Should Strive to Be a Good Customer to the Insurance Carriers

What does it mean to be a good customer to the insurance carrier? It means:

You pay your premiums on time. This is their revenue.

You maintain your property well and have good standard operating procedures. This leads to lower risks of claims.

You are loyal. You don’t switch carriers every year.

An insurance company will look at you (their customer) in terms of how you have performed over the life of the relationship. Remember that their goal is to make more money on the premiums than they pay out in claims over years and decades.

You are more likely to have lower premiums each year (and a better claim outcome) if you have been a customer for five years without a claim than if you are three months into your first policy year with the company.

Don’t necessarily change carriers every year to save a few bucks. Think of it as a long term partnership.

Pro tip: as you build up a portfolio of properties, look into putting them into a single “portfolio” insurance policy. This could save you money and make things simpler to operate.

Closing Thoughts

Don’t be intimidated by insurance. Understand that it plays an important role in the world of real estate investing.

View it with curiosity and always be learning.

The Property Manager: On the Front Line of Your Property

Why the relationship with your property manager is so important

As we did last week, let’s anchor in on where we are in the process of learning how to be a real estate investor.

You own your first property.

You have a business plan and are in the early stages of executing it.

You have hired a local property manager.

You are eyes wide open that unexpected issues will come up.

You understand how to review the monthly reports.

Today we are going to discuss how to work effectively with your property manager.

Your property manager is on the front line of your property. They are the main point of contact with tenants and vendors.

Your tenants’ experience of the property will be based on four things:

Where the property is physically located.

How much rent they have to pay.

The physical condition of the property.

How the property manager responds to their requests and challenges.

You can’t change the location and you want to maximize the rent. The physical condition is generally fixed other than the ability to maintain it and possibly improve it.

It is the performance of the property manager that is the most malleable. It is one of the few things that you as the property owner have the ability to influence.

Today we will discuss:

The role of the property manager.

Why being a property manager is so challenging.

When to hire a property manager and how to find a good one.

The importance of setting clear expectations relative to your operational philosophy and goals.

How much discretion to give the property manager.

What to do when things aren’t working out.

Let’s dig in.

The Role of a Property Manager

A property manager is the person or team that manages the property for you on a day to day basis. They will likely be an employee of the company you hire to manage your property.

In addition to the monthly reporting package generated by their team, they have two main focus areas:

Tenants

Vendors

Tenants

Property managers respond to tenant requests and give tenants direction. They use the lease (and instructions from the owner, if any) to determine how they respond to issues. Here are some examples of issues that will come up with tenants.

The tenant is paying rent late.

The HVAC unit in the tenant’s suite stopped working and needs maintenance.

The tenant is leaving trash in the common area.

The property manager has to interpret how to handle the issue, get approval from the owner, communicate the resolution to the tenant, and make sure the tenant cooperates.

This is very easy to say, but hard to do.

Vendors

Property managers also hire vendors to maintain, repair, and upgrade your property. Some of this is done proactively. Some of this is done reactively. You as the owner set the direction of the maintenance standards, but it is the property manager who has to execute this. Here are some examples of issues.

Exterior maintenance relative to cleanliness and the landscaping.

Preventative maintenance (if any) of the building systems.

Want to operate your property like a slum lord? It falls on the property manager to execute this and face the consequences of the unhappy tenants.

Why Being a Property Manager is So Challenging

Let me state this clearly:

The role of a property manager is one of the hardest in the real estate industry.

Why?

There are multiple reasons:

Lack of Time Control: a property manager is faced with a variety of issues each day, many of which are unplanned and time sensitive. Things break. Emergencies happen. Property managers have a very hard time keeping control over their schedule and time.

Workload: property management is a low margin business. Owners of property management firms tend to overload their property managers with a heavy workload.

Context Shifting: a property manager is a jack of all trades. From communicating with a tenant, to analyzing a lease, to reviewing and commenting on a financial report, to preparing a vendor contract, to interpreting a technical building issue - a property manager has to do it all, often in a single day.

80/20: 80% of what happens at a property goes well and unnoticed. It is the 20% of issues that go wrong (most of the time outside of the property manager’s control), that get noticed and complained about to the property manager. It can be a thankless job.

Let me say it again.

The role of a property manager is one of the hardest in the real estate industry.

The good ones do all of this with amazing customer service and keep everyone happy.

I have SO much respect for property managers.

When to Hire a Property Manager and How to Find a Good One

Some of you may be considering managing the property yourself. That is fine, but proceed with caution.

I did this for a year on my property. It is like taking on a part-time job. Once I received an emergency call while on vacation with my family, I realized I would much rather pay someone else to do the work.

Hiring a property manager is particularly important if any of the following criteria apply to you:

You don’t live near the property.

You have a full time job.

You have a low tolerance for customer service issues.

You put a high value your time and mental peace.

The good news is that there are great property managers out there. Here’s how to find one.

Ask for referrals. Search the internet. Ask AI. Note: referrals are the best.

Interview 2-3 firms. Yes this will take time, but it will give you a good comparison.

Check references. What are their existing clients saying.

Request an example monthly report.

Discuss your operating philosophy and goals.

You don’t always want to go with the cheapest option. Find the one that has the right balance of costs and service - and who is on board with your philosophy and goals.

A note of fees: property managers typically charge a fee based on percentage of rent collected from the tenants each month. This varies by market and property type. Here’s a rough range to give you an idea:

1-4 Unit Residential: 8-10%

Large Multifamily, Retail, Office, and Industrial: 3-5%

They may also charge fees for construction management, leasing, and other “one time” services.

Once you select the right property manager for you, make sure you set clear expectations.

The Importance of Setting Clear Expectations Relative to YOUR Operational Philosophy and Goals

In a previous newsletter - Daily Issues You Will Face While Owning Real Estate - I discussed the importance of being clear on your own operating philosophy using three types of cars as an analogy:

Do you want to operate the property like a top of the line Mercedes, a reliable but basic Honda, or a car that constantly breaks down?

If you don’t understand your own philosophy and goals, your unfortunate property manager will either (a) constantly be guessing at how to handle issues and coming to you regularly for direction or (b) taking action on issues that may or may not be what you want.

Take the time to be clear on your philosophy and goals.

Once you do this, you can set the framework of a good working relationship with your property manager that will benefit your property. Here are the specific steps I recommend:

Send an email to the property manager explaining your philosophy and goals.

Meet with the property manager onsite to walk the property and discuss your philosophy and goals. Make sure you take the time to get to know your property manager and understand their daily workload outside of your property.

Agree upon expectations for how the property will be operated day to day.

Agree upon how often you will have a call or meeting and what will be covered. This will be much more efficient than ad hoc communication.

Agree upon what communication should fall outside of the call/meeting schedule. What should qualify as an emergency? Do you prefer texts, calls, or emails?

Agree to check in after 90 days to discuss what is working and not working.

Setting the foundation up front will help establish a clear working relationship that will benefit each of you and the property.

Here are some examples of how you can operate a property to give you an idea of how to develop your own operating philosophy.

Tenant Compliance

“Letter of the Lease”: strictly interpret the lease. Don’t give the property manager any wiggle room. If the tenant is unhappy, too bad. They signed the lease. If they paid a day after the grace period, immediately move to eviction.

“Best of Alternatives”: use the lease as a foundation, but be practical. You may be strict on the rent, but be more flexible on maintenance issues. Maybe the lease says that the tenant has to maintain the HVAC, but you tell the property manager that you are willing to pay for maintenance issues for tenants who are consistently paying rent on time.

I like option 2, but it does run the risk of getting out of hand if not closely monitored.

Property Maintenance

“Reliable but Basic Honda”: keep the property functioning well, but don’t try to fix and improve every possible issue.

“Top of the Line Mercedes”: keep everything looking and functioning perfectly. Cost is irrelevant.

“Car That Constantly Breaks Down”: do the bare minimum.

I operate my property as a “reliable but basic Honda” and use the “best of alternatives” approach to tenant issues.

Once you have set clear expectations with the property manager, you will want to decide how much discretion they should have.

How Much Discretion to Give Your Property Manager

When I talk about discretion, I am mainly referring to financial discretion. Spending money.

Your property manager will be making decisions daily that don’t cost any money. This is what you want. There is no point in paying someone to manage your property if they have to come to you for approval on every issue.

When it comes to financial issues, I recommend setting a dollar threshold under which the property manager has the discretion to resolve issues without coming to you for approval.

For example, you could set a threshold of $250. This could be per issue with a monthly cap or per month. This allows the property manager to resolve small issues without having to come to you each time for approval. It will save each of you time and will benefit tenant relations as issues can be solved real time.

Try a dollar threshold for a few months. If it works well and you develop an increasing level of trust with your property manager, consider increasing the threshold. If it is not working, consider reducing or eliminating the threshold.

Remember that you can change things over time.

Start with an approach, set a time period under which to try and evaluate it, and then make modifications if needed.

What To Do When Things Aren’t Working Out

All that being said, you can do everything to set yourself, the property manager, and the property up for success, but still have problems.

There will be times when things aren’t working out.

Welcome to being a real estate owner.

Here are some red flags to watch for relative to the performance of your property manager.

Poor Property Condition: the property is not being maintained to your agreed upon standards. You see this repeatedly in your property visits.

Non-Responsiveness: your property manager does not respond to your emails or calls. You may also hear from your tenants saying they are contacting you because the property manager is not responding to them.

Poor Treatment of Tenants or Vendors: in short, your property manager acts like a jerk.

Deadlines Consistently Missed: your property manager is responsive, but never hits agreed upon deadlines.

Sometimes these issues can be resolved with a conversation with your property manager (or your property manager’s boss). Sometimes they can’t.

When they can’t, it is time to make a change. Don’t settle for poor performance. You will lose tenants and spend more money maintaining your property in the long run.

Interview 2-3 new property management companies to find a better fit for you.

Closing Thoughts

Finding the right property manager is critical to your success as a real estate investor.

In the property I own directly with a partner, I experienced three of the four red flag issues above with the first property manager. I ended up firing them and finding a new one.

Everything has been SO much better since then. It was worth the time and the additional monthly expense.

Take the time to find the right team for you and your property.

Your time. Your money. Your choice.

Getting Meaning from Monthly Reports

Understanding income statements, rent rolls, A/R, and balance sheets

Let’s anchor in on where we are in the process of learning how to be a real estate investor.

You own your first property.

You have a business plan and are in the early stages of executing it.

You have hired a local property management and accounting firm.

You are eyes wide open that unexpected issues will come up.

Having a clear business plan relative to leasing and construction is probably the most important step you must take. We will get into the details of this in a future newsletter.

Today we are going to discuss how to interpret and get meaning from the monthly reporting package you will receive from your property management and accounting team.

I will define and discuss the individual reports that go into the reporting package:

Summary page

Rent Roll

Accounts Receivable (aka A/R)

Cash Flow and Income Statement with a Comparison to Budget

Balance Sheet

Construction Activity & Leasing Report

You do NOT need to have any accounting knowledge to understand these. All you need is patience, common sense, and a little guidance from Professor Bateman.

Let’s dig in.

Reporting Package Overview

Let’s start with the very basics.

What is a “reporting package” and where does it come from?

What: a reporting package is a collection of reports that help you understand how your property is performing.

When: it will likely be delivered to you within the first 10 days for the month and include activity for the previous month. Example: by May 10th you receive the report for April.

Format: it will be a pdf sent to you by the property manager.

The property manager’s accounting team will have prepared it according to the company’s accounting practices combined with the structure you (the client) have agreed upon. [Note: if you don’t have a property manager, you might have prepared it yourself or hired an accountant to do it.]

You don’t need to be an accountant to understand the reports, but it does help to have some foundational knowledge. Here are some basics.

Whenever there is financial activity at a property, the accountant records it in the general ledger. This could include:

Rent charged to or paid by the tenant.

A maintenance invoice received by or paid to a vendor.

Distributions made to investors.

And any other financial activity.

Think of the general ledger as a big excel file with (i) a date, (ii) a category ID, (iii) the amount, and (iv) comments.

Most reports are just a roll up of this activity, summarized in a specific way using the dates, category IDs, and amounts.

That’s about it. Yes, it is an oversimplification of the reporting process but it gives you an overview of how it works.

To be clear, it is way more complicated if you are doing the work, but as a reader of reports this should anchor you on the basics.

Now let’s discuss the individual reports within the reporting package. Your specific report may be different in order and content. Use the list below as an example only.

#1 - Summary Page

The summary page is just as it sounds: a summary. It will include highlights such as:

Property square feet and percent leased.

List of new or vacating tenants.

Amount of rent not paid (aka delinquent).

List of construction or maintenance projects.

Current cash, recent distributions, NOI and any other “snapshot” financial data.

There may be comments on some or all of these or it could just be a statement of the facts.

All of it will likely be in one page. It will help you understand the overall property performance before you read the individual reports.

#2 - Rent Roll

The rent roll is a summary of the leases and suites for your property.

Each accounting firm will create a slightly different version of a rent roll. Rent roll templates can also differ by asset class.

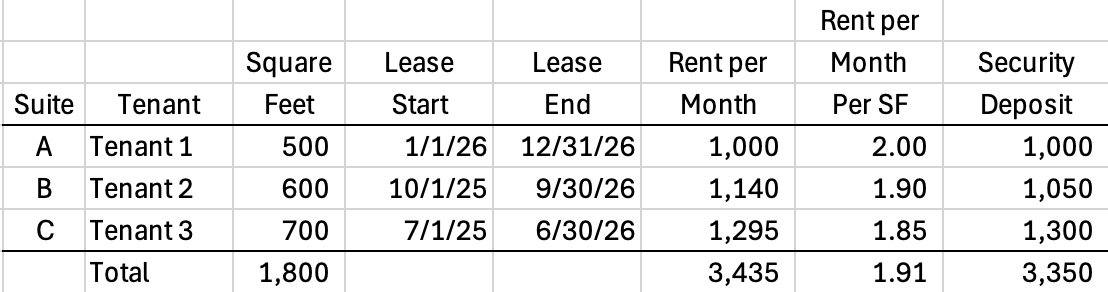

See below for an example of a rent roll for a three unit residential property.

Example: Rent Roll of 1-4 Unit Residential Property

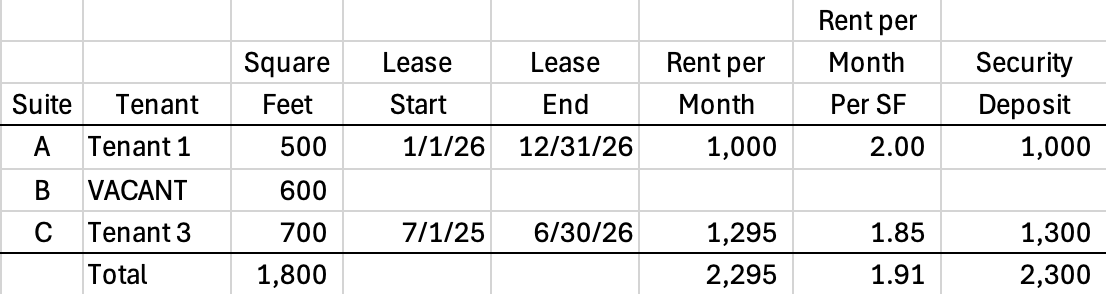

It gives you a way to see your tenants in a summarized report. If there was a vacant suite, it would be listed as vacant as shown in the example below.

Example: Rent Roll of 1-4 Unit Residential Property - Including Vacant Suite

Important Note: never rely exclusively on your rent roll when making a decision about a specific tenant. In this case, you want to refer to the signed lease as there could have been a mistake made when the rent roll was prepared.

That being said, rent rolls are very useful to reference day to day.

Let’s move on to the A/R report.

#3 - Accounts Receivable (A/R)

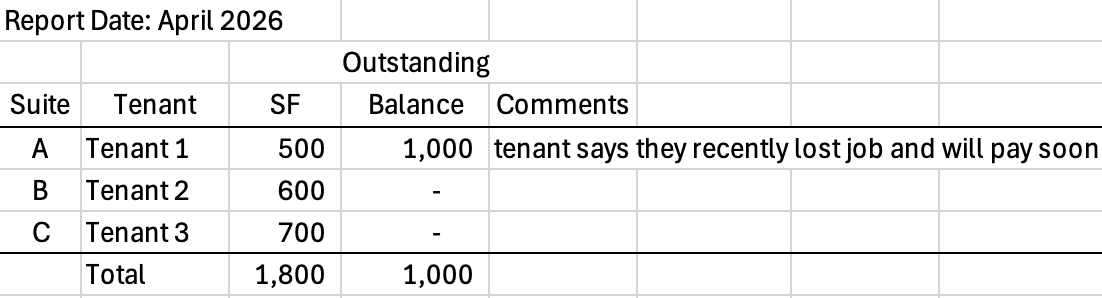

Whereas a rent roll lists what each tenant is contractually required to pay each month, the A/R report will be your guide to what the tenant actually paid.

In the example above, Tenant 1 in suite A is supposed to pay $1,000 per month. If they did not pay that month, the A/R report would show this outstanding balance (aka delinquency).

Example: A/R Report

The comments would have been added by the property manager who would have (hopefully) contacted the tenant to find out what was going on.

It is then your decision as the property owner to decide whether to allow the tenant some time to catch up on the rent or move to eviction.

Let’s move on to the overall property performance reports.

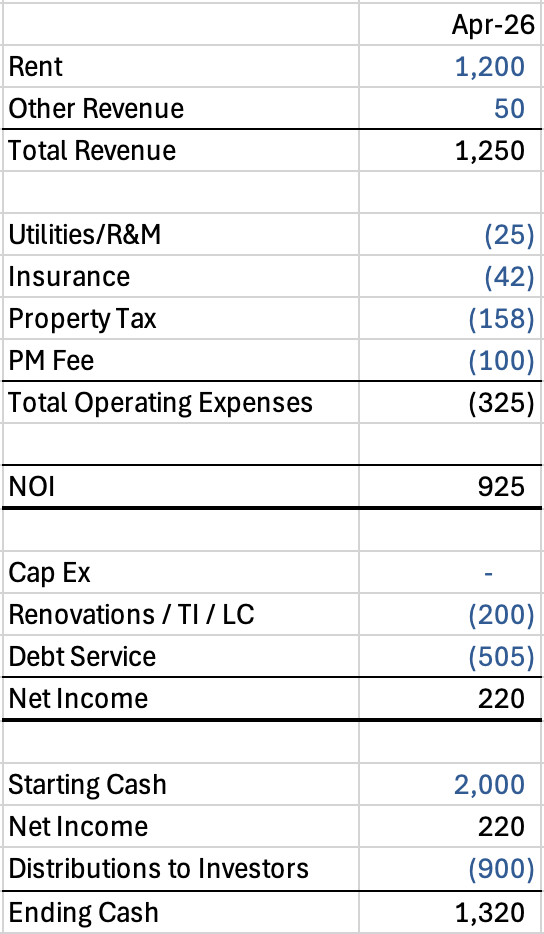

#4 - Cash Flow & Income Statement

Rent rolls and A/R reports are specific to revenue. The cash flow and income statement capture the revenue and expense activity that combine into the net operating income (NOI) and net income.

As an individual investor, I like to think of the cash flow and income statement as a single report.

But those of you who are accountants or in the real estate industry probably recognize that this is not always the case. Here’s how they differ:

An income statement is a summary of activity through NOI and inclusive of debt service, capital improvements (capex), leasing costs (tenant improvements and commissions) that totals in net income. It does not necessarily correlate to (a) the cash activity that occurred at the property that month nor (b) include a starting and ending cash balance.

This is because there are many, many accounting rules that indicate how reports should be prepared. They are anchored on logic that makes sense, but do not always result in helpful information for an individual investor.

Here’s what a cash flow and income statement might look like.

Example: Cash Flow & Income Statement

It looks like an income statement through “Net Income” but then adds comments on the starting and ending cash to give you an ending cash balance.

Cash is king. You always want to know how much cash you have.

A further variation on the income statement would be to include a “comparison to budget”. This would look like the example above with three extra columns:

The budgeted amounts for that month. The monthly budget would have been finalized at the end of the previous year - in this example, the end of 2025.

A comparison of the actual amounts to the budgeted amounts.

Comments on any significant variances to budget.

Now that you have a sense of a cash flow and income statement, let’s move on to the balance sheet.

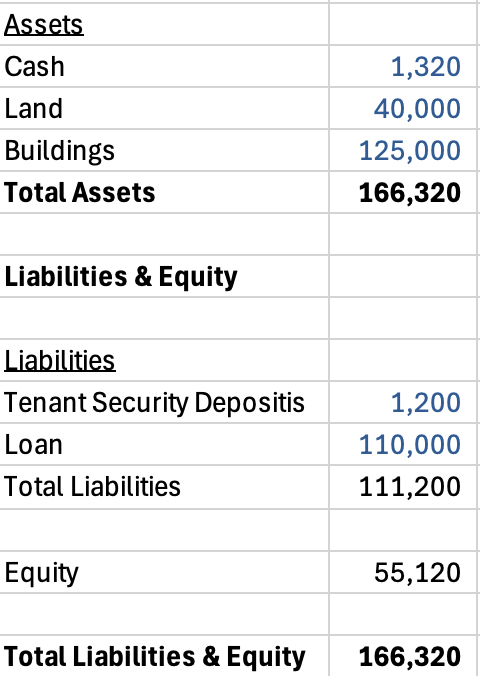

#5 - Balance Sheet

A balance sheet is a snapshot of assets, liabilities, and equity.

Assets are things at the property that have value.

Liabilities are things the property owes to others.

Equity is the difference between the two.

It looks like this.

Example: Balance Sheet

The balance sheet is literal. It must “balance”.

Assets = Liabilities + Equity

Equity = Assets - Liabilities

Balance sheets are helpful to track your liabilities, but I don’t find them particularly useful in my day to day operations of a property.

#6 - Construction Activity & Leasing Report

These last two reports will vary in both who they come from and what they look like.

A construction activity report will likely come from the property manager. It will provide some level of detail on planned, in process, and completed construction activity. It will show things like (i) costs - both budgeted and actual, (ii) timeline - both budgeted and actual, (iii) a narrative on how the work is going.

This will likely be your most important report if you are in the middle of a renovation.

A leasing report will either come from your property manager (all residential properties) or your broker (all commercial properties). It will show leasing activity and lease comparables (aka lease comps).

Lease comps are completed leases at similar properties. They help give you a benchmark of what similar properties are leasing for in the same market. They help you determine what you should charge for rent for your property. We will get into this in a future newsletter.

So what is the takeaway on all these reports?

My Recommendations

Here’s how I use the reports.

For the deals in which I am a limited partner (LP) investor, I read the summary of the report with a focus on what is most important to me. If cash flow (aka investor distributions) is most important, I focus on that.

I recognize that as an LP (a) I have no control over day to day activity nor decision making and (b) I have invested as an LP so I don’t have to do any work. With this in mind, I don’t bother reading much beyond the summary page(s).

If you are an individual LP investor, you will “get what you get” relative to reports from the general partner (GP). Here are three examples of reports I get as an LP investor with three different GPs.

Monthly report an income statement and balance sheet, but with minimal narrative.

Quarterly report with detailed narrative and an income statement.

Annual letter with a narrative only. One page. No numbers.

This does not correlate to the property performance. It is just a choice that each GP has made as to how they want to communicate with their investors. As an LP, I have no ability to change this.

When I am investing by myself or with a partner, I take the opposite approach to reviewing the reporting package.

Not only do I read everything in the report, but I also have my own excel file of (i) monthly cash flow and income statement, (ii) rent roll, and (iii) capex report.

My excel based cash flow and income statement includes both historical and projected amounts per month with a running cash balance so I can project capital spending and investor distributions.

It is more work for me to enter the information from the reporting package pdf into excel each month, but it is well worth the effort as this makes sure I really understand the property financial performance.

A side benefit is that as long as the property manager gives me the information I need to enter into my excel file, I don’t care what format they deliver the reports to me in. They can use their standard templates.

Recognize that if you ask a property manager for customized reports that differ from their standard templates, it may be more work for them. This could mean more costs to you.

Make sure you agree on the content, timing, and frequency of the reporting package before you hire your property manager or accountant. I suggest starting by requesting an example reporting package and seeing if it has the content you need.

Red Flags to Watch For

As you review the reports, here are a list of things to be on the lookout for.

Increasing A/R: this indicates tenants are consistently paying late or not at all. Work with your property manager to come up with an action plan.

Actual Expenses Are Significantly (>10%) Over Budget: either your budget was too low or there are issues going on at the property. Discuss with your property manager.

Minimal Cash Balances: always leave a cash cushion for the unexpected.

Vacant Suites Staying Vacant for 3+ Months: work with your property manager or leasing broker. You may need to lower the asking rate or change brokerage teams.

Construction Delays and/or Cost Overruns: watch this closely and actively manage the team managing the jobs.

Pay attention and don’t be shy about calling your property manager to discuss in detail. Use your common sense and ask questions. Don’t be a jerk, but don’t be too passive.

Your Property, Your Choice

You can decide how you approach each investment.

It is your investment, your money, your time.

And you can always change your approach to report review over time. That is what I did.

How I approach it today is different than I did five years ago and will likely change five years from now.

That is learning and evolution. As my needs change, I adapt my approach to better meet my needs.

Don’t be intimidated by the jargon of real estate reports: income statements, rent rolls, and balance sheets.

Ask your property manager or accountant to explain them to you in simple terms. Take notes. Be a student.

After reading a month or two of reports, you will find they are key to extracting meaningful insight into how your investment is performing.

Daily Issues You Will Face While Owning Real Estate

From A/R to maintenance issues to finding tenants

Over the past three weeks we have covered real estate terms, getting organized, and developing your leadership skills.

Now we are going to get into the day to day issues you will face as a real estate investor.

Just as we did in the discussion on due diligence, we are going to use an income statement as our guide.

Revenue

Operating Expenses

Capital Improvements

Leasing Costs

Interest Costs (i.e. debt)

Other Issues Affecting Value

Almost everything you will be faced with could have an impact on the income statement. All other issues will have an impact on sale value and debt options.

I won’t overwhelm you with trying to give every detail of each issue. Think of this as a high level overview. We will dive into the specifics in the rest of the newsletters in this series on operating real estate.

Let’s dig in.

What is an “Issue”?

For this discussion, let’s define an issue as something that comes up that you have the power to take action on. That is not to say that there is a solution for everything, but most of the time there is something you can do.

But let’s make something very clear:

There are many things that will be outside of your control that will affect the performance of your property. Examples of these over the past 10 years include:

A global pandemic

Inflation that impacts both costs and interest rates

War

Political policies and changes in laws

That being said, there are many things within your control. You want to know what those are and what your options are. That is where this newsletter comes in.

Let’s start with revenue.

Revenue

As a reminder, revenue is made up of rent from tenants (and other income like parking) but is offset by vacancy and credit loss (i.e. tenants not paying rent).

Issue #1 - Tenants Not Paying Rent

You have leases in place but the tenants are not paying rent or are paying late.

Your Options: (i) do nothing; maybe you can live with the tenant paying late as long as they pay by the end of the month, (ii) same as previous but also charge a late fee, (iii) talk with the tenant to understand if this is a temporary issue; if so, work out a payment plan, or (iv) evict the tenant.

Future Discussion Newsletter: property management.

Issue #2 - Existing Tenants Causing Problems

Maybe they are loud or leaving trash in the common areas. They are doing something that disrupts others and/or damages the property.

Your Options: (i) do nothing; be a passive landlord, (ii) all bark, no bite - threaten to do something but never do it, or (iii) give the tenant a deadline to resolve the issue and then move to eviction if they don’t.

Future Discussion Newsletter: property management.

Issue #3 - No Tenant

To state the obvious, if you don’t have a tenant in one of your units you will not get rent. Said another way, this is vacancy at your property. It is like an airplane that takes off without a passenger in a seat. You will never get that rent back.

Your Options: (i) find a tenant by working with a motivated broker that knows the local market and/or (ii) expand an existing tenant.

Future Discussion Newsletter: leasing.

Issue #4 - Lease Rate

How aggressive do you want to be in setting your lease rates? Are you willing to give an existing tenant a lower lease rate than you would a new tenant?

Your Options: understand the market conditions and decide on an operational philosophy. Maybe you care more about steady cash flow than driving the rent as high as possible with periods of vacancy.

Future Discussion Newsletter: leasing.

Issue #5 - How a New Tenant Will Use the Space (Commercial Properties Only)

You may have a tenant ready to lease your space at a great lease rate, but you are concerned about how they will use the space. You could be worried they will be disruptive to other tenants and/or be hard on your property.

Your Options: talk with your broker and people your trust. Check with your insurance broker to see if it will affect your insurance rates. Consider a shorter term lease and put strong usage language in the lease.

Future Discussion Newsletter: leasing.

That should be enough to chew on for revenue. Let’s move on to operating expenses.

Operating Expenses

Operating expenses are made up of utilities, repairs and maintenance (“R&M”), insurance, property taxes, and property management fees (“PM Fee”). Some assets will have a more detailed list, but these are the major items.

Issue #6 - R&M: Costs vs. Quality

You will have a number of vendors performing services such as landscaping, pest control, HVAC maintenance, etc. You will need to analyze the trade-offs between frequency, quality, and price.

Your Options: develop your own operating philosophy. What kind of landlord do you want to be? Do you want to operate the property like a top of the line Mercedes, a reliable but basic Honda, or a car that constantly breaks down?

Future Discussion Newsletter: property management.

Issue #7 - Property Manager

This is a similar concept. What are you looking for in your property manager? How proactive do you want them to be? Are you willing to pay more for a property manager with a manageable workload, or do you want the cheapest that has an unrealistic number of other properties?

Your Options: same concept as R&M costs.

Future Discussion Newsletter: property management.

Issue #8 - Insurance

Insurance can get expensive. You will be faced with the choice of having broad coverage or minimal coverage. If you have a loan on the property, the lender will play an active role in determining your coverage requirements. Broad coverage is more expensive than minimal coverage and unfortunately there is no “right” answer to the amount of coverage to have. Additionally, you may have to file an insurance claim at some point.

Your Options: (i) understand your tolerance for risk and (ii) dive in deep and early when you have an insurance claim by actively engaging with your insurance broker and/or claims adjuster.

Future Discussion Newsletter: insurance and property taxes.

Let’s move on to the “below the NOI” line items. Reminder: NOI = Revenue minus Operating Expenses.

Capital Improvements (aka Capex)

Issue #9 - Repair or Replace

Things are going to break and deteriorate. That is the reality of owning a property. It might be the HVAC unit, a dishwasher, or a section of the roof. As the landlord, you may need to address this under the terms of the lease.

Your Options: (i) read the lease to determine who is responsible for the issue - landlord or tenant, (ii) review the age of the system - example: if the HVAC unit is 20+ years old, a replacement may make more sense than a repair, (iii) price out both the repair and the replacement, and (iv) get opinions from multiple vendors.

Future Discussion Newsletter: construction.

Issue #10 - Replacement Quality

This is the same concept as R&M vendors and property managers. How high a quality system and work do you want for your property. Are you OK with the cheapest lighting, HVAC, and quality of work that won’t last as long but is less expensive? Or are you willing to pay more for high quality systems and work that will last longer term?

Your Options: (i) develop your own operating philosophy, (ii) be eyes wide open on the trade-offs and the reality of your cash position, and (iii) get multiple bids for the work and talk with the contractors about their work before you sign a contract.

Future Discussion Newsletter: construction.

Leasing Costs: Tenant Improvements (“TI’s”) and Broker Commissions

Issue #11 - Your TI Budget

How much are you willing to spend for the right tenant? What is the reality of your cash situation? Although TI’s are mainly applicable to commercial properties, the same concept applies to residential relative to how much you want to improve the unit for a prospective tenant.

Your Options: (i) develop your own operating philosophy, (ii) be careful of tenants that want specialized TI’s that are unlikely to be re-used by a future tenant, or (iii) try to push the cost of the TI’s onto the tenant in exchange for free rent and/or a lower lease rate.

Future Discussion Newsletter: leasing.

Issue #12 - Leasing Commissions (Commercial Properties)

Brokers play a very active role in leasing commercial properties. Commissions can get expensive and need to be paid at the time the lease is signed (i.e. upfront). This can squeeze you on cash at a time your revenue is down because you have a vacant suite.

Your Options: (i) build up cash prior to a potential vacancy and (ii) understand the time commitment and risks of not using a broker.

Future Discussion Newsletter: leasing.

Let’s move on to debt.

Interest Costs, Debt, and Other Lender Issues

Issue #13 - Rising Interest Costs

You may be tempted by the low interest rate that come with a floating rate, adjustable loan. But if interests rates go up, your monthly interest costs could double. Yikes!

Your Options: there may not be any options if your interest costs go up. This could wipe out your cash flow and/or put you in a situation where you can’t make debt service. Be very careful of floating rate debt. This adds a significant amount of uncontrollable risk.

Future Discussion Newsletter: investor and lender issues.

Issue #14 - Lender Approvals

As discussed in Debt: An Amazing Tool with Strings Attached, your lender may have approval rights on a number of issues and not allow you to do what you believe is best for the property.

Your Options: (i) read and understand the loan documents so you know your rights, (ii) develop a positive working relationship with your lender from day one and be reasonable; this will pay dividends in the future, and (iii) make the case for why you want to do what you want to do.

Future Discussion Newsletter: investor and lender issues.

And finally, let’s quickly address “other issues”.

Other Issues Affecting Value

There are some issues that may not affect your cash flow during ownership, but will be problems when you go to sell or refinance the property. These could include:

Environmental issues

Zoning changes

Challenging neighbors

Challenging tenants

Your Options: (i) conduct annual property reviews to identify issues early, (ii) maintain good relationships with city officials and neighbors, (iii) address problems immediately rather than letting them compound, and (iv) document everything in case issues arise during sale.

The key is to be eyes wide open on the risk to your future sale and/or refinance and then try to resolve the issues as best as you can before you are in the time crunch of a sale or refinance.

That’s the list of 15 or so issues. Are these all the possible issues you will face?

No, but they give you a sense of the type of issues you will face.

What are our key takeaways?

Key Takeaways

Here’s what you need to keep in mind:

Develop your own operating philosophy. Combine this with your niche, and you will have a clear foundation on which you evaluate your decisions. Without a philosophy, you will find yourself over analyzing each decision and not having any consistent approach.

Issues that you need to figure out will come up. Methodically break them down into parts. Do the research. Talk to experts. And then make a decision.

Not all issues are equal. Cash flow problems (non-paying tenants, rising interest costs) demand immediate attention. Quality decisions (Mercedes vs Honda) can be determined over time.

There will be unexpected costs. Keep a cash cushion. Don’t distribute every last dollar.

Life is full of challenges. Think of all the ones you have overcome in your life just to be able to be sitting here reading this newsletter.

Operating real estate is a lot more complicated than owning stock.

It can be time consuming and stressful. There is no sugarcoating it.

If you don’t want this in your life but you still want to be a real estate investor, there is alway the option to invest as an LP and have the GP do all the work (for a fee).

But for those of you willing to do the work, it can be financially lucrative and intellectually rewarding.

You can do it.

Developing Your Leadership Skills

The power of reading non-fiction and creating a reading journal

Reading non-fiction has made me a better leader.

No question. No debate.

I have learned so much through the reading process, not just about other subjects, but also about myself.

Last week we talked about getting organized. Soon we will be moving on to all the things that will come with operating your property: (i) proactively executing your business plan, (ii) reacting to issues, and (iii) leading others to accomplish your goals.

You need to develop your own tools to do these well. Not just the specifics of real estate, but also the fundamental leadership skills needed for these functions in anydomain.

That is why this week we will talk about reading as a foundational practice to understand yourself and develop your leadership skills.

We will cover three topics:

The list of some of my favorite books that talk about key skills to develop.

How to remember what you read by creating your own reading journal.

The most important skills all leaders need.

Let’s dig in.

Why Non-Fiction

Fiction is tons of fun, but non-fiction helps me grow.

It makes me a better leader, investor, employee, and professor.

It makes me a better person.

It expands my perspective and helps me think.

Non-fiction books are also an insane bargain. For less than $20 (or free at the library) you get a comprehensive presentation of someone's deep research into a subject.

That person put 100's of hours into creating it.

An editor read many drafts to perfect the organization and main points.

All of this is then there for anyone to buy for less than $20. What a deal!

So here’s a list of books I recommend to make you a better leader, not only of your properties, but also of your life and everything else you do.

Recommended Reading List

Understanding Yourself: if you don’t understand yourself, you will limit your growth.

Emotional Intelligence 2.0 by Travis Bradberry and Jean Greaves: probably one of the most foundational discussions of not only how to understand emotional intelligence (aka EQ), but also how to develop it. Emotional intelligence is critical to working with others.

Mindset by Carol Dweck: one of the most influential psychology books of the last decade. Do you have a fixed or growth mindset? Read this book to understand the importance of a growth mindset and how to develop one. It may change your entire perspective on life.

Grit by Angela Duckworth: understand the need for consistency of effort over the long run to achieve your goals.

Quit by Annie Duke: Duke is both a university professor and former world poker champion. She discusses our bias against quitting and shows you the formula for when you should quit.

Clear Thinking by Shane Parrish: a guidebook on how to make better decisions.

Your Career & Leadership: read to help guide your career and become a leader.

Legacy by James Kerr: short lessons on leadership based on the legendary New Zealand national rugby team. I think I have read this four times.

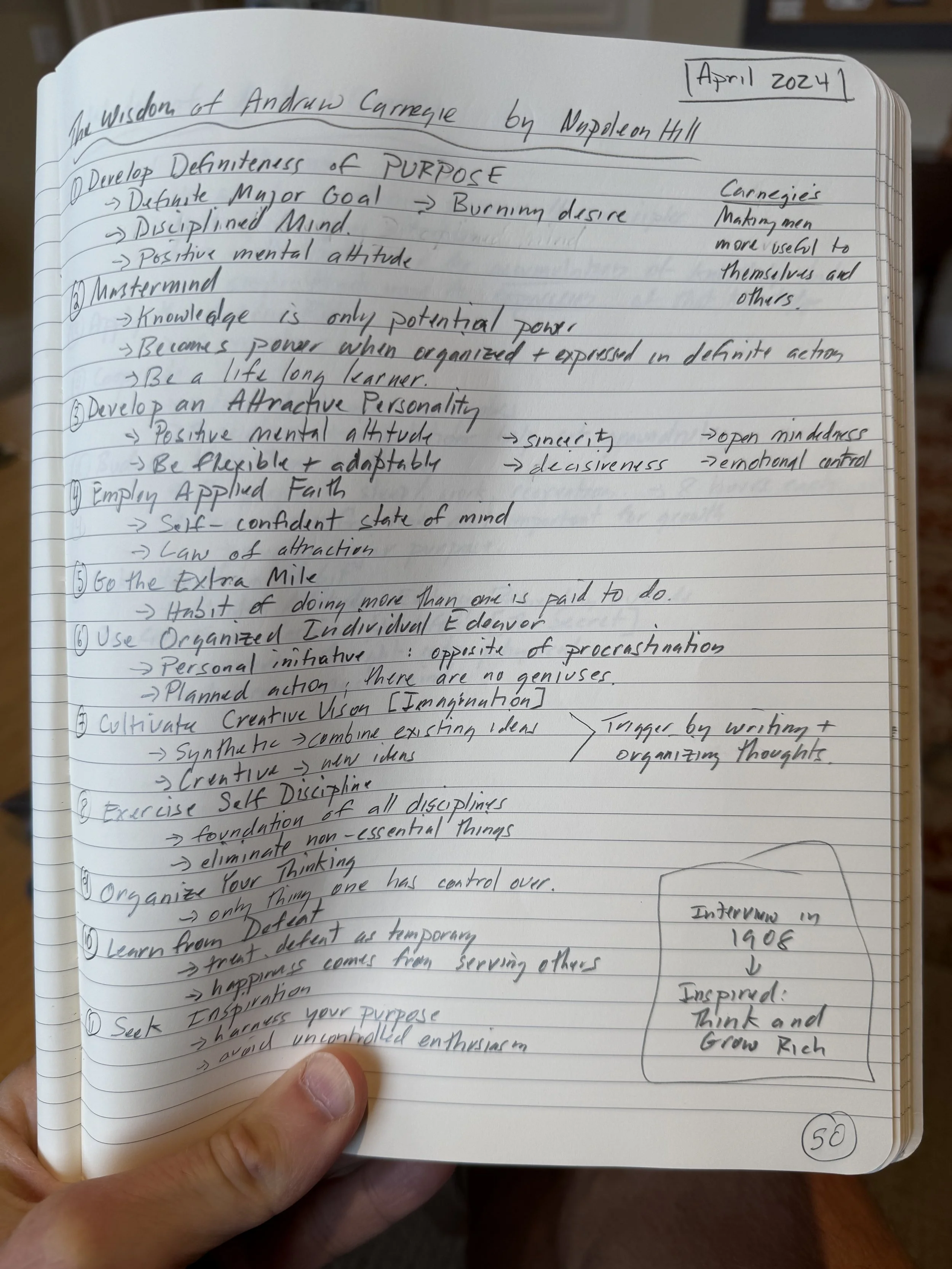

The Wisdom of Andrew Carnegie as told by Napoleon Hill: this was the precursor to Think and Grow Rich. It is an interview with Andrew Carnegie full of his principles for a successful life. These lessons from 1908 still hold true today.

The Infinite Game by Simon Sinek: a discussion on a more grounded form of leadership that yields better results.

Atomic Habits by James Clear: the incredibly popular book on the importance of habits and how to develop them. Over 25 million copies sold. Read it. Live it.

Money and Investing: these will help you think about investing at a more foundational level than just real estate.

What to Make of a Life by Jim Collins: helps you understand the power of what happens when you find the things you are naturally good at.

The Psychology of Money and The Art of Spending Money both by Morgan Housel: these books help you understand the major role that psychology plays in influencing all of our decisions about money.

The Simple Path to Wealth by J.L. Collins: this guy is the master of helping you understand the stock market and its importance as a passive vehicle for wealth creation. He also explains what IRAs, 401Ks, and 529 plans are.

The Algebra of Wealth by Scott Galloway: wealth = focus + (stoicism x time x diversification).

The Five Types of Wealth by Sahid Bloom: helps you think beyond wealth as being limited only to money.

Living a Good Life: making money is a way earn your freedom, but it is a pointless exercise if you don’t live a good life.

Transitions by William Bridges: explains the three steps we go through when making transitions in life.

30 Lessons for Living by Karl Pillner: based on interviews with people in their 70s, 80s, and 90s. A great way to learn from those that have “been there, done that” in the journey of life.

The Daily Stoic by Ryan Holiday: I read this every morning. One page per day. I can’t speak highly enough about stoicism. It is the 2000+ year old philosophy that is anchored on the concept of distinguishing between what you can and cannot control. Don’t waste your time getting emotional on what you cannot control. All of Holiday’s seven+ books on stoicism are outstanding.

That’s my curated list of 15+ favorites from the 50+ non-fiction books I have read in the last five years.

Now what?

Let’s say you choose to read some or all of these books. Pick one that looks interesting. Create a dedicated 20-60 minute uninterrupted block to start reading. Keep going if it interests you. Move on to another book if it doesn’t.

Remember, I didn’t magically read all of these at once. I found one that was interesting (Atomic Habits) and kept following my curiosity.

The list I am sharing here is a manifestation of the power of compounding in action.

I have found that 10-12 books per year is my pace. I tend to go through spurts, reading three books in six weeks and then not reading anything for a month or two. Find your own rhythm but make reading a priority.

Ideally, you want to retain the key learnings from each of these books to be able to refer back to them when you feel the need. This is what we will talk about next.

Remember What You Read: Create Your Own Reading Journal

I used to mainly listen to non-fiction books via audio. I enjoyed listening while on a hike or during a car ride. It was super convenient.

The downside to this convenience was that I often forgot the lessons of the book months later.

Then I heard about the concept of a commonplace library: the idea of writing down the key points or quotes of a book in a centralized place (ex. notecards by subject or a reading journal).

This required me to restructure the way I read.

I moved to a kindle so I could highlight as I go. Highlighting is key to be able to go back and reference the important parts of the book.

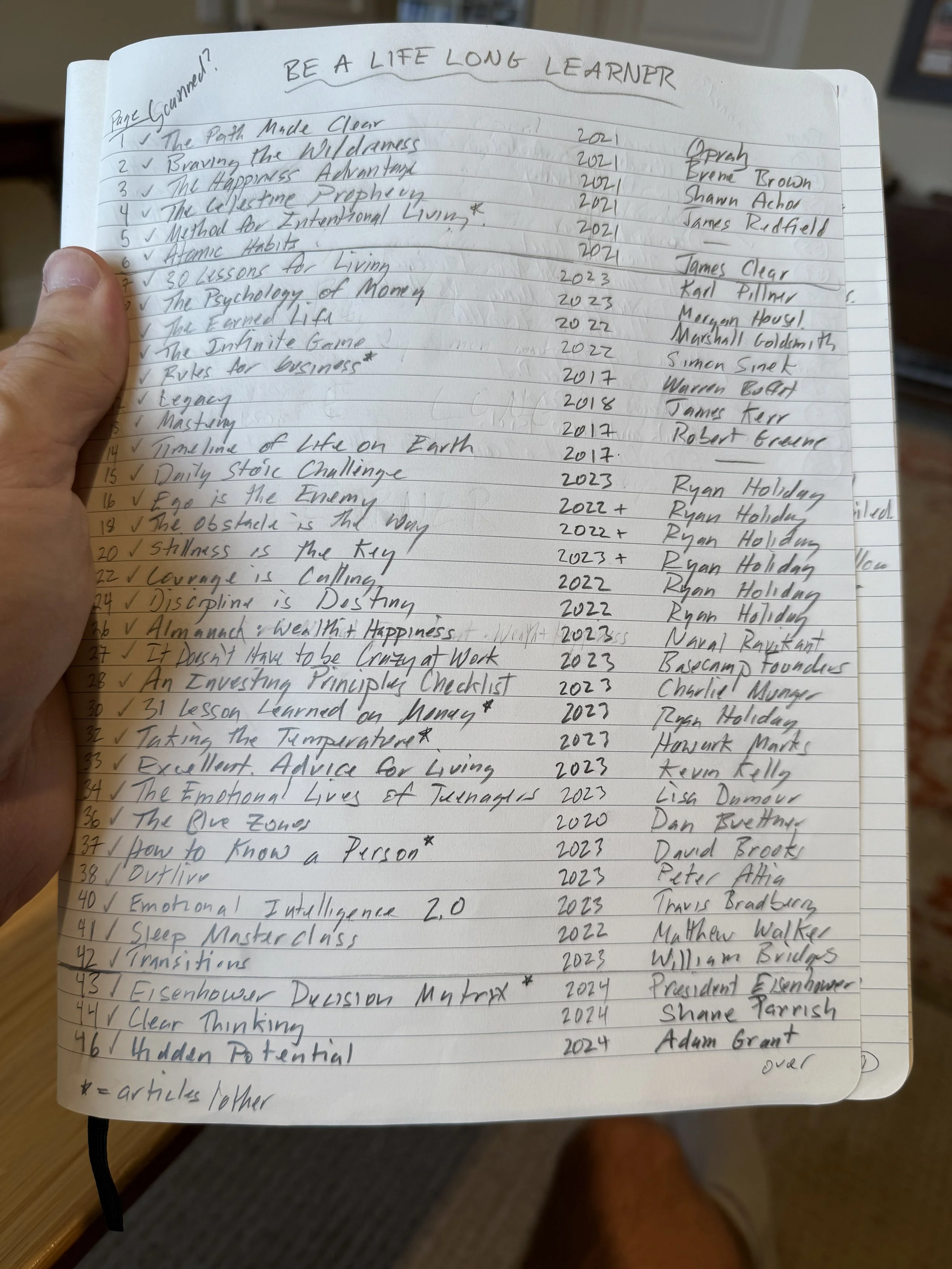

I bought a Moleskin journal that is dedicated to summaries of the books I read. One to two pages of notes per book. Here are the specific steps:

Read the book in any format that allows you to highlight specific passages.

Once you finish the book, set it aside for a week or so.

Come back to the book with fresh eyes to go through the highlighted sections. Summarize the key concepts in your dedicated journal. I don’t bother with quotes or putting in everything I highlighted. I just want to capture the key concepts. I like being limited to 1-2 pages of notes.

I now have a journal full of knowledge that I can refer back to. It is one of my favorite possessions. These pictures will give you a better sense of it.

Note: if you absolutely have to listen on audio, consider carrying around a notebook to take notes as you go.

Image 1: My Moleskin Journal Dedicated to Reading Summaries

Image 2: The Table of Contents

Image 3: An Example of a Book Summary

Anytime I am making a big decision or think of something that I have read and want to re-visit, I turn to my reading journal.

So what have I learned about leadership through reading and becoming a leader at work?

Important Leadership Skills

Be Clear on What You Want: get priorities correct so as to spend time on the correct things.

Measure Success: figure out how to measure whether you are achieving your goals. Measure what matters. Results will follow

Be Driven & Humble: this is the magic combination. Recognize you can always learn from others. You don’t want to be the smartest person in the room.

Give credit to others. Take the blame for mistakes.

Embody the leadership skills you admire. People will watch what you do more than what you say.

Build and Rely on Your Team: don’t do everything yourself. Assemble a team of people that are good at specific areas. Trust them and give them room to do things their own way. Don’t micromanage them.

Respect Differences: other people’s ways may be different from your own. It is results that count, not the methods.

Be Prepared: for meetings and discussions. This means doing the reading and research in advance and expecting the same from others.